Archive for February, 2009

-

Stocks Hate the Dollar

Eddy Elfenbein, February 20th, 2009 at 12:46 amA strong dollar used to be good for U.S. stocks, but since the credit crisis broke, that relationship has completely reversed itself.

Here are some numbers: Starting from the beginning of 1999 and going through September 17, 2008, on days when the dollar has rallied against the euro, the S&P 500 was up an annualized rate of 34.9%. But when the dollar fell against the euro or stayed the same, the S&P 500 dropped by an annualized rate of 26.7%. Stocks clearly liked a strong dollar.

Since September 18, the numbers are striking. On days when the dollars has rallied against the euro, the S&P 500 has fallen at an annualized rate of 95.7%. When the dollar has lost ground to the euro, the S&P is up by an amazing 747.5% annualized. Of course, that’s a much smaller sample size, but the early evidence suggests that stock investors now favor a weaker greenback. -

New York Times Suspended Dividend.

Eddy Elfenbein, February 19th, 2009 at 7:29 pmThe publisher said in a statement today it suspended its quarterly dividend of 6 cents a share to help reduce debt, three months after slashing the payout. It joins McClatchy Co., owner of the Sacramento Bee, and Media General Inc. in halting dividends.

The suspension will save New York Times about $34.5 million annually, based on shares outstanding. The publisher is cutting jobs and selling assets as advertising dwindles. It’s seeking buyers for its stake in the Boston Red Sox baseball team and is in talks about a sale-leaseback on its Manhattan headquarters.

“It’s going to be very challenging for them to generate much free cash flow even after this cut,” said Mike Simonton, a credit analyst at Fitch Ratings. “It’s certainly a prudent move to preserve liquidity in light of the difficult credit market and their heavy debt burden.”

New York Times fell 20 cents, or 5.4 percent, to $3.51 at 4:15 p.m. in New York Stock Exchange composite trading, before the announcement. The shares have declined 82 percent in the past 12 months.

“Today’s decision provides the company with additional financial flexibility given the current economic environment and the uncertain business outlook,” Chairman Arthur Sulzberger Jr. said in the statement. The Ochs-Sulzberger family controls New York Times and has benefited from the dividend on its Class B stock.Here’s the Times opining against cutting dividend taxes in 2003.

-

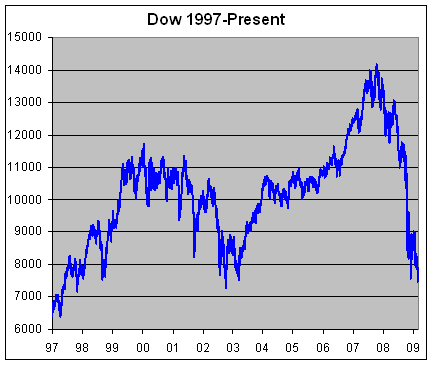

Dow Closes at 6-Year Low

Eddy Elfenbein, February 19th, 2009 at 4:35 pmThe Dow closed today at 7,465.95, its lowest close since October 9, 2002. The Dow is off 47% from its high of 14164.53 which came on October 9, 2007.

The Dow is now lower than where it was on June 9, 1997.

-

Irish Bank Workers Spat Upon

Eddy Elfenbein, February 19th, 2009 at 4:14 pmI hope your day is going better than this:

Irish bank workers are being spat at and threatened with physical violence by customers who are incensed at scandals in the industry, a union said on Thursday.

The IBOA, which represents over 20,000 workers in Ireland’s financial sector, said staff at banks had been facing growing abuse.

“We are seeing this kind of abuse not just in the working day but even socially in the evening,” said IBOA general secretary Larry Broderick.Same thing happened to John Rambo after the Nam.

(Via: Alea.) -

Santelli Calls for Tea Party

Eddy Elfenbein, February 19th, 2009 at 2:00 pmGrab your pitchforks. We have a leader.

-

Speaketh thy Beard

Eddy Elfenbein, February 18th, 2009 at 1:51 pmBen at the National Press Club. Here’s an excerpt:

Some observers have expressed the concern that, by expanding its balance sheet, the Federal Reserve will ultimately stoke inflation. The Fed’s lending activities have indeed resulted in a large increase in the reserves held by banks and thus in the narrowest definition of the money supply, the monetary base. However, banks are choosing to leave the great bulk of their excess reserves idle, in most cases on deposit with the Fed. Consequently, the rates of growth of broader monetary aggregates, such as M1 and M2, have been much lower than that of the monetary base. At this point, with global economic activity weak and commodity prices at low levels, we see little risk of unacceptably high inflation in the near term; indeed, we expect inflation to be quite low for some time.

