Archive for August, 2014

-

The Stock Market Calms Down, For Now

Eddy Elfenbein, August 11th, 2014 at 12:45 pmThe stock market is up again today after a very good day on Friday. The S&P 500 hit a near-term low of 1,904.78 on Thursday. Today we’ve been as high as 1,944.90. Several of our Buy List stocks are doing well; Qualcomm, IBM and Bed, Bath & Beyond are all up more than 1% so far.

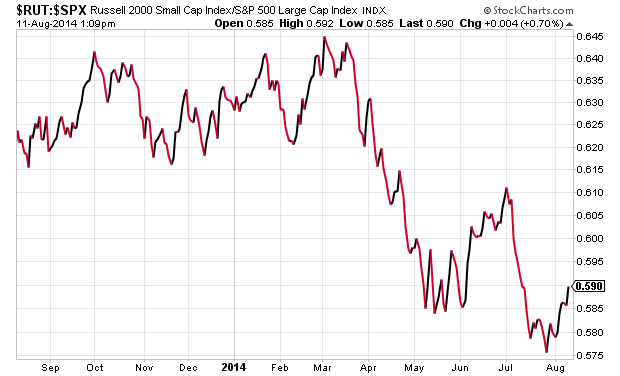

Small-caps are doing especially well today. The Russell 2000 is currently up 1.2%, which is more than double the S&P 500. Despite repeated predictions of its demise, the bond market continues to do very well. On Friday, the 10-year closed at 2.41% which is the lowest closing yield in 14 months. The yield is currently holding at 2.42%.

The stock market got quite nervous last week due to some geo-political tensions, but it seems that the threat has cooled off since then, though by no means has it gone away. The recent price action seems to be strongly related to a relaxation of tensions.

Check out this relative strength chart of the Russell 2000 divided by the S&P 500.

-

Morning News: August 11, 2014

Eddy Elfenbein, August 11th, 2014 at 6:59 amWar Risks Slow Company Bond Sales to Least Since July ’13

Food and Flirting; How Firms Learn to Live With China Antitrust Raids

Libor to FX Cases Drive Surge in Teamwork With Regulators

Stalled Gazprom Antitrust Case May Suggest Unease for Energy Sanctions

Wheat Bears Retreat as Black Sea Supply Risks Mount

Kinder Morgan to Consolidate Empire

Keystone XL Could Mean More Carbon Emissions than Estimated, Study Says

Balfour Beatty Rejects Two Merger Offers From Rival Carillion

Amazon Takes on Disney’s Superheroes in Online Fight

In a Fight With Authors, Amazon Cites Orwell, but Not Quite Correctly

Andreessen Horowitz Invests $50 Million in Buzz Feed

How Tiger Woods Becomes Zynga’s Last Hope for Glory

Treasury Wine Says Buyout Firm Matches K.K.R.’s $3.2 Billion Bid

Jeff Miller: Weighing the Week Ahead: The Market Risk from Current Crises

Epicurean Dealmaker: A Cure Worse Than The Disease

Be sure to follow me on Twitter.

-

CWS Market Review – August 8, 2014

Eddy Elfenbein, August 8th, 2014 at 7:26 am“Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.” – Peter Lynch

After a very subdued June and July, the stock market has suddenly gotten a lot more interesting. The S&P 500 had gone 62 trading days in a row without a daily move, up or down, of more than 1%. That was the longest streak of its kind in nearly 20 years. Then we had three such days within two weeks, and we came very close to a fourth on Tuesday.

On Thursday, the S&P 500 fell to a two-month low of 1,909.57. In an apparent homage to Black Monday, the index reached its closing high of 1,987.98 on July 24. We’re now down 3.94% from that mark. Last week, the S&P 500 broke below its 50-day moving average last week, and we’re only 2.6% above the 200-DMA. It’s been 21 months since the S&P 500 last closed below its 200-DMA.

There are lots of reasons for the market’s new-found case of anxiety: Ebola, Putin, Hamas, ISIS. From its July low to its August high, the Volatility Index ($VIX) soared 66%. Gold has been creeping up as well. Despite the increase in worrying, the fundamentals of the economy and stock market are sound.

