Archive for August, 2016

-

Duncan Weldon Eats His Shoes

Eddy Elfenbein, August 7th, 2016 at 5:47 pm -

Q2 2016 Earnings Calendar

Eddy Elfenbein, August 5th, 2016 at 9:25 amSixteen of our 20 Buy List stocks reported Q2 earnings throughout the past month. Here’s a list of reporting dates, Wall Street’s consensus estimates and actual reported results:

Company Ticker Date Estimate Result Wells Fargo WFC 15-Jul $1.01 $1.01 Microsoft MSFT 19-Jul $0.58 $0.69 Signature Bank SBNY 20-Jul $1.97 $1.90 Alliance Data ADS 21-Jul $3.59 $3.68 Biogen BIIB 21-Jul $4.67 $5.21 Snap-on SNA 21-Jul $2.23 $2.36 Stryker SYK 21-Jul $1.37 $1.39 Express Scripts ESRX 25-Jul $1.57 $1.57 Wabtec WAB 25-Jul $1.08 $1.05 CR Bard BCR 26-Jul $2.47 $2.54 AFLAC AFL 28-Jul $1.68 $1.71 Ford Motor F 28-Jul $0.60 $0.52 Stericycle SRCL 28-Jul $1.18 $1.18 Cerner CERN 2-Aug $0.57 $0.58 Fiserv FISV 2-Aug $1.07 $1.08 Cognizant Tech CTSH 5-Aug $0.82 $0.87 July Jobs Report = +255K

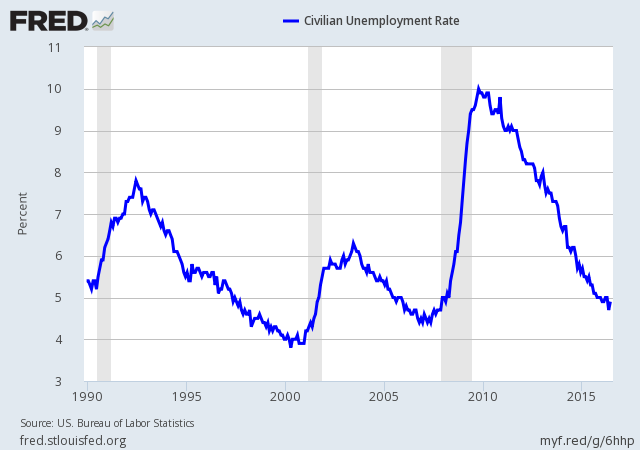

Eddy Elfenbein, August 5th, 2016 at 8:33 amThis morning, the government reported that the U.S. economy added 255,000 net new jobs last month. Economists were expecting a gain of 180,000. The unemployment rate remains at 4.9%.

This is a solid report. Hourly average earnings rose by 0.3%. The private sector added 217,000 jobs. The number for May was revised higher by 13,000 and June was revised up by 5,000.

This report is ammo for Fed members looking to raise rates, but I doubt we’ll see any move before Election Day.

Cognizant Tech Earns 87 Cents per Share

Eddy Elfenbein, August 5th, 2016 at 8:21 amCognizant Technology Solutions (CTSH) just reported Q2 earnings of 87 cents per share. That’s five cents more than expectations. Revenues rose 9.2% to $3.37 billion which matched consensus.

“Our second quarter performance, as anticipated, represented broad-based revenue growth across service lines, geographies and industries, including healthcare and financial services,” said Francisco D’Souza, Chief Executive Officer. “While our revised guidance reflects the impact of near-term macroeconomic headwinds, our longer term outlook and underlying business fundamentals remain strong. We continue to see an expanding market opportunity ahead and are well positioned to capitalize on the digital transformations taking place among enterprises around the world.”

“The shift to digital continues to intensify and accelerate,” said Gordon Coburn, President. “Our strong second quarter revenue growth, adding incremental quarterly revenue of nearly $170 million, is the result of clients turning to Cognizant to help them define strategy and infuse new technologies to address key challenges and implement new business models. Our robust strategy and implementation capabilities have made us a key partner to clients as they fundamentally transform their businesses and navigate the shift to the digital economy.”

CTSH’s guidance was a little on the light side. Cognizant sees Q3 coming in between 82 and 85 cents per share. The Street had been expecting 86 cents per share. But they reiterated their full-year guidance range of $3.32 to $3.44 per share.

For revenue, CTSH sees Q3 between $3.43 billion and $3.47 billion. Wall Street had been expecting $3.54 billion. CTSH lowered their full-year guidance range for revenue from $13.65 billion – $14.0 billion to $13.47 billion – $13.60 billion. Wall Street had been expecting $13.75 billion.

Cognizant also added $1 billion to their stock repurchase plan.