However, at some point, when credit markets and the economy have begun to recover, the Federal Reserve will have to moderate growth in the money supply and begin to raise the federal funds rate. To reduce policy accommodation, the Fed will have to unwind some of its credit-easing programs and allow its balance sheet to shrink. To some extent, this unwinding will happen automatically, as improvements in credit markets should reduce the need to use Fed facilities. Indeed, where possible, we have tried to set lending rates and other terms at levels that are likely to be increasingly unattractive to borrowers as financial conditions normalize. In addition, some programs–those authorized under the Federal Reserve’s so-called 13(3) authority, which requires a finding that conditions in financial markets are “unusual and exigent”–will, by law, have to be phased out once credit market conditions substantially normalize. However, the principal factor determining the timing and pace of that process will be the Federal Reserve’s assessment of the condition of credit markets and the prospects for the economy.

A significant shrinking of the balance sheet can be accomplished relatively quickly, as a substantial portion of the assets that the Federal Reserve holds–including loans to financial institutions, temporary central bank liquidity swaps, and purchases of commercial paper–are short-term in nature and can simply be allowed to run off as the various programs and facilities are scaled back or shut down. As the size of the balance sheet and the quantity of excess reserves in the system decline, the Federal Reserve will be able to return to its traditional means of making monetary policy–namely, by setting a target for the federal funds rate.

Importantly, the management of the Federal Reserve’s balance sheet and the conduct of monetary policy in the future will be made easier by the recent congressional action to give the Fed the authority to pay interest on bank reserves. Because banks should be unwilling to lend reserves at a rate lower than they can receive from the Fed, the interest rate the Fed pays on bank reserves should help to set a floor on the overnight interest rate. Moreover, other tools are available or can be developed to improve control of the federal funds rate during the exit stage. For example, the Treasury could resume its recent practice of issuing supplementary financing bills and placing the funds with the Federal Reserve; the issuance of these bills effectively drains reserves from the banking system, thereby improving monetary control. As we consider new programs or the expansion of old ones, the Federal Reserve will carefully weigh the implications for the exit strategy. And we will take all necessary actions to ensure that the unwinding of our programs is accomplished smoothly and in a timely way, consistent with meeting our obligation to foster maximum employment and price stability. -

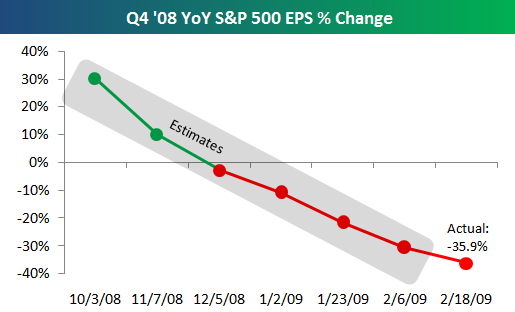

Analysts Were Way Off

Eddy Elfenbein, February 18th, 2009 at 12:29 pmI prefer to use trailing Price/Earning Ratios, though it’s not the only metric I use, when looking at stocks. The problem with forecasts is how far wrong you can be. The guys at Bespoke have tracked how poorly analysts did this past earnings quarter. Just four-and-a-half months ago, Wall Street saw a rosy future.

It’s actually worse than that. If I understand the chart correctly, it shows the sum of the previous four quarter earnings. Wall Street analysts weren’t even close this earnings quarter. -

Hedgies to Consolidate

Eddy Elfenbein, February 18th, 2009 at 12:25 pmFrom Bloomberg:

Hedge funds are looking to consolidate after record investment losses and customer withdrawals cut assets by 37 percent in the second half of 2008, squeezing their main source of fees. As many as 40 percent of the 9,000 hedge funds and funds of funds may disappear in the next two years, according to Karamvir Gosal, a New York-based investment banker at Jefferies Putnam Lovell. While some will return money to investors and shut their doors, mergers and acquisitions will be more prevalent than in the past.

“The conditions at the moment lend themselves to a surge in M&A activity in the hedge-fund world,” said Udi Grofman, a partner at Schulte Roth & Zabel LLP, a New York-based law firm that advises hedge funds. “We’ve already seen some players looking to take advantage of the low valuations and get their foot in the door, particularly when it comes to managers specialized in areas that are likely to be active in the near future, like mortgages and distressed debt.” -

Yesterday’s Close

Eddy Elfenbein, February 18th, 2009 at 12:23 pmThe Dow finished yesterday at 7,552.60 just 0.31 point above the November 20th close which was the lowest close since March 2003.

-

New York Times’ Share Price Less Than Sunday Newspaper Price

Eddy Elfenbein, February 17th, 2009 at 10:46 pmCheck out this very ugly chart:

Shares of NYT (NYT) dropped 29 cents today to close at $3.77. The Sunday paper goes for $4 at the newsstand.

Maybe they could save costs by printing the paper on their stock certificates.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His