Archive for November, 2013

-

Another All-Time High

Eddy Elfenbein, November 15th, 2013 at 4:16 pmThe S&P 500 rallied into the close today. We finished the day at 1,798.18. This was our sixth-straight weekly gain. Our Buy List trailed the market today, gaining 0.32% to the S&P 500’s 0.42%.

-

Nirvana: MTV Unplugged

Eddy Elfenbein, November 15th, 2013 at 4:04 pmThis Monday marks the 20th anniversary of Nirvana’s famous concert on MTV Unplugged.

-

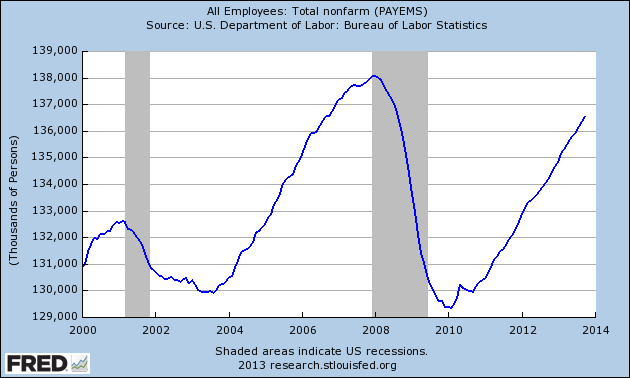

October Industrial Production Drops 0.1%

Eddy Elfenbein, November 15th, 2013 at 9:35 amThis morning, the Federal Reserve reported that Industrial Production fell 0.1% in October. That’s the first drop since July. IP is one of the data series that hasn’t topped its peak from 2007.

Wall Street had been expecting growth of 0.2%. The reading for September was revised to +0.7%. The IP number for October was 99.9778. The peak was 100.8200 from December 2007.

-

CWS Market Review – November 15, 2013

Eddy Elfenbein, November 15th, 2013 at 7:11 am“There are only two kinds of forecasters—those who don’t know, and

those who don’t know they don’t know.” – John Kenneth GalbraithThis has truly been a charmed stock market this year. On Thursday, the S&P 500 closed at 1,790.62, which is yet another record high. The index is now up 25.53% for the year, and it’s on track to yield its best yearly gain in a decade. The Nasdaq Composite is 25 points away from touching 4,000 for the first time in 13 years.

Last year, I thought I was being bold when I said the market could break 1,500 sometime in 2013. Sheesh, that happened before the Super Bowl, and now the S&P 500 is closing in on 1,800.

What’s remarkable about this year’s market is not only the stunning gain but also the absence of volatility. The market has gone up in a relatively steady manner. Consider that we haven’t had a daily drop of more than 1.6% in nearly five months. Compare that with the second half of 2011, when it happened 24 times. This Saturday will mark the one-year anniversary of the last time the S&P 500 closed below its 200-day moving average. As I said, it’s been a charmed market.

The market’s good fortune has led to a lot of talk, much of it careless, about the stock market being in a bubble. Even Janet Yellen was asked the great bubble question in her Congressional testimony (she said no). In this week’s CWS Market Review, I’ll take a closer look at where the market stands and investigate the issue of a possible bubble. Now that earnings season is past, this is a good time to take a step back and look at the larger picture.

I would be remiss if I didn’t point out that our Buy List continues to outpace the overall market. Through Wednesday, our Buy List beat the S&P 500 for eight straight days. This has been a very good earnings season for us. Since October 9, the Buy List has rallied 9.50%. We’re now up 33.64% on the year (not including dividends), which is 8% more than the S&P 500. This looks to be our seventh market-beating year in a row.

Now let’s turn to the broader market environment.

Is the Stock Market a Bubble?

The latest rage on Wall Street is to proclaim everything, particularly the stock market, a bubble. This is rather understandable when you consider it’s coming after two of the biggest blow-ups in Wall Street history: the Tech Bubble and the Financial Crisis. Naturally, the first sustained rally after these disasters would make anyone feel a bit nervous.

