Archive for February, 2016

-

Cognizant Earned 80 Cents per Share for Q4

Eddy Elfenbein, February 8th, 2016 at 7:24 amThis morning, Cognizant Technology Solutions (CTSH) reported Q4 earnings of 80 cents per share which was two cents more than expectations. The company had previously said it expected earnings of at least 77 cents per share. Quarterly revenue rose 17.9% to $3.23 billion.

“We are pleased with our strong performance in 2015,” said Francisco D’Souza, CEO. “At a time when major technology shifts are disrupting all industries, clients are looking to a partner like Cognizant to work with them to create the winning business models of tomorrow at the intersection of the physical and digital worlds. Our investments in disruptive technologies, new business models and best-in-class delivery uniquely position us to enable clients to drive digital transformation at enterprise scale.”

For the year, Cognizant made $3.07 per share. Revenue rose 21.0% to $12.42 billion. A year ago, their initial guidance for 2015 was for earnings of at least $2.91 per share and revenue of at least $12.21 billion. Overall, 2015 was a very good year for CTSH.

Now for guidance. This is their first look at 2016. Cognizant sees Q1 earnings between 78 and 80 cents per share. For the year, CTSH expects earnings to range between $3.32 and $3.44 per share. That’s very light. In Friday’s newsletter, I said I was looking for something around $3.45 per share. Don’t worry. I think the company is lowballing expectations so they can raise them later on.

Cognizant expects Q1 revenue between $3.18 billion and $3.24 billion, and full-year revenue between $13.65 billion and $14.20 billion.

Update: CTSH is trading about 7% lower this morning.

-

Morning News: February 8, 2016

Eddy Elfenbein, February 8th, 2016 at 7:01 amOil Falls With Equities as Venezuela Tour Doesn’t Deliver Deal

China’s Foreign-Exchange Reserves Decline to $3.23 Trillion

National Bank Takes $119 Million Writedown on Maple Bank Inquiry

Yellen to Balance Confidence With Caution in Testimony

A Dying Breed: Currency Traders Are Left Out of New Wall Street

Net Neutrality Again Puts F.C.C. General Counsel at Center Stage

VW Plans to Make U.S. Diesel Owners an Offer They Can’t Refuse

LeapFrog to Be Acquired by VTech in Shake-Up for Toy Industry

EU Approves Schlumberger’s Cameron Takeover

U.N. Agency Seeks to End Rift on New Aircraft Emission Rules

Credit Suisse C.E.O. Asks for a Cut in His Bonus

Peyton Manning Just Gave Budweiser $3.2 Million in Free Ad Time

Bridgewater Executives Deny Report of Rift at the Hedge Fund

Jeff Miller: Is a Recession Looming?

Jeff Carter: Real Time Settlement, A Unique Piece of The BlockChain

Be sure to follow me on Twitter.

-

The Weakness in Semiconductors

Eddy Elfenbein, February 5th, 2016 at 8:44 pm -

January NFP +151K, Unemployment 4.9%

Eddy Elfenbein, February 5th, 2016 at 8:30 amThe February jobs report is out. Last month, the U.S. economy created 151,000 net new jobs. That’s not very strong. The unemployment rate dropped to 4.9%. That’s an eight-year low.

NFP growth has gradually decelerated for the last year.

-

CWS Market Review – February 5, 2016

Eddy Elfenbein, February 5th, 2016 at 7:08 am“There are two times in a man’s life when he shouldn’t speculate:

when he can afford to and when he can’t.” – Mark TwainThis is shaping up to be a very good earnings season for our Buy List stocks. We’ve had 12 earnings reports so far; eleven topped Wall Street’s consensus, while one merely met consensus. Guidance for 2016, however, is a mixed bag.

In this week’s CWS Market Review, I’ll cover our latest round of earnings reports. I’ll also preview our one earnings report coming next week. I’ll also talk about the wave of negative interest rates sweeping the world.

