Archive for May, 2008

-

Nicholas Financial’s Earnings

Eddy Elfenbein, May 9th, 2008 at 3:09 pmYesterday, Nicholas Financial (NICK) reported quarterly earnings of 20 cents a share. That’s for the company’s fourth quarter which ended on March 31. For the same quarter one year before, NICK earned 29 cents a share. Revenue dropped 6% to $12.7 million.

Yes, I still think this is an absurdly undervalued stock. For the entire fiscal year, NICK earned 94 cents a share. That still means the company is going for about seven times earnings. Nicholas Financial has now reported revenue increases for 18 straight years. -

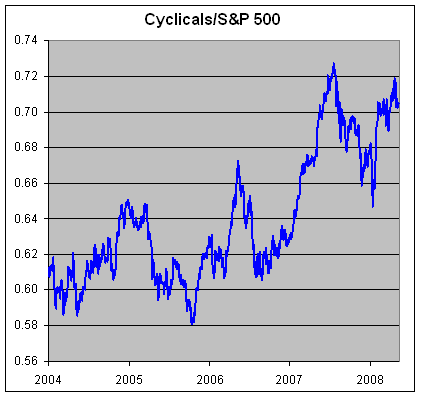

The Cyclicals are Still Overpriced

Eddy Elfenbein, May 7th, 2008 at 12:38 pmHere’s a look at something I wrote a lot about last year, it’s the ratio of the Morgan Stanley Cyclical Index (^CYC) to the S&P 500 (^GSPC):

The ratio peaked on July 19 and started falling for the next few months. It eventually reached a bottom on January 9 and has been steadily climbing ever since. -

Signs of Health in the Credit Markets

Eddy Elfenbein, May 7th, 2008 at 10:42 amIn the course of a three-and-a-half- hour dinner at Manhattan’s Smith & Wollensky steakhouse, Emil Assentato went from also-ran to the top of the world’s fastest-growing credit market.

By the end of the meal, Assentato, 58, the head of Cie. Financiere Tradition’s North American securities business who races cars on weekends, had persuaded more than a dozen credit- derivatives brokers led by Donald Fewer and Michael Babcock to defect from rival GFI Group Inc., court documents allege. In the end, 21 would leave for Tradition with the promise of $130 million over three to five years, about $6 million apiece.

Tradition’s attack did more than decimate GFI’s credit- default swap desk. It also raised the bar for the “extraordinary” pay commanded by derivatives brokers who match buyers and sellers between banks, according to affidavits filed by New York-based GFI in a suit against Tradition. As Wall Street buckles under the biggest credit-market losses in history, brokerage firms are seeking to tap the $10 billion of fees generated by middlemen, who spend as much as $500 million a year entertaining traders with strippers, football games and evenings at trendy Manhattan bars, based on court records and interviews with industry officials. -

Harry & David’s Withdraws IPO

Eddy Elfenbein, May 7th, 2008 at 10:37 amAnother victim of the stock market, Harry & David’s has withdrawn its IPO due to “market conditions.” Although the market has improved considerably over the past two months.

-

Looking at Inflation

Eddy Elfenbein, May 7th, 2008 at 9:37 amIn today’s NYT, David Leonhardt makes some interesting points about inflation. The things that are rising in price and the ones we pay most attention to. The ones that are flat or falling, we tend to ignore.

There is also something particular to inflation that aggravates loss aversion. Price increases are obvious. But price declines are often hidden. The cost of an item stays about the same for years, while everything else gets more expensive and nominal incomes rise.

When you dig into the Consumer Price Index, you start to realize just how many things fall into this category. The price of major appliances has been flat over the last year. Furniture is 1 percent less expensive. A decade ago, a basic four-door Toyota Corolla LE cost $16,018, according to the company. The 2009 basic model costs $16,650, and it’s a safer, more powerful, more fuel-efficient car than its predecessor.

To top it all off, most people don’t buy any of these items very often. “People tend to remember things they do frequently,” says Stephen Cecchetti, an economist at Brandeis University who studies inflation. “And what do you buy more frequently than gas and food?”

But combine the less noticeable trends with some true price declines, like a 5 percent drop in women’s clothing over the last year, and an inflation rate of 4 percent starts to seem more reasonable. Inflation really has gotten worse recently — it was only 2 percent a year and a half ago — but it’s not as bad as it feels.The whole idea of trying to measure inflation is a very difficult task. The reason is that if, say, chicken rises more than beef, consumers will start eating more beef and less chicken. In other words, as prices change, the weighting for each grouping changes.