So do I think the market is in a bubble?

The answer is a bit complicated, but I’ll give you the simple version: I don’t know and I don’t care.

For one, it’s rather strange to discuss the stock market as if it were one entity. The stock market is composed of thousands of stocks. Even our Buy List, which is very diversified, contains just 20 stocks. In such a broad market, there will always be gems that the crowd overlooks. For stock pickers, that’s a good thing. I bet a monster-cap like ExxonMobil ($XOM) spends more on erasers than what little Harris ($HRS) earns in a full year. At Crossing Wall Street, we strive to be disciplined stock pickers, so the movement of the S&P 500 is of general importance to us, but it doesn’t alter our strategy of focusing on high-quality stocks going for good prices.

We should also remember that even if the stock market is overpriced, it’s still very hard to get the timing right. Lots of people were short the market going into the Financial Crisis, but it kept going higher and higher. If you’re disposed to see bubbles everywhere, then guess what: you’ll start seeing them everywhere. Remember, the trend is your frenemy. Momentum can always last longer than you expect. For example, I thought Ford Motor ($F) was a bargain at $15. I had no idea it was going to fall below $9 per share, as it did last year. As Lord Keynes famously said, “Markets can remain irrational a lot longer than you and I can remain solvent.” That’s painfully true.

Obviously, it would be great if we could always time the market perfectly, but we can’t. And no one can. I’ll go a step further. Even when disaster strikes, a buy-and-hold strategy can still serve you well. The S&P 500, including dividends, has performed reasonably well since mid-2008. That is, starting before the worst of the Financial Crisis. Time may not heal all investing wounds, but it sure can help a lot.

True market bubbles are very rare. By this, I mean to differentiate a bubble from a typical lousy market. The stock market drops every few years. That’s what markets do, and if you’re not prepared for it, you shouldn’t be in the stock market. Period. Stocks go up, and stocks go down. As Hyman Roth said, “this is the business we’ve chosen.”

The Two Kinds of Bear Markets

I think a good way of looking at bear markets is to divide them into two categories. One is where market prices shoot up far beyond values, and then reality reasserts itself. Those are your classic bubbles like 1987 or 2000. The other kind is where the value falls apart and then prices catch up. That’s what we had in 1990 and 2008. You might be surprised to hear me say that 2008 wasn’t a stock bubble. That’s true. There was a bubble in housing, but stock valuations were rather normal.

I very much doubt that we’re currently in a classic bubble. Earnings for the S&P 500 are expected to be about $107 per share (that’s an index-adjusted figure), and companies will probably pay out $35 per share in dividends. That works out to about 2%. Interestingly, the market’s dividend yield has hovered around 2% for much of the last decade, except for the most frightening parts of the Financial Crisis. Analysts currently expect the S&P 500 to earn about $121 per share next year. So even after our robust rally, the market is still going for about 14.8 times next year’s earnings estimate. That’s normal. We haven’t gone from normal valuations to sky-high ones. Rather, we’ve gone from duck-and-cover valuations to average ones.

Janet Yellen seems to agree. During her Congressional testimony this week, she was asked if the stock market was in a bubble. Yellen responded, “Stock prices have risen pretty robustly, but I think if you look at traditional valuation measures—the kind of things we monitor akin to price-equity ratios—you would not see prices that suggest bubble-like conditions.” Of course, investors should pay attention to more than a few easy-to-find ratios. But the general view indicates that equity valuations are quite normal.

Now the question that most concerns me is, are analysts too optimistic for the market’s future earnings? That’s a much more difficult question to answer, and if the answer is yes, then we have a different story. As I said, analysts see earnings coming in next year at $121, but I need to add that analysts don’t have an enviable track record with their forecasts (see the Galbraith quote above).

What concerns me most is that profit margins have grown very high and are near multi-decade highs. If (or when) we revert to the mean, then corporate profits will not grow as rapidly as the overall economy. However, the high margins may be a result of slow growth and ultra-low interest rates. We’ve never been in a situation quite like this, so the old rules may not apply.