Last Friday, for example, we had another good jobs report: the U.S. economy created 209,000 net new jobs in July. This is the first time in 17 years that the economy has created more than 200,000 jobs for six months in a row, and I think we can expect a seventh. On Thursday, the Labor Department reported that the four-week moving average of jobless claims fell to an eight-year low. We also learned last week that the ISM Manufacturing Index jumped to 57.1, which is its highest level in more than three years. There are lots of problems in the world, but an imminent recession in the U.S. isn’t one of them.

We’re nearing the end of second-quarter earnings season, and it’s mostly been a good one. Of the S&P 500 companies that have reported so far, 75% have beaten their earnings expectations, while 65% have beaten on sales. For Q2, the S&P 500 is on track to report earnings growth of 9.4% and sales growth of 4.2%. Despite all the loose talk of a new bubble, valuations haven’t changed much in the past year.

Our Buy List nearly made it through earnings season without a dud, but Cognizant Technology ($CTSH) had to ruin it for us. On Wednesday, the IT outsourcer beat estimates by four cents per share, but it lowered its sales guidance. Traders didn’t like that at all, and by the closing bell, CTSH lost 12.6%. I’ll have a complete rundown in just a bit (Spoiler Alert: I’m still a Cognizant fan.) I also want to review some Buy List members who may not make it onto next year’s list. We’re still a few months away from making our selections, but I want to share some thoughts with you. But first, let’s look at this newly volatile market.

What Are the Side Effects of QE?

Despite the big loss from Cognizant, our Buy List has been outperforming the overall stock market lately. Since we focus on high-quality stocks, we usually outperform the market during “worrying” stretches like we’ve seen recently.

Through Thursday, our Buy List is trailing the S&P 500 for the year (3.31% for the S&P 500 to -0.32% for us, not including dividends). Part of our underperformance this year is due to the rally being overfed by a lot of low-quality, crappy stocks. Even Janet Yellen recently said, while defending the overall market’s valuation, that “valuation metrics in some sectors do appear substantially stretched, particularly those for smaller firms in the social media and biotechnology industries.”

She’s absolutely right. Look at a stock like Amazon.com ($AMZN) which is down more than 23% from its high, and it’s still trading at 150 times next year’s earnings (the company will probably lose money this year). Last month, I mentioned the outrageous case of Cynk Technology ($CYNK). The shares are down 97% since then.

This is a paradox of the market. On one hand, we want to see lower-quality names do well so capital can reach marginal businesses (and borrowers). But we don’t want to see the trend go overboard and cause investors to leave the good stuff behind. That’s partly what happened during the Credit Bubble. I remember how our Buy List trailed the market in 2006 and kept slightly ahead in 2007. But once the Financial Crisis took hold and all those garbage stocks got called out, our Buy List fell far less than the market. We recovered much more quickly as well. Why? Because we never bought the junk, so when the House of Cards tumbled over, our relative performance was outstanding.

This leads me to one of the big questions on the minds of professional investors: what are the side effects of the Federal Reserve’s unprecedented policies? The Fed has kept short-term interest rates near 0% for a long time. Naturally, any Fed policy will distort the market. I think, too, that some investors view this phenomenon in overly sinister tones, but I tend to view it rather dispassionately. The central bank is powerful, and it’s trying to entice investors to be more confident. That’s not easy to do, and 0% interest rates is a start.

One side effect is that investors grew too fond of junk bonds. Since the start of July, junk bonds have taken a sharp turn for the worse, and that’s probably a healthy sign. This is an important sector for investors to watch, even if you’re not invested there, because it tells us how the marginal borrower is doing. When junk bonds perform as well as other bonds, or even outperform them, that’s usually an optimistic sign for the economy. It hints that business is going well, and will probably continue to improve. But again, it shouldn’t be used to fund shady operations.

I’m also concerned that low rates have made share repurchases too easy to resist. I have no problem with companies borrowing money to fund their operations. But I’m concerned that easy credit has allowed too many companies to boost their EPS, not by growing their earnings but by reducing their share count.

This has also been a lousy year for small-cap stocks, and I can’t help but think it’s related to the Fed’s winding down of QE. Not that smaller companies benefit from the bond buying, but they prosper as the risks have been partly covered by the Fed. Why not, then, go for more aggressive names? But since July 3, the small-cap Russell 2000 is down 7.3%, nearly twice as much as the S&P 500. Investors want more safety, and they’re willing to pay for it.