CWS Market Review – August 5, 2016

Eddy Elfenbein, August 5th, 2016 at 7:08 am“The cleverly expressed opposite of any generally accepted

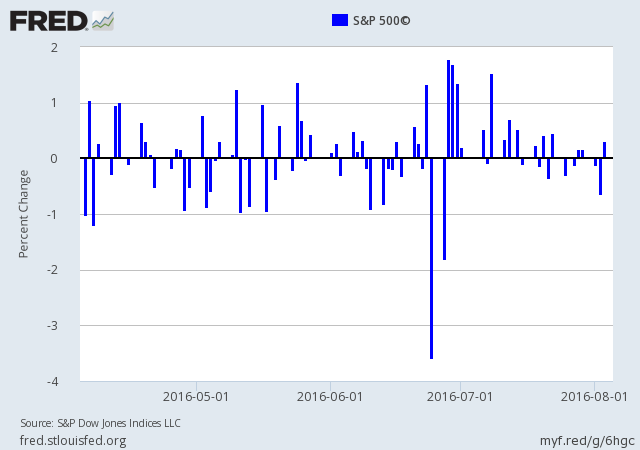

idea is worth a fortune to somebody.” – F. Scott FitzgeraldThe boring stock market is back. Which isn’t such a bad thing, considering all the dramatic news we’ve had this summer. Except for the two days immediately following Brexit, the S&P 500 hasn’t had a 1% daily drop in four months (see the chart below). It took a few days, but Wall Street has reverted to its pre-Brexit slumber.

Personally, I prefer boring markets. Like the tortoise, slow and steady wins the race. In this week’s CWS Market Review, I’ll bring you up to speed on some recent economic reports. The U.S. economy is soggy, but it’s mildly positive. Sure, there’s lots of room for improvement, especially with wages, but we’re not near a recession. Don’t let the fear-mongers get to you.

I’ll also update you on our two Buy List earnings reports from this week. Both Cerner and Fiserv beat the Street by a penny per share. Shares of Cerner jumped 7% on Wednesday. The stock is up more than 32% from its March low. But the big story this week was Biogen. The biotech stock jumped nearly 10% on news that it may be a takeover target. I’ll have full details in a bit, plus I’ll give you my promised analysis of Stericycle. But first, let’s run down some recent economic news.

The U.S. Economy Plods Along

Last Friday, the government said that real GDP grew by 1.2% during Q2. Frankly, that’s pretty weak, and it was less than half of what Wall Street had been expecting. Since the recession ended seven years ago, the economy has grown by just over 2% per year. This is one of the weakest recoveries on record.

One positive note in the GDP report was that consumer spending increased by 4.2% during Q2. The soft spots were sluggish business investment, less government spending and lower inventories.

Despite the sluggish numbers, we’re still a long way from the risk of a recession. In fact, JPMorgan lowered their odds of a recession in the next year to 30%. One of my favorite indicators, the spread between the two- and ten-year Treasuries, stands at 0.87%. The danger zone isn’t until the spread falls below 0.15%.

On Tuesday, the BEA said that personal income rose by 0.2% in June and personal spending rose by 0.4%. Those figures were included in the GDP, and it shows us how healthy consumer spending has been. That may not last. Part of consumers’ strength has been the improving jobs picture. The unemployment rate was 4.9% in June. However, wage growth has been weak. We need to see improvement here.

In last week’s policy statement, the Federal Reserve said, “near-term risks to the economic outlook have diminished.” That’s Fedspeak for, “we’re not following Europe off a cliff.” While that’s encouraging, I don’t believe the Fed thinks the economy is ready, just yet, for another rate hike. The futures market doesn’t see another rate hike coming for another ten months.

Now about earnings. The second-quarter earnings season is quickly coming to a close. Less than one-fourth of the S&P 500 has yet to report. So far, 78% of reports have beaten earnings estimates, while 57% have beaten their sales estimates. Earnings for the S&P 500 are now projected to fall by 3.2% for Q2. That’s not good, but one month ago, the decline was expected to be 5.4%. I think there’s a good chance we’ll see an earnings increase for Q3.

Let me caution you not to be overly concerned with the plodding economy. Much of the weakness in the past year was caused by the strong dollar. As the greenback has stabilized, we can expect some of those effects will fade. Investors should continue to focus on high-quality stocks like you’ll find on our Buy List. From our stocks, Ford Motor (F) and Snap-on (SNA) look particularly attractive at the moment. Now let’s look at our big winner from this week.

Biogen Soars on Takeover Rumors

We got a big surprise on Tuesday afternoon when shares of Biogen (BIIB) rocketed higher after The Wall Street Journal reported that two companies were interested in buying the biotech firm. The news hit the markets at exactly 2:42 p.m. Shares of Biogen immediately jumped from around $300 to nearly $330. In fact, trading in the stock was briefly halted. When trading closed on Tuesday, Biogen had gained 9.37% on the day.

Specifically, the WSJ said that Merck (MRK) and Allergan (AGN) are interested in buying Biogen. The stock has struggled since its peak at $480 in March 2015. That’s one of the reasons why I added it to this year’s Buy List. One analyst at RBC Capital said Biogen could fetch between $375 and $475 per share. I think that’s probably too high, but there’s definitely pressure on big-time healthcare companies to find merger partners. Allergan wanted to hook up with Pfizer earlier this year, but the government blocked a possible inversion.

Whether there is a deal or not, the interest in Biogen shows the hunger big pharmaceutical companies have for new sources of growth.

After years in which their pipelines were depleted, new-drug approvals are up. But the companies have become so large that adding a new blockbuster drug in many cases isn’t enough to increase growth substantially—especially given the pricing pressures that they face. Merck had a market value of $162 billion; Allergan’s was $101 billion.

Biogen had sales of $10.8 billion last year, up 11%. The company, based in Cambridge, Mass., dominates the lucrative market for multiple-sclerosis drugs, now worth nearly $20 billion a year. Its Tecfidera treatment for the condition had one of the best new-drug launches after its 2013 approval, and Biogen stock has roughly doubled since the beginning of that year