Expect Small-Caps and Cyclicals to Lag

While I’m not a fan of market-timing, I do think it’s possible to spot areas that are due for outperformance or underperformance. In particularly, I’ve grown leery of the small-cap sector. Historically, small-cap stocks have done very well. The catch is that they’ve gone on long, multi-year runs of beating the market, then long runs of trailing. The current small-cap cycle began in April 1999.

Here’s a stunning fact: If the Dow had kept pace with the small-cap Russell 2000 since April 8, 1999, it would be over 28,000 today. I think investors should steer clear of macro bets on the small-cap sector. There are still many outstanding individual names there, but the sector as a whole needs to rest.

Related to small-caps are cyclical stocks. From a macro perspective, small-caps and cyclicals behave somewhat alike. This makes sense in that smaller companies tend to be more focused on domestic industries while mega-caps are skewed to large-scale multi-national service businesses. Cyclicals also tend to outperform when the market itself does well (hence the name “cyclicals”). Again, there are many individual cyclical names I like, such as Ford Motor ($F), but I expect the sector to lag the market for the next few years.

Updates on Some of Our Buy List Stocks

I want to caution investors not to expect more years like 2013. While I refuse to play the bubble guessing game, it’s certainly prudent for investors to grow more conservative as the rally goes on. Let’s take a look at a few of our Buy List stocks.

Despite missing earnings by one whole penny, AFLAC ($AFL) made back everything it lost and just rallied to another 52-week high. The duck stock announced that it’s expanding its buyback program by 40 million shares. Don’t chase this one. AFLAC is a good buy up to $70 per share.

FactSet Reseatch Systems ($FDS) just hit a new 52-week high. The stock is having a very good year. We’ll get another earnings report before the end of the year. I’m raising our Buy Below to $119 per share.

Several more of our stocks hit new 52-week highs on Thursday, such as Harris ($HRS), Fiserv ($FISV), Cognizant ($CTSH) and CA Technologies ($CA). So did WEX Inc. ($WEX), which was raised to a buy by Zacks. WEX looks to crack $100 per share any day now. I was impressed to see Oracle ($ORCL) hit $35 this week for the first time since May. Oracle continues to be a very good buy up to $35 per share.

Both Ross Stores ($ROST) and Medtronic ($MDT) made new highs on Thursday, and both stocks are due to report next week. I previewed their earnings reports in last week’s CWS Market Review. This week, I’m raising the Buy Below on Medtronic to $61 per share. Expect to see another solid earnings report this Tuesday.

That’s all for now. This Wednesday, the Commerce Department will report on retail sales. Also on Wednesday, the Labor Department will release the inflation report for October. Expect to see more subdued inflation. However, the most important release will be the minutes from the Fed’s meeting three weeks ago. As expected, the Fed decided to hold off tapering, but it will be interesting to see what issues the FOMC discussed. The Street is now expecting a tapering move in March. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: November 15, 2013

Eddy Elfenbein, November 15th, 2013 at 6:26 amEU Inflation Rate Falls to Four-Year Low

Ireland Is to Exit Its Bailout, and Without a Safety Net

Japan Drastically Scales Back Greenhouse Gas Emissions Target

Spain Free-for-All Pitting Apollo Against Blackstone

Yellen Says Stronger Job Growth a Fed Imperative

Moody’s Cuts Ratings of Four Major U.S. Banks

U.S. Trade Gap Widens More Than Forecast to $41.8 Billion

Retailers Less Than Cheerful Over Christmas Sales

Billionaire Paulson Sticks With Gold Wager as Prices Rebound

After Twitter #Fail, JPMorgan Calls Off Q. and A.

Maybe Snapchat Is Crazy To Turn Down $3 Billion, But Was Facebook Nuts To Offer It?

Cisco Sales Miss Casts Shadow Over CEO’s Turnaround Plan

Cullen Roche: A Wise Way For the Fed to Taper

Jeff Carter: The Fed Can Be Wrong

Be sure to follow me on Twitter.

