Archive for August, 2006

-

The Election Cycle Revisited

Eddy Elfenbein, August 10th, 2006 at 6:03 amA few months ago, I wrote about the stock market’s election cycle. This is one of those bits of market trivia that I usually don’t have much faith in. But I have to admit that the evidence is pretty strong that the market follows a four-year cycle.

The indexes seem to have had several major bottoms during mid-term election years (see here). In April, I crunched the data from Ibbotson and Associates to see what the average cycle looks like, and this is what I got:

You can see that the market runs into a wall in the year after an election, and stays flat through most of the mid-term election year. The theory is that the incumbent president tries to make the economy look great for Election Day, and everything goes to hell shortly afterward. This data was based on the market’s total return (dividends included) from 1926 through 2005.

The data I had was monthly, and I wanted to see if I could narrow it down some. I looked at all the daily closings for the Dow Jones from the start of 1929 through this past Tuesday. That’s roughly 19-1/3 election cycles. This is slightly different because it’s just one index and dividends aren’t included, but I do have the benefit of zeroing in on a specific day.

This is the average Dow election cycle looks like:

You can certainly see a similar pattern here. The market hits its low on September 30 of the mid-term year (not too far away!) and peaks on August 3 of the post-election year. In that 14-month period, the market declines an average of 9.4%. The market is up 46.8% over the other 34 months.

What I really found surprising is that the bullish period is very heavily concentrated within the first 12 months.

From September 30 of the mid-term to September 13 of the pre-election year, the Dow is up an average of 31.6%. To put that in perspective, the Dow averages a gain of 33.1% over the entire four-year period. So every four years, 95% of the market’s capital gains is squeezed into a one-year period (on average).

If you’re curious, the market’s best day during the four-year cycle is September 21 of the election year (+1.15%, thank you 1932) and the worst day is October 19 of the pre-election year (-2.04%, thank you 1987). And most importantly, Leap Day is slightly positive (+0.12%). -

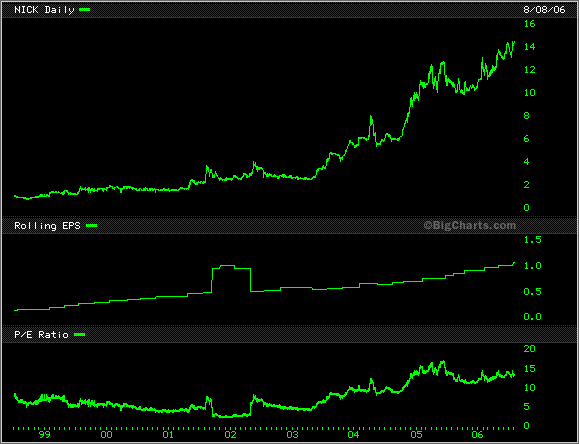

Nicholas Financial

Eddy Elfenbein, August 9th, 2006 at 11:30 amFor today’s edition of “Widdle Biddy Stocks That Ain’t No One Never Heard Of,” I give you Nicholas Financial (NICK).

Nicholas is a Florida-based company that provides auto loans for used cars, a segment that’s often not served by larger lenders. I’m not joking when I say this is a small company, about 200 employees and a market value of $140 million. Citigroup, by comparison, is over 1,500 times larger.

But dude, check out NICK’s results:

Year…………Sales (mil)………EPS

1997…………..$6.21…………$0.12

1998…………..$7.94…………$0.13

1999…………$10.42…………$0.22

2000…………$14.07…………$0.34

2001…………$17.80…………$0.45

2002…………$20.22…………$0.50

2003…………$22.38…………$0.54

2004…………$25.50…………$0.64

2005…………$32.83…………$0.80

2006…………$42.68…………$1.01

That grabs my attention. NICK has certainly found a niche for itself. The company recently reported first-quarter results (the fiscal year ends in March). Net income grew 29%. The company earned 29 cents a share compared with 23 cents last year. This brings their trailing four-quarter earnings up to $1.07 a share. That means that the company is going for less than 14 times earnings.