The world may be on the brink of a currency war where it’s a massive race to the bottom. This is a dangerous game with no winners. I’ll talk about what it means for our stocks. I’ll also update you on some news impacting our portfolio. But first, let’s look at the slowly emerging currency war.

Currency Wars, Begun They Have

Last week, the Bank of Japan shocked the financial world by cutting interest rates to -0.1%. In other words, savers have to pay for the trouble of lending their own money. The economy there is still a mess and the government has tried just about everything to get things moving again.

It’s a controversial policy. The Bank of Japan approved the new policy by a vote of five to four. Even retired slugger Jose Canseco criticized the idea. But the real fear of negative rates is that it could spark a currency war.

Let me explain. Governments know they can give a shot in the arm to their economies by letting their currencies fall. That helps their exports. The trick is that their currency must decline relative to their trading partners. If they respond by lowering their currencies, well…then the effect is lost. Worse still, it could trigger a cycle of competitive devaluations where everybody joins in. That’s a game nobody can win.

In Europe, for example, Mario Draghi has done just about everything to get the Eurozone moving again. He’s followed the Fed’s script—he’s lowered rates below 0%, he’s bought bonds. So what’s been the effect of all this? The euro’s actually been getting stronger. It’s not due to Draghi’s lack of effort. It’s that other countries have struck back.

Later on, I’ll cover our recent Buy List earnings reports, and you’ll notice a theme. Companies are reporting sales and earnings, and they’re also noting what sales and earnings would have been if the dollar weren’t so darn strong. (Funny, they never credit a weak dollar when it boosts their sales.) But it’s not that the dollar is strong. Rather, it’s that everybody else is doing their best to weaken their own currencies. The U.S. dollar right now is kind of like being the world’s fastest turtle.

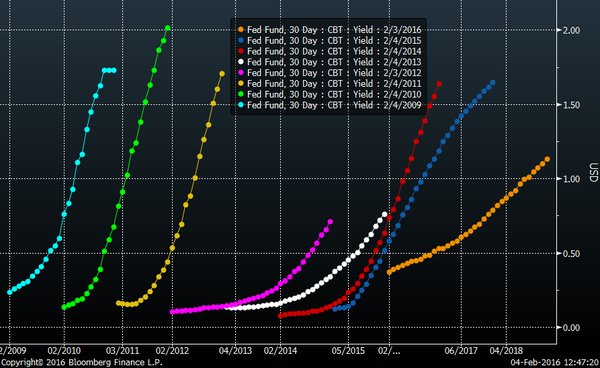

The effect on financial markets is profound. For the last six years, Wall Street has expected the Fed to raise rates at any minute, and they’ve been wrong, wrong and wrong (see the chart below via Charlie Bilello). That is, until a few weeks ago when they were right and the Fed finally raised rates. But now, Wall Street has begun to realize that the Fed isn’t going to continue raising rates despite some bold talk from Janet and her friends at the central bank.

The futures market has given up on the idea of another rate hike this year. At best, they see another rate hike (maybe) in 2017. Some folks think the Fed’s next move may even be a cut. I don’t know about that but the issue is clear. The strong dollar has already done much of the Fed’s work for them. In fact, now that pressure is off the Fed, the dollar finally took a big hit this week. On Wednesday and Thursday, the greenback suffered its worst two-day drop in seven years.

You can really see the effect when we compare yields in the U.S. with yields in Europe. In the U.S., the two-year Treasury yields about 0.7%. But in Europe, oh dear lord! In France, their two-year yields -0.4%. In Germany, it’s -0.5%. And in Switzerland, the two-year yields -0.9%. Here’s my favorite stat: In July 2011, Ireland’s two-year was going for 23%. Today it’s -0.34%.

What does this mean for stocks? The weak dollar is good for cyclical stocks like Energy, Transports and Materials. Those areas have suffered so long and it’s far too early to say that the dollar is in a prolonged slide. Investors should continue to focus on high-quality stocks, especially ones that can prosper in any environment.