-

The World’s First Billion Dollar Home

Eddy Elfenbein, May 6th, 2008 at 3:11 pm -

Shorting Puts

Eddy Elfenbein, May 6th, 2008 at 10:25 amI’ve always thought that shorting puts is a fascinating options strategy. A few years ago, I edited a book on the topic. Here’s part of the intro:

It then occurred to me that there is a great way to acquire stocks without trading what you’ve got or using borrowed funds. Simply stated, the method involves the sale of long-term options on highly rated companies, using the premiums received to further your investment program. There is no interest paid on the funds received; the funds never have to be repaid (because they have not been borrowed); and the equity requirements needed to do this are much lower than those for regular margin buying. Although I adapted and perfected this technique to suit my own needs and situation, it can be used by any investor who has built up some measure of equity and would like to acquire additional stocks without contributing additional capital. As we shall see later, the potential benefits far outweigh any incremental risks, especially when appropriate hedges and proper safeguards are incorporated.

What makes this technique so effective is that it exploits the fact that option prices do not reflect the expected long-term growth rates of the underlying equities. The reason for this is that standard option pricing formulas, used by option traders everywhere, do not incorporate this variable. With short-term options, this doesn’t matter. With long-term options, however, this oversight often leads the market to overvalue premiums. Taking advantage of this mispricing is the foundation of my strategy.

I have been using this technique for the past four years-very cautiously at first, because of the newness of these long-term options (they were only invented in 1990) and the almost complete lack of information regarding their safety and potential. It was this lack of analysis that led me to start my own research into the realm of long-term equity options. Having determined their relative risk/reward ratio, I am now very comfortable generating several thousand dollars a month in premiums which I use to add to my stock positions. I am often told that what I am doing is much akin to what a fire or hazard insurance company does, generating premiums and paying claims as they arise. A better analogy might be to a title insurance company, for with proper research, claims should rarely occur.Now I learn that Warren Buffett is using the same strategy:

Buffett arranged his multibillion-dollar positions by selling puts on these indexes. Berkshire will only have to make payments if the respective indexes fall below the levels they were issued at. “In the meantime, the premiums we have received are ours to invest freely,” Buffett says in the quarterly report. At the end of 2007, the conglomerate had $4.5 billion in premiums and $4.6 billion in liabilities.

Berkshire has continued to enlarge its position. In the first quarter, it increased premiums by 8.5%, or $383 million, by selling more puts, and increased its liability by 34.8% to $6.2 billion. Berkshire recorded a first-quarter loss on the contracts of $1.2 billion.

The indexes Buffett is bullish on haven’t fared well in the past year, given the turmoil in the credit markets. Over the last 12 months, the S&P 500 has fallen 7.9%, the FTSE dropped 4.1%, the Euro Stoxx is down 12.1% and the Nikkei has plunged 19.2%. His positions reveal that he is confident that the European, Asian and U.S. markets will move far higher in next 10 years and beyond.

Buffett warned that Berkshire’s earnings may “swing widely because of the accounting regulations that govern the reporting of derivatives contracts,” but that “that these contracts will prove profitable over the 15- to 20-year periods they cover, even if we exclude the investment income we can expect to earn on the $4.9 billion that we hold.” Buffett did not disclose the exact size of this global bet, only remarking that “we’re talking billions and billions and billions and billions of dollars of these things.” -

Morgan Stanley Is Being Sued Over James Brown’s Estate

Eddy Elfenbein, May 6th, 2008 at 10:19 amHow can you not like this story?

Brown’s estate has been at the centre of legal controversy. The 16-month scrap over his money has included allegations of embezzlement by some of his managers, wives, partners and offspring, as well as a fight over the veracity of the will.

It was drawn up by a lawyer who is serving 30 years in jail for murdering a strip-club dancer.

Two court-appointed trustees of Brown’s estate filed a lawsuit this week against Morgan Stanley at a court in South Carolina, the singer’s home state.

In court papers, the trustees allege that Joseph Lizzio, a Morgan Stanley banker who continues to work for the Wall Street group, breached his fiduciary duty to his client by failing to check with Brown whether an employee was allowed to withdraw funds from his account. -

Commodity Prices in Historical Perspective

Eddy Elfenbein, May 6th, 2008 at 10:06 amHere’s an interesting report on commodity prices from Wachovia. They point out that surges in commodity prices are fairly common. In fact, that latest rally pales in comparison to some recent rallies. The report also includes the CRB Index adjusted for inflation (Exhibit 2), a chart I’ve run a few times here. Over the long haul, commodity prices have consistently underperformed inflation.

-

Best Lede I’ve Read Today

Eddy Elfenbein, May 5th, 2008 at 3:12 pmFrom Reuters:

At least two analysts said Bank of America will likely lower its purchase price for Countrywide Financial , with Friedman, Billings Ramsey analyst saying the bank may bring down its deal price to the $0 to $2 level or completely walk away from the deal.

I like that: They’re lowering their offer to the $0 level. Didn’t that also happen in Godfather 2?

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His