Archive for October, 2009

-

Fannie Mae, Freddie Mac Price Targets Cut to $0

Eddy Elfenbein, October 19th, 2009 at 3:59 pmKeefe, Bruyette & Woods lowered its rating on Fannie (FNM) and Freddie (FRE) to $0.

They also downgraded the stock to “Underperform.” Of course, if you think it’s going to $0 that makes sense.

Both stocks trade a little over $1. -

S&P 1100

Eddy Elfenbein, October 19th, 2009 at 3:41 pmFor a very brief moment, the S&P 500 jumped over 1,100, saw its shadow and ran back below.

Someone’s been dumping lots of NICK today (and buying it as well). The stock is poised to have its biggest volume today in five months. The ask is currently at $6.88. I wouldn’t mind buying more if it goes lower. -

Rosenberg Rewrites History

Eddy Elfenbein, October 19th, 2009 at 2:13 pmIf you’re in the business of making market calls, you’re going to wrong. That’s just how it is. I’m wrong all the time. So is Jim Cramer. It happens. But I won’t tolerate someone trying to run away from their calls. There’s no excuse for that.

For the second time, David Rosenberg is trying to rewrite history and claim that he was neutral at the bottom. First he claimed it a few weeks ago and again today. As Joe Wisenthal points out, Rosenberg claims he “turned agnostic” in March.

Bullshit. That’s just complete bullshit.

Check out these stories.

March 9, 2009Merrill Lynch & Co.’s chief North American Economist David Rosenberg said today the S&P 500 may bottom out at 600 in October, lowering his estimate after the benchmark’s decline last week.

Based on the outlook for corporate profits and the typical trough P/E multiple that characterized recession bear markets, it would not surprise us to see the S&P 500 gravitate in a 475-650 range for an extended period of time.

At every point, Rosenberg discounted the rally (see here, here and here). After the market experienced a stunning rally, this is what he said in September.

I never did turn bullish enough at the lows, which is true. But I did turn neutral and while I did see the prospect of a complete throw-in-the-towel move towards 600 on the S&P 500, I can recall putting in print that the good news was that the bear market was about 95% over. Why quibble about another 60 points at that juncture. And, in the name of keeping an open mind, in my final report at Merrill Lynch, I played a game of Devil’s Advocate with myself … what if I was unduly bearish?

I didn’t stay bearish at the lows, which is contrary to popular opinion. I was basically neutral. And I continued to — still do, by the way — frame what we have experienced in the context of a bear market rally as opposed to the onset of a new secular bull market (the first you rent, the second you own). I am always skeptical of rallies that are purely premised on technicals and liquidity but bereft of a solid economic foundation. While green shoots did appear in the economic data, all the growth we have seen globally, and in the U.S.A. in particular, has come courtesy of unprecedented government stimulus. We see nothing organically in the economy to get us excited.I’ll quibble about 60 points because it was a lot more than 60 points. We’re now up more than 400 points since then and Rosenberg said that bottom could come in October (i.e. now).

You simply can’t say that you’re neutral but you see the prospects of a big move down. That statement makes no sense. It can be used to say anything, which is another way of saying it means nothing.

If the market were at a new low now, then I doubt Rosenberg would say he had truly been agnostic in March. -

Buy List +38%

Eddy Elfenbein, October 19th, 2009 at 12:28 pmThanks to today’s rally, the Buy List is up 38.2% for the year. Sysco (SYY), Danaher (DHR) and Cognizant (CTSH) are all at new 52-week highs. Eaton Vance (EV) hit one earlier today and Amphenol (APH) isn’t far behind. Nicholas Financial (NICK) has traded at $7 a share several times over the past two months but can’t seem to get one penny above it.

-

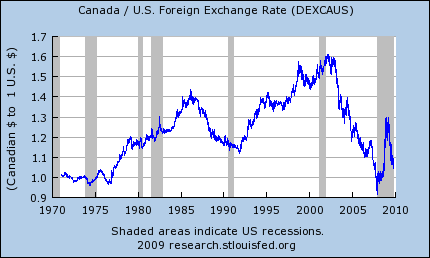

Loonie Closing in on Greenback

Eddy Elfenbein, October 19th, 2009 at 11:23 amWhile Wall Street is celebrating the Dow being over 10,000, there’s another milestone coming up: The Canadian dollar is about to reach parity with the U.S. dollar.

Seven years ago, a loonie was worth about 60 cents. -

Technical Analysis Strikes Out

Eddy Elfenbein, October 19th, 2009 at 11:17 amA new paper finds that technical analysis is pretty much a dud around the world.