In a bit, I’ll tell you about Fiserv (FISV) which has increased its earnings by double digits for 30 straight years. Investors should also focus on rich dividends. For example, Ford Motor (F) is a strong company that currently yields 5.2%. That’s nearly three times the 10-year Treasury’s yield. Now let’s take a look at some of our earnings reports from this week.

Four Buy List Earnings Reports

On Monday, AFLAC (AFL) reported Q4 operating earnings of $1.56 per share. That was a very good report, and it beat Wall Street’s consensus by nine cents per share. The earnings report was also at the top of the company’s own range for Q4 of $1.36 to $1.56 per share. Remember that with insurance companies, it’s better to look at their operating earnings rather than net earnings.

In Q4, the weak yen cost the duck stock five cents per share. That’s bad, but it’s much less than the damage inflicted in previous quarters. For the year, AFLAC made $6.16 per share, which exactly matched what it made in 2014; the weak yen knocked 46 cents per share off their full-year earnings. In currency-neutral terms, AFLAC grew its operating EPS by 7.5% last year. That’s not bad. The original guidance was for 2% to 7%. In July, they raised it to 4% to 7%. Overall, AFLAC performed well in a difficult environment.

AFLAC is a top-notch firm, but it’s a tough business to be in when the yen is sinking and interest rates are microscopic. The company continues to gobble up large amounts of stock. For Q4, their share count was almost 5% lower than it was one year ago.

For 2016, AFLAC said it expects operating EPS to range between $6.17 and $6.41. That assumes a value for the yen of 120.99 to the dollar. AFLAC detailed the yen’s expected impact on its guidance. I’ll simplify it for you.

Basically, for every one yen the Japanese currency strengthens against the dollar, meaning the ratio goes down, three cents per share are added to AFLAC’s profits. For every one yen it weakens, meaning the ratio rises above 120.99, about 2.5 cents per share are taken away.

Please understand that I didn’t add AFLAC to our Buy List based on any outlook for the yen. That’s impossible to predict. I added AFLAC because it’s a well-run outfit, and it’s an easy prediction to say that it will continue to be well run. This week, I’m lowering my Buy Below AFLAC to $63 per share.

On Tuesday, Fiserv (FISV) reported Q4 earnings of $1.00 per share, which matched Wall Street’s estimate on the nose. Fiserv’s report was our first non-beat this earnings season. All nine previous reports, plus the two since then, beat Wall Street’s estimate.

Fiserv had already told us that Q4 earnings would range between 98 cents and $1.01 per share. When a company like Fiserv gives you a narrow range like that, you can be pretty sure it’s going to be accurate. The company was able to grow its EPS 12% over last year’s Q4.

For the entire year, Fiserv earned $3.87 per share. That’s up 15% from the $3.37 per share they made in 2014. Here’s an amazing stat: This was Fiserv’s 30th consecutive year of double-digit earnings growth. That’s truly remarkable. It’s not the most exciting stock, but Fiserv delivers the goods.

Now let’s look at guidance. For 2016, Fiserv expects internal-revenue growth of 5% to 6%, and they expect earnings to range between $4.32 and $4.44 per share. That represents a growth rate of 12% to 15%, so they should keep their double-digit streak alive. The stock has gained back much of its December slide, and it may strike a new high soon. For now, I’m keeping my Buy Below for Fiserv at $103 per share. This is simply one of the best companies out there.

On Thursday morning, Snap-on (SNA) reported Q4 earnings of $2.22 per share, which beat Wall Street’s consensus by four cents per share. That’s an increase of 12.7% over last year’s Q4. Revenue growth, however, was slight. Snap-on’s “organic sales” rose by just 3.1%. That probably reflects some of the manufacturing slowdown that hit the U.S. economy towards the end of last year.