There’s not much info on Nicholas, but here’s part of article on the company from 2004:The interest rate Nicholas can charge is dictated by state regulations, and it won’t go into a state where it can’t get a rate of at least 20 percent.

Generally, Nicholas borrowers don’t qualify for traditional sources. The economy has made more people “credit-challenged,” but Finkenbrink says that doesn’t mean they are bad risks.

“We try to finance people who may have had trouble because of a divorce, medical problems or job loss, as opposed to ‘credit criminals,'” he said.

Creating relationships

The company’s branch system is key. Branches require overhead, but they put employees in touch with customers.

“Customers like to come into the office,” Finkenbrink said. “We create relationships, and employees often will counsel customers.”

The result is low delinquency. For the past few years, about 1 percent to 2.5 percent of total loans due at any one time are more than 30 days past due, according to an April 14 research report from Atlanta-based Westminster Securities.

Many larger companies pulled out of the sub-prime auto loan business in the 1990s when they failed to make a lot of money at it, said Will Lyons, Westminster director of equity research.

Currently, GMAC and Ford Motor Credit dominate the industry, and Nicholas has only one-tenth of 1 percent of the market, according to an investors presentation by Nicholas.

“Nicholas takes a personal approach to every loan they do,” Lyons said. “It costs a lot of money to do that, and big companies don’t want to take that kind of approach.”Here’s the chart:

-

The Fed Pauses

Eddy Elfenbein, August 8th, 2006 at 2:52 pmSeventeen and done…for now. Not a good move in my opinion.

Here’s the statement:The Federal Open Market Committee decided today to keep its target for the federal funds rate at 5-1/4 percent.

Economic growth has moderated from its quite strong pace earlier this year, partly reflecting a gradual cooling of the housing market and the lagged effects of increases in interest rates and energy prices.

Readings on core inflation have been elevated in recent months, and the high levels of resource utilization and of the prices of energy and other commodities have the potential to sustain inflation pressures. However, inflation pressures seem likely to moderate over time, reflecting contained inflation expectations and the cumulative effects of monetary policy actions and other factors restraining aggregate demand.

Nonetheless, the Committee judges that some inflation risks remain. The extent and timing of any additional firming that may be needed to address these risks will depend on the evolution of the outlook for both inflation and economic growth, as implied by incoming information.

Voting for the FOMC monetary policy action were: Ben S. Bernanke, Chairman; Timothy F. Geithner, Vice Chairman; Susan S. Bies; Jack Guynn; Donald L. Kohn; Randall S. Kroszner; Sandra Pianalto; Kevin M. Warsh; and Janet L. Yellen. Voting against was Jeffrey M. Lacker, who preferred an increase of 25 basis points in the federal funds rate target at this meeting.Lacker is the President of the Richmond Fed.

Two other bank presidents, Moskow and Poole, were probably for another rate increase. Since the bank president’s rotate turns, those two won’t be able to vote until next year.

Can you tell when the announcement came?

-

The Fed’s Decision

Eddy Elfenbein, August 8th, 2006 at 11:04 amAt 2:15 we’ll find out what the Fed will do. For the first time in a while, there’s actually some drama to a Fed announcement.

According to the latest futures contracts, the market believes there’s a 21% chance of a rate hike. Personally, I’m a little baffled. It’s seems pretty obvious that the Fed needs to get rates higher. We’ll know more this afternoon. -

My Favorite Links

Eddy Elfenbein, August 8th, 2006 at 10:18 amI’m very bad in updating my links page but I finally got around to it. Please check out some of the other stock bloggers.

Some of my favorites include Justin Walters and Paul Hickey over at Ticker Sense, Barry Ritholtz, John, Elizabeth, Joe, Muffie & Co. at DealBreaker, Herb Greenberg, David Phillips at 10-Q Detective and Michelle Leder at Footnoted. -

Hansen Cracks

Eddy Elfenbein, August 8th, 2006 at 10:03 am

Hansen Natural (HANS) has been one of the hottest stocks on Wall Street. But yesterday, the shorts finally caught up to the Monster Energy drink maker.