What does this mean for us? Investors should focus on higher-quality names, especially dividend payers. Some Buy List stocks I like right now include Ford Motor ($F), which is especially good below $17 per share. Oracle ($ORCL) is a bargain below $40 per share. Ross Stores ($ROST) can’t seem to catch a break, but if you’re able to get it under $65, you got a good deal. Earnings are due out soon. Now let’s take a look at our big flop of this earnings season.

Cognizant Technology Plunges after Earnings

On Wednesday, shares of Cognizant Technology Solutions ($CTSH) got nailed for a 12.6% loss. At one point, the shares were down 17% on the day. The interesting part is that their Q2 earnings were quite good. Cognizant earned 66 cents per share, which topped Wall Street’s consensus by four cents per share, and quarterly revenues rose by 16.5% to $2.52 billion.

What caused traders so much grief wasn’t the earnings; it was Cognizant’s guidance. Actually, it wasn’t the earnings guidance—that was the same. It was their sales guidance that caused so much grief.

For Q3, Cognizant now expects earnings of at least 63 cents per share. Wall Street had been expecting 65 cents per share. But the company is keeping their full-year guidance at $2.54 per share, which is the same as it’s been. For Q3 sales, Cognizant now expects a range between $2.55 billion and $2.58 billion. Wall Street had been expecting $2.66 billion. For full-year sales, CTSH lowered their growth rate from 16.5% to 14%.

Cognizant’s CEO Francisco D’Souza said, “Due to weakness at certain clients and longer-than-anticipated sales cycles for certain large integrated deals, we are adopting a more conservative stance for the remainder of the year and revising our 2014 revenue guidance to growth of at least 14% over the prior year, while maintaining our full-year non-GAAP EPS guidance of $2.54.”

I can hardly say that I’m worried about a company that’s beating earnings and growing its top line by 14%. After Wednesday’s damage, CTSH is going for about 17.5 times this year’s estimate, which is a very good price. To reflect the selloff, I’m lowering my Buy Below on Cognizant to $48 per share.

Potential Buy List Deletions

According to the rules of our Buy List, the 20 stocks are locked and sealed for the entire year. No matter how much I want to make a move, I can’t touch any of the stocks until the end of the year. As usual, I only add and delete five stocks.

Now that we’re in the middle of summer, I want to share some of my preliminary thoughts on which stocks may not be around next year. Please understand that these are early indications, and I may change my mind before December. This also doesn’t mean that I don’t like these stocks at the moment. They’re simply on the short list to be cut next year. Ideally, when I make the change at the end of the year, the decisions shouldn’t come as a big surprise to regular readers.

At the top of the list is DirecTV ($DTV). It’s here not because it’s done poorly, but because it’s done very well for us. Thanks to the deal with AT&T, it’s not clear how much longer DTV will go on as an independent company. I can’t make any predictions on the AT&T deal falling though, or when it might be completed, but I’d prefer to congratulate DTV, and move on to a new stock. DTV has been a big winner for us.

Unfortunately, CA Technologies ($CA) has been much weaker than I expected. Quarterly revenues have dropped for nine quarters in a row, and will be probably do so again. We’ve been patient with CA, but the company’s problems run deep. I like the rich dividend, but frankly, not much else.

Moog ($MOG-A) dropped sharply in February, but recovered very nicely this spring. The recent guidance, however, was not what I was expecting.

I haven’t given up on McDonald’s ($MCD). The stock is cheap, but the problems for the burger giant are bigger than I expected. I think management realizes this, but turning around a company of this size won’t be easy. I still like MCD, but I want to see signs of improvement.

Medtronic ($MDT) is a long-time favorite of mine, and the stock has done well for us. My concern is that the Covidien deal is a major undertaking, and the new entity will be quite different from the old Medtronic. I understand why Medtronic wants to do this deal, and it probably makes sense, but it may not be the company we want on our Buy List.

All 16 of the Buy List stocks with quarters ending in June have new reported earnings. There are only two Buy List stocks that have quarters ending in July, Medtronic ($MDT) and Ross Stores ($ROST). Medtronic is due to report on August 19, and Ross Stores will follow two days later. I’ll have more to say about both stocks next week. Before I go, I also want to lower my Buy Below on Qualcomm to $79 per share. The stock has continued to drift lower after the earnings report. I like QCOM a lot and expect it to recover.