Still, this was another solid year for Snap-on. Organic sales rose 7.1% for the year, and the company made $8.10 per share. That’s a 13.4% increase over 2014. Digging through the numbers shows that Snap-on’s Commercial and Industrial Group was the weak link; organic sales fell by 0.3% last quarter. But the Tools Group, which is Snap-on’s largest, saw organic sales rise by 8.7%.

Snap-on’s outlook for this year was vague. They expect a tax rate this year similar to what they saw in 2015. They also expect to have capital expenditures of $80 million to $90 million. I think Snap-on should be able to earn $9 per share this year, but I’ll have a better idea as the year progresses. The stock got dinged for a 5.2% loss on Thursday. I’m lowering my Buy Below on Snap-on to $158 per share.

After the closing bell on Thursday, Stericycle (SRCL) reported Q4 earnings of $1.11 per share. That beat Wall Street’s consensus by one penny per share. This was a good quarter for Stericycle. Quarterly revenues rose 31.2% to $888.3 million. Adjusting for currency, revenues were up 35.2%.

For the whole year, Stericycle earned $4.40 per share. Revenues rose 16.8% to $2.99 billion. Adjusted for currency, revenues were up 21.2%. The company has previously said it expects earnings for 2016 to range between $5.28 and $5.35 per share. I’m lowering my Buy Below on Stericycle to $125 per share.

Earnings Preview for Cognizant Technology Solutions

We only have one Buy List earnings report next week. Cognizant Technology Solutions (CTSH) is due to report Q4 earnings on Monday, February 8, before the opening bell. The IT outsourcer has been doing quite well. In fact, this company offers a good lesson in why I prefer to invest in high-quality stocks.

A year ago, Cognizant’s initial guidance for 2015 was for earnings of at least $2.91 per share. At the time, that news disappointed Wall Street, as analysts had been expecting $2.96 per share. But Cognizant stuck to its game. They consistently beat earnings and raised guidance throughout the year.

In May, Cognizant raised guidance to at least $2.93 per share. Then in August, they raised it to at least $3.00 per share. Finally, in November, Cognizant said they expect earnings of at least $3.03 per share.

So, a year ago, Wall Street thought it had been too optimistic on CTSH, when in reality, they hadn’t been optimistic enough. For Q4, Cognizant expects earnings of at least 77 cents per share. That sounds about right to me. Look for 2016 earnings guidance of around $3.45 per share.

Buy List Updates

I wanted to pass along a few updates on some of our Buy List stocks. In last week’s CWS Market Review, I mentioned the strong earnings report from CR Bard (BCR). This is a good company, and they finished up a solid year for 2015 by making $9.08 per share. I also wanted to mention their guidance for 2016. Bard said they expect 2016 earnings to range between $9.90 and $10.05 per share. That’s growth of 9% to 11%. My Buy Below was a bit too high for Bard, so this week I’m lowering it to $199 per share.

Shares of Ford Motor (F) fell again this week. The automaker said that January sales fell by 3%, but some of that was due to weather and strong sales a year ago. Ford also said it’s going to cut jobs in Europe. That region has been a difficult one for Ford. While Europe provides about one-fifth of Ford’s revenue, they had operating margins of just 1% last year. Ford said they’re going to concentrate on higher-priced models in Europe, which is a smart move. This week, shares of Ford came close to breaking below $11. On Wednesday, Ford closed at a three-year low. I still say to wait this one out. Ford remains a buy up to $13 per share.

In October, I wrote, “I think it’s possible they could do a major deal soon”—“they” being Stryker (SYK). I suppose I was on to something. This week, Stryker announced that it’s buying Sage Products for $2.775 billion.

According to Stryker, “The transaction includes an anticipated future tax benefit which is expected to exceed $500 million and to positively impact cash flows over approximately 15 years.” In other words, more money for them. Stryker raised its full-year EPS guidance by five cents at both ends. The new range is $5.55 to $5.75 per share. They said they hope the deal closes during Q2. Stryker remains a buy up to $101 per share.