-

Today’s News

Eddy Elfenbein, November 14th, 2013 at 2:22 pmThe following paragraph is all you need to know about today’s trading:

“Stock prices have risen pretty robustly but I think if you look at traditional valuation measures – the kind of things we monitor akin to price-equity ratios – you would not see prices that suggest bubble-like conditions,” Yellen said.

-

Janet Yellen’s Congressional Testimony

Eddy Elfenbein, November 14th, 2013 at 10:17 amHere’s Janet Yellen’s testimony. The Fed watchers think they’ve spotted a “dovish” angle which helped the market rise to an all-time high yesterday.

Chairman Johnson, Senator Crapo, and members of the Committee, thank you for this opportunity to appear before you today. It has been a privilege for me to serve the Federal Reserve at different times and in different roles over the past 36 years, and an honor to be nominated by the President to lead the Fed as Chair of the Board of Governors.

I approach this task with a clear understanding that the Congress has entrusted the Federal Reserve with great responsibilities. Its decisions affect the well-being of every American and the strength and prosperity of our nation. That prosperity depends most, of course, on the productiveness and enterprise of the American people, but the Federal Reserve plays a role too, promoting conditions that foster maximum employment, low and stable inflation, and a safe and sound financial system.

The past six years have been challenging for our nation and difficult for many Americans. We endured the worst financial crisis and deepest recession since the Great Depression. The effects were severe, but they could have been far worse. Working together, government leaders confronted these challenges and successfully contained the crisis. Under the wise and skillful leadership of Chairman Bernanke, the Fed helped stabilize the financial system, arrest the steep fall in the economy, and restart growth.

Today the economy is significantly stronger and continues to improve. The private sector has created 7.8 million jobs since the post-crisis low for employment in 2010. Housing, which was at the center of the crisis, seems to have turned a corner–construction, home prices, and sales are up significantly. The auto industry has made an impressive comeback, with domestic production and sales back to near their pre-crisis levels.

We have made good progress, but we have farther to go to regain the ground lost in the crisis and the recession. Unemployment is down from a peak of 10 percent, but at 7.3 percent in October, it is still too high, reflecting a labor market and economy performing far short of their potential. At the same time, inflation has been running below the Federal Reserve’s goal of 2 percent and is expected to continue to do so for some time.

For these reasons, the Federal Reserve is using its monetary policy tools to promote a more robust recovery. A strong recovery will ultimately enable the Fed to reduce its monetary accommodation and reliance on unconventional policy tools such as asset purchases. I believe that supporting the recovery today is the surest path to returning to a more normal approach to monetary policy.

In the past two decades, and especially under Chairman Bernanke, the Federal Reserve has provided more and clearer information about its goals. Like the Chairman, I strongly believe that monetary policy is most effective when the public understands what the Fed is trying to do and how it plans to do it. At the request of Chairman Bernanke, I led the effort to adopt a statement of the Federal Open Market Committee’s (FOMC) longer-run objectives, including a 2 percent goal for inflation. I believe this statement has sent a clear and powerful message about the FOMC’s commitment to its goals and has helped anchor the public’s expectations that inflation will remain low and stable in the future. In this and many other ways, the Federal Reserve has become a more open and transparent institution. I have strongly supported this commitment to openness and transparency, and will continue to do so if I am confirmed and serve as Chair.

The crisis revealed weaknesses in our financial system. I believe that financial institutions, the Federal Reserve, and our fellow regulators have made considerable progress in addressing those weaknesses. Banks are stronger today, regulatory gaps are being closed, and the financial system is more stable and more resilient. Safeguarding the United States in a global financial system requires higher standards both here and abroad, so the Federal Reserve and other regulators have worked with our counterparts around the globe to secure improved capital requirements and other reforms internationally. Today, banks hold more and higher-quality capital and liquid assets that leave them much better prepared to withstand financial turmoil. Large banks are now subject to annual “stress tests” designed to ensure that they will have enough capital to continue the vital role they play in the economy, even under highly adverse circumstances.