That’s all for now. Next week will be a fairly slow week for economic reports. I’ll be curious to see Wednesday’s retail sales report. Consumer spending hasn’t been as strong as I’d like to see. On Friday, we’ll get the report on Industrial Production. The last three reports haven’t been that great. I’d like to see some improvement here. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: August 8, 2014

Eddy Elfenbein, August 8th, 2014 at 6:55 amShares, Dollar Sink as U.S. Authorizes Air Strikes in Iraq

Putin Seen Punishing Own People Not Foes With Sanctions

Trade Boost May Not Save German Economy From Q2 Contraction

BOJ Holds Stimulus as Weaker Economy Challenges Kuroda

What the Latest Economic Data Say About China’s Changing Growth Model

Dow Falls to Lowest Since April as Ukraine Tensions Grow

Foreign Investigators Say They Didn’t Know China Law

Ford Says July China Auto Sales Rise 2% Y/Y

Hannaford Parent Company a Rival Bidder for Market Basket

Is It Game Over for Zynga? Weak Second Quarter Earnings Scare Off Investors

Barnes & Noble Teams with Google on Book Delivery Push

CBS Revenue Falls But Profit Beats Forecasts

Lululemon Founder Agrees Not to Wage Proxy War, Advent Buys Stake

Roger Nusbaum: Income Investing Evolves, Volatility Doesn’t

Cullen Roche: America’s Frightening Lack of Retirement Savings…

Be sure to follow me on Twitter.

-

Investing by the Pool

Eddy Elfenbein, August 7th, 2014 at 11:18 amThe other day I was struck by the particular brilliance of one my tweets.

1. Screen for 3%+ divs. 2. Delete names with too much debt 3. Sit by pool.

— Eddy Elfenbein (@EddyElfenbein) July 15, 2014

Fortunately, Gunnar Peterson of the Motley Fool was kind enough to expand on what I said.

By insisting on a 3% dividend you limit your choices to companies that pay out over 50% more than the current S&P 500 dividend payout. Furthermore, this helps investors avoid speculative situations. Checking the debt level gives the investor a margin of safety, as the company’s balance sheet should be ready to weather tough times.

I’m not much of a fan of stock screeners. Perhaps screeners can be used as a first hurdle in selecting good stocks, but I think they’re too mechanistic.

Successful investing basically boils down to buying high-quality companies at cheap prices. The problem is that high-quality companies are usually rather expensive. The good part is that the stock market isn’t always so rational, and if you’re patient, you can eventually see a good stock at a low price. Again, if you’re patient.

Personally, I have a large Watch List of stocks that I keep an eye on. These are stocks that I’ve judged to be of superior quality. The Watch List is sort of the minor leagues for our Buy List. At the end of the year, if a Watch List stock falls to a cheap price, it then becomes a candidate for our Buy List.

Back to my tweet. The idea I tried to convey is that investors should focus on well-run companies going for good prices. The dividend yield part of the equation will generally, but not always, show us bargain stocks. Companies with low debt will generally, though not always, signal that they’re well run.

I ran a screen of just S&P 500 companies with dividend yields over 3% and zero long-term debt. The four companies I got were Paychex, Garmin, Coach and GameStop. But even that’s a little misleading because Garmin is on track to pay out more than 60% of its earnings as dividends. That’s nearly twice the rate of the S&P 500. Coach will probably pay out 70% and Paychex will be near 80%. Only GameStop is near reasonable territory at 36%, and there are serious questions about the sustainability of their business model.

Gunner ran a similar screen (thought he used low debt instead of zero debt) and came up with three stocks; AstraZeneca, Procter & Gamble and Unilever. He also wisely advises investors to be wary of any stock with a dividend yield greater than 6% or 7% and payout ratios over 70%. Honestly, there are a zillion different screens you can run, but it should always reflect the simple equation of high-quality and low cost.

-

Morning News: August 7, 2014

Eddy Elfenbein, August 7th, 2014 at 7:02 amDraghi Outlook Menaced by Putin as Ukraine Crisis Bites

Weak German Industry Output Adds to Signs of Second-Quarter Slowdown

Russia’s Putin Issues Retaliatory Ban on Food Imports

China Cracks Down on Messaging Apps

BofA Reportedly in $17-Billion Settlement Over Toxic Loan Securities

Nestle Announces Share Buyback as Emerging Markets Pick Up

Fox Tops Estimates With Film, Cable Unit Spurring Profit

Rio Tinto is Being Cruel Just Because It Can

Walglreen Feared IRS Scrutiny If Inversion OK’d

Deutsche Telekom Still Waiting for Acceptable T-Mobile US Bid

Dish Meets Estimates as Broadband Offsets Pay-TV Loss

Viacom Revenue Misses Estimates on Fewer Movie Releases

The Hottest Ticket in Tech for Companies Struggling With the Gender Gap

Joshua Brown: These Are the 10 Cheapest and 10 Most Expensive Stocks in the S&P 500

Jeff Carter: What’s It Take To Be Successful?