Hormel Foods (HRL) will be splitting its stock 2-for-1 next Wednesday, February 10. Shareholders will then have twice as many shares as the share price is cut in half. Our Buy Below price will split along with the stock. That means that the post-split Buy Below price will be $41 per share. Earnings are due out on February 16.

Investor’s Business Daily had a good article on Ross Stores (ROST). They pointed out some key facts that many investors overlook. For example, Ross is one of the few retailers that’s relatively impervious to Amazon. I think some analysts don’t get that Ross has carved out a special niche in the deep-discount market. They’re really not in competition with many other retailers. Check out the whole article.

Wells Fargo (WFC) agreed to pay $1.2 billion to settle a government lawsuit about its FHA home-mortgage program. Wells said that will reduce its 2015 earnings by three cents to $4.12 per share. That’s not pleasant news, but the damage has been done and it’s a very small part of their business. Wells is a buy up to $52 per share.

That’s all for now. There are still more earnings reports next week. We’ll also get important economic reports on wholesale inventories (Tuesday), initial jobless claims (Thursday) and retail sales (Friday). Also, remember that Hormel Foods splits 2-for-1 on Wednesday. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: February 5, 2016

Eddy Elfenbein, February 5th, 2016 at 7:02 amWorld Stocks Drift as Fed Watchers Await US Job Data

German Factory Orders Fall as Export Slowdown Cools Confidence

Brazil’s Recession Is Crashing Its Biggest Party

Obama’s Seriously Bad Oil Tax For Transportation Infrastructure: The Hypothecation Violation

China Insurance Purchase Curb Extended to Visa, MasterCard

LinkedIn -27.5% Due to Guidance; Field Sales Growth Expected to Slow, Acquisition Announced

Toyota Stays on Track to Report 3 Trillion Yen in Annual Profit

ArcelorMittal to Raise $3 Billion After Chinese Steel Exports Hit Profits

Volvo Readies For U.S. Slowdown as Fourth-Quarter Profit Just Lags

Monsanto to Focus on Technology as Syngenta Merger Slips Away

Despite Billions in Fresh Cash, Symantec Will Cut Costs and Go Into Debt

Mattel, Hasbro Would Face Rising Antitrust Worry Over Mega Deals

Roger Nusbaum: Taking Ownership of Your Retirement Outcome

Cullen Roche: Why Do Corporations Pay Dividends?

Be sure to follow me on Twitter.

-

IBD on Ross Stores

Eddy Elfenbein, February 4th, 2016 at 4:27 pmNice article today on Ross Stores (ROST) from Investor’s Business Daily: Ross Stores: A No-Nonsense Retailer Free From Amazon’s Clutches

It doesn’t have an online shop. It doesn’t promise luxury brands. And its fluorescent lighting and long, uninterrupted racks of merchandise aim in no way to replicate the glossy feel of a Bloomingdale’s or Macy’s.

But Ross Stores (ROST) is widely considered a solid, if not particularly flashy, find as other retailers struggle against the Web tide, and as shoppers increasingly take their business to off-price channels.

“They are so well positioned. They’re one of the best,” Morningstar analyst Bridget Weishaar said of Ross, adding that the off-price industry overall has hit the “sweet spot of pricing and distribution.”

Check out the whole article. They explain how Ross is impervious to Amazon. The store is also safe from weather-related issues that can wreak havoc on the inventories of other retailers.

-

Snap-on Beats Earnings by Four Cents

Eddy Elfenbein, February 4th, 2016 at 7:48 amSnap-on (SNA) earned $2.22 per share for Q4. That was four cents better than estimates. For the year, the company earned $8.10 per share which is up from $7.14 in 2014.