The company’s earnings were in line with expectations (28 cents a share) yet the stock fell $10.40 a share, or 25%. Youch! And that doesn’t count the $10 a share it lost in the month before yesterday’s open. Shares of Hansen were up 332% in 2004, and 330% in 2005. The stock is “only” up 51% so far this year.

I wonder what would have happened if the company missed earnings. -

Why Interest Rates Are So Important

Eddy Elfenbein, August 7th, 2006 at 6:36 amOn Tuesday, the Fed will make its big decision on interest rates. If you’re new to investing, the direction of interest rates is extremely important to the stock market.

Stocks love falling rates, but rising rates act like Kryptonite. Consider these numbers:

Since 1960, the yield on the 90-day Treasury bill has risen on 1,201 weeks. If we islotate those weeks, the market has climbed a total of 144% which works out to 3.9% a year. But on the 1,107 weeks when rates have fallen, the market has climbed over 650%. That comes to 10% a year, or 2.5 times better than when rates are rising.

Rates have stayed the same on 121 weeks for a total return of 16.5%, or 6.8% annualized which is almost the exact average of the other two categories.

Short-term rates hit their lowest point on June 19, 2003 at just 0.79%, and have risen ever since. Since then, the S&P 500 is up 28.6% or 8.4% a year. -

Efficient Couch Market Hypothesis

Eddy Elfenbein, August 6th, 2006 at 9:32 pmI own Comfy Couch, the single most comfortable couch in the entire world. It’s plush and squishy and fits me juuusst right. Unfortunately, Comfy Couch is also the ugliest couch in the world. I’m serious, this thing is truly hideous.

Well, I felt the time had finally come to depart with Comfy Couch. Comfy Couch, you see, is getting on in years, and she’s just not what she was. (On a side note, I inherited Comfy Couch from Tobin Smith, one of the market mavens on Bulls & Bears.)

So I advertised Comfy Couch on Craig’s List under the “Free Stuff” section (“Ugly Ass Couch, Free!!”). I waited and waited, but no one wanted her. No e-mails, nothing. I even reposted the ad, but still there were no takers.

Soooo…I changed strategy. I posted the ad under the “For Sale” section (Ugly Ass Couch, $30!!).

Sold. That day.

Efficient market, my ass! It’s like economics, but…freaky.

You’re reading this, of course, on my free blog. Ah, irony! -

“Sometimes libertarians deserve to win an argument”

Eddy Elfenbein, August 6th, 2006 at 11:23 am

So says the Washington Post in its editorial on hedge fund regulation:There are three types of argument in favor of regulating hedge funds, and none is persuasive.

The first invokes systemic risk: If a hedge fund collapses, the banks that lent to it may collapse, too, causing a chain reaction through the financial system. This danger is real, but the banks that lend to hedge funds have a strong incentive to manage it by limiting their exposure to hedge funds and by monitoring the risks that the funds take. Since the Long-Term Capital debacle, this is what banks appear to be doing. Regulatory prodding has encouraged the banks to get smarter, though in some cases the rules perversely permit hedge funds to borrow more if they take on extra risk — an example of how oversight of this complex industry can backfire.

The second argument for regulating hedge funds is that they are havens of insider trading and other sorts of illegal manipulation. It’s true that some prominent cases of fraud involve hedge funds, but this isn’t surprising given their size. The law already empowers regulators to go after hedge fund managers who commit financial crimes. It’s not clear that extra regulations would add much.

The third argument for regulation concerns investor protection. The SEC suggests that by registering and inspecting hedge funds it can reduce the danger that investors will lose money. Some hedge fund managers are happy to accept this line: To reassure anxious clients, some choose to register with the SEC anyway, and they calculate that submitting to mild regulation now may be smarter than waiting until the political storm that would follow the scandalous blowup of a crooked player in their industry. But this is a case of hedge funds and their customers trying to ensure their reputations by gaining a regulatory seal of approval. The regulators should decline to become a security blanket. -

Mixed Market

Eddy Elfenbein, August 4th, 2006 at 11:19 amAP:

MarketWatch:

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His