We have made progress in promoting a strong and stable financial system, but here, too, important work lies ahead. I am committed to using the Fed’s supervisory and regulatory role to reduce the threat of another financial crisis. I believe that capital and liquidity rules and strong supervision are important tools for addressing the problem of financial institutions that are regarded as “too big to fail.” In writing new rules, however, the Fed should continue to limit the regulatory burden for community banks and smaller institutions, taking into account their distinct role and contributions. Overall, the Federal Reserve has sharpened its focus on financial stability and is taking that goal into consideration when carrying out its responsibilities for monetary policy. I support these developments and pledge, if confirmed, to continue them.

Our country has come a long way since the dark days of the financial crisis, but we have farther to go. Likewise, I believe the Federal Reserve has made significant progress toward its goals but has more work to do.

Thank you for the opportunity to appear before you today. I would be happy to respond to your questions.

-

Morning News: November 14, 2013

Eddy Elfenbein, November 14th, 2013 at 6:52 amEuro Zone Economy Stagnates as Growth Slows in Germany

Top Japan Banks’ Second-quarter Earnings Leap Thanks to ‘Abenomics’ Bull Market

JPMorgan’s Fruitful Ties to a Member of China’s Elite

Spy Scandal Weighs on U.S. Tech Firms in China, Cisco Takes Hit

New Catfish Inspections Are Posing a Problem for a Pacific Trade Pact

Yellen Says Economy Performing Far Short of Potential

Rejecting Billions, Snapchat Expects a Better Offer

Swiss Chocolate Maker Barry Callebaut Opens Factory in Japan in Rare Foreign Investment Coup

Macy’s Reverses Lackluster Quarter, Helped by Ad Campaign

EADS Third-Quarter Profit Rises on Higher Airbus Jet Deliveries

Apple Sticks to Winning Script in Samsung Damages Retrial

Italy Investigates Apple for Alleged Tax Fraud

Investment Manager Explains Why 99.5% of Americans Can Never Win

Edward Harrison: The Deflationary Forward Guidance Threshold

John Hempton: The FDA, Statistics and Fundamentalism

Be sure to follow me on Twitter.

-

The Surge In Consumer Services

Eddy Elfenbein, November 13th, 2013 at 11:38 amHere’s something I didn’t anticipate (which is a large category of things). The Consumer Services Sector has soared over the past few years, and it’s gotten stronger every day.

What’s interesting is that this sector had basically kept up with the broader market for years. Starting in mid-2008, it started to break away. The index has barely taken a break in the last two years.

Note that this is the Dow Jones U.S. Consumer Services Index which is similar (I believe) to the what the S&P calls its S&P 500 500 Consumer Discretionary Index.

-

Morning News: November 13, 2013

Eddy Elfenbein, November 13th, 2013 at 6:12 amU.K. Unemployment Falls to 7.6% in Move Toward BOE Threshold

Central Banks Risk Asset Bubbles in Battle With Deflation Danger

House Stalls Trade Pact Momentum

Dollar Rises to 2-Month High Versus Yen on Fed Bets

Gary Gensler’s Successor Has His Work Cut Out for Him

It’s Getting Closer to Panic Time for Healthcare.Gov

Starbucks Concludes Packaged Coffee Dispute With Kraft

Baidu Faces Lawsuit Over Video Piracy

CNPC, PetroChina to Buy Peru Oil, Gas Assets From Petrobras for US$2.6 Billion

WTI Trades Near Five-Month Low as U.S. Supplies Seen Rising

Jos. A. Bank Tries to Look Like a Catch for Men’s Wearhouse

Rosneft Beats Rivals to Grab Enel’s $1.8 Billion SeverEnergia Stake

Samsung Says It Will Supply Half Of The Smartphones In Africa This Year

Joshua Brown: Everything You Need to Know About Stock Market Crashes

Epicurean Dealmaker: The Invention of Leisure

Be sure to follow me on Twitter.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His