“For full-year 2015, Snap-on achieved organic sales growth of 7.1% and diluted earnings per share increased 13.4%, once again validating Snap-on’s ability to build upon its unique combination of capabilities in serving serious professionals and to successfully navigate our runways for coherent growth and operating improvement,” said Nick Pinchuk, Snap-on chairman and chief executive officer. “Our fourth quarter results, including 3.1% organic sales growth, a 19.1% operating margin before financial services, and a 12.7% increase in diluted earnings per share, represent an encouraging finish to 2015 and demonstrate ongoing progress along these runways while overcoming meaningful and continuing external headwinds. As we enter 2016, we believe that we’ll further strengthen our position with professionals performing critical tasks by enhancing the franchise network, expanding in the vehicle repair garage, extending to critical industries and building in emerging markets. At the same time, we remain committed to taking advantage of the opportunities for ongoing operating improvement through our Snap-on Value Creation Processes in the areas of safety, quality, customer connection and rapid continuous improvement. Finally, our progress in 2015 would not have been possible without the capability and commitment of our franchisees and associates, and I thank them for their dedication and their contributions.”

-

Morning News: February 4, 2016

Eddy Elfenbein, February 4th, 2016 at 6:46 amEuropean Growth Seen as Slower Than Previously Predicted

Six Oil Producers Agree on Emergency Meeting, Iran’s Shana Says

Bond Markets Are Underestimating the Fed, Goldman and Pimco Warn

U.S. Airlines Are Letting Flight Crews Avoid Zika Zones

Credit Suisse Posts First Loss Since 2008, Sees Tough Markets

Royal Dutch Shell’s Profit Down 56% on Slumping Oil Prices

Amazon Plans Hundreds of Brick-and-Mortar Bookstores, Mall CEO Says

Sharp Chooses Foxconn as Preferred Bidder Over Japan Fund

Wells Fargo Agrees to Pay $1.2 Billion to Settle FHA Claims

Emaar Chairman Leads Investor Group Buying Americana Stake

Toshiba Widens Full-Year Net Loss Outlook

GoPro Earnings Plunge After New Camera Fails to Impress

Does a Company Have To Disclose When a Top Executive Has a Serious Medical Problem?

Jeff Miller: The Costly Craving for Explanations

Howard Lindzon: Can the 8-80 Brands and Services Save the Market? …and My Gameplan

Be sure to follow me on Twitter.

-

Note on Yesterday’s Market

Eddy Elfenbein, February 4th, 2016 at 2:30 amI wanted to touch on yesterday’s market action because it was so unusual. The S&P 500 gained 0.50% on Wednesday but there was a very wide divergence within the market.

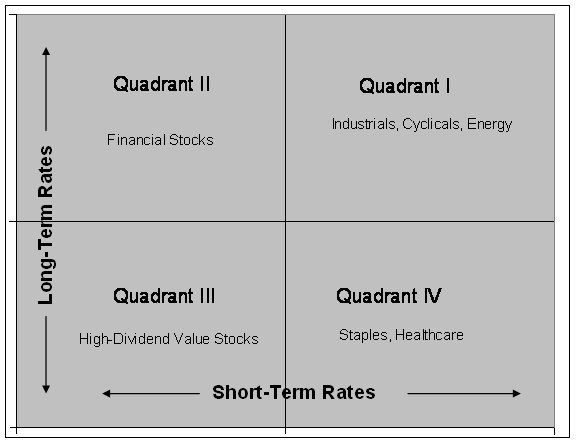

The S&P 500 Value stocks gained 1.02% while the Growth stocks gained just 0.01%. The other divergence can be seen among the cyclicals. The Energy stocks in the S&P 500 gained 3.96% while the Materials stocks were up 3.33%. That’s a big gap between them and everyone else.

This is an important point that I stress to investors: different categories of stocks move in different ways. The cyclicals represent one node of the market. Mostly these are Energy and Materials stocks. Industrials are their closest cousins. Not surprisingly, the Industrials did fairly well today with a 1.51% gain.

Here is the matrix I’ve used to describe how the market generally moves. Yesterday was a classic Quadrant I day.

Long-term yields moved slightly higher on Wednesday while short-term yields were largely unchanged. I should add that the Energy and Materials stocks did well yesterday after doing very poorly for the last several months. The Industrials have been underperforming for about 20 months.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His