Technical analysis is not consistently profitable in the 49 countries that comprise the Morgan Stanley Capital Index once data snooping bias is accounted for. There is some evidence that technical trading rules perform better in emerging markets than developed markets, which is consistent with the finding of previous studies that these markets are less efficient, but this result is not strong. While we cannot rule out the possibility that technical analysis compliments other market timing techniques or that trading rules we do not test are profitable, we do show that over 5,000 trading rules do not add value beyond what may be expected by chance when used in isolation.

(HT: Alea)

-

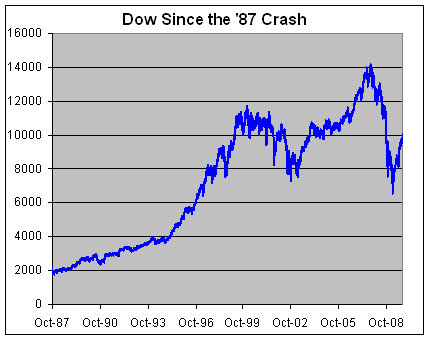

22 Years Since the 1987 Crash

Eddy Elfenbein, October 19th, 2009 at 11:02 amIt was 22 years ago today — October 19, 1987 –that the market busted. The Dow plunged 508 points, also on a Monday.

As it turned out, the crash was an excellent buying opportunity as the market can surging for another 12-1/2 years.

If you bought the day after the crash, you would have improved your annualized return by 1.25%. -

You Know It’s Bad…

Eddy Elfenbein, October 19th, 2009 at 12:46 am…when the Catholic Church files for bankruptcy.

Catholic Diocese of Wilmington files for Chapter 11

Catholic Diocese of Wilmington Inc filed for Chapter 11 bankruptcy protection, court documents showed.

In a filing with the U.S. Bankruptcy Court for the District of Delaware on Sunday, the diocese listed estimated assets in the range of $50 million to $100 million and estimated liabilities in the range of $100 million to $500 million. -

Time to Bury MPT

Eddy Elfenbein, October 18th, 2009 at 11:10 pmAny idea for ditching Modern Portfolio Theory gets a thumbs-up from me, and it gets two thumbs up if it’s from David Merkel.

David says it’s time to put MPT and beta in their grave. He suggests a “contingent claims theory.” If I have him right, we ought to view equity, not as a separate animal, but as simply the next point on the process of debt. Equity is the folks who get paid last so they get the highest yield.

I like the logic, but my question is—what if a firm has little or no debt?

Update: David responds:Good question. The total volatility of a firm can be broken up into three pieces: financial leverage, operating leverage, and sales volatility. Saturday’s piece dealt with financial leverage and its costs. An unlevered firm in the financial sense still possesses operating leverage and volatility of sales. Different unlevered firms have different costs of equity capital because they have different levels of sales volatility, and different degrees of operating leverage.

That will manifest itself in option implied volatility, which is a crude measure of what people would pay to gain and lose exposure to the equity of the company. The cost of equity should be positively related to that. More volatile companies should have a higher cost of equity.

Another way to look at it is to ask what is the effect on the firm if the company issues or buys back equity. How much does the generation of free cash flow change relative to the price paid or received for equity? -

We go to gain a little patch of ground that hath in it no profit but the name

Eddy Elfenbein, October 18th, 2009 at 2:26 pmChristopher Hitchens reviews Peter Hart’s The Somme: The Darkest Hour on the Western Front:

From Hart’s book I was able to learn and grasp (and even picture) the historic importance of the “creeping,” or perhaps better say “staggered,” barrage. The descriptions one has so often seen, of entire ranks and files of British infantry lying dead almost symmetrically, like so much freshly scythed wheat, are all true. But these men were being expended while the British artillery struggled to evolve a system of covering bombardment that “walked” in front of them, smashing trench after trench and clearing them a path. Painstakingly leading us through a series of terrible engagements, Hart succeeds in showing how the gunners got steadily better (as did the guns). He also succeeds in giving one an enhanced respect for the German soldiers who held positions under this unbelievable rain of fire and were still—almost always—ready to fight. Sometimes they were too stunned and deafened and dazed to do anything but surrender, or rather, try to do so. An unpleasantly recurrent theme in the diaries and letters of British soldiers—Niall Ferguson has also been able to be honest about this often-avoided question—is the casual or even gloating way in which the Tommys boasted of killing German prisoners.

In America, World War II is really the Great War, but I’ve become convinced that World War I was the worst thing to ever happen in the history of the world.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His