Be sure to follow me on Twitter.

-

Bank of America Finally Raises Its Dividend

Eddy Elfenbein, August 6th, 2014 at 11:41 amThis has been a rather unusual day so far on Wall Street. I often caution investors that announced mergers deals can fall through. Today we learned that Sprint is no longer trying to buy T-Mobile. The anti-trust issues were apparently too much. Also, 21st Century Fox has ended its bid to buy Time Warner. Both TWX and TMUS are down sharply this morning.

I’ve steered clear of Citigroup and Bank of America even though both banks appear to be cheap based on most valuation metrics. Before considering them, I’ve wanted to see them raise their dividends, but the Fed has kept a leash on that. For me, it’s a signal that the banks aren’t quite so risky.

BAC finally got approval to raise their quarterly payout from one penny per share to five cents per share. Based on yesterday’s close, the yield will rise from 0.26% to 1.32%. That’s better, but still not much. Citigroup still pays a penny per share even though the bank earned $4.39 per share last year.

The Commerce Department reported that the trade deficit dropped to $41.5 billion in June. That was less than forecast. Compared with the pre-recession peak, exports are up 18% while imports are up 2%.

-

Cognizant Plummets on Lower Guidance

Eddy Elfenbein, August 6th, 2014 at 10:36 amShares of Cognizant Technology Solutions ($CTSH) are getting hammered this morning after the company very mildly lowered its sales forecast (but reaffirmed earnings). The stock has been down as much as 17% this morning.

Cognizant actually beat its earnings forecast. For Q2, they earned 66 cents per share which was four cents better than Wall Street’s consensus. Quarterly revenues rose 16.5% to $2.52 billion, which was $10 million below forecast.

For Q3, Cognizant sees earnings of at least 63 cents per share. Wall Street had been expecting 65 cents per share, but the big miss is on revenues. For Q3, CTSH projects revenues to range between $2.55 billion and $2.58 billion. Wall Street had been expecting $2.66 billion.

Cognizant’s CEO Francisco D’Souza said, “Due to weakness at certain clients and longer than anticipated sales cycles for certain large integrated deals, we are adopting a more conservative stance for the remainder of the year and revising our 2014 revenue guidance to growth of at least 14% over the prior year, while maintaining our full year non-GAAP EPS guidance of $2.54.”

So the full-year earnings guidance stays the same, but the sales guidance is weaker. CTSH now sees revenues rising by 14%. That translates to sales of at least $10.08 billion. The previous guidance was for revenues of at least $10.3 billion, meaning growth of at least 16.5%.

The sell-off seems far greater than what the underlying news suggests. That can happen when a stock carries an unusually rich valuation (“priced for perfection”), but I don’t think that’s the case with CTSH.

-

We Suck at Math

Eddy Elfenbein, August 6th, 2014 at 10:10 amMorgan Housel has a great column on how people are terrible at perceiving risks:

We generally just suck at math.

Americans were widely worried about growing government spending in 2009. After the federal government passed a $3.5 trillion annual budget to mass protests, a group of economists asked 1,000 Americans a simple question: “How many millions are in a trillion?” Only 21% answered correctly. The rest either didn’t know or answered wrong. Most Americans were worried about spending $3.5 trillion, but most had no idea how much a trillion actually was.

People deal with statistical illiteracy by reacting with their gut. Sometimes that’s good — I don’t need to calculate risks to know that driving blindfolded is stupid. But it can be dangerous, too. It makes us overreact to things that seem dangerous only because they’re unknown, and underreact to things that are dangerous but look benign.

Financial adviser Carl Richards says “risk is what’s left over when you think you’ve thought of everything.” Wherever you’re not looking, or not thinking, that’s where it is.

-

Q2 2014 Earnings Calendar

Eddy Elfenbein, August 6th, 2014 at 10:09 amHere’s a look at the 16 Buy List stocks that end their reporting quarter in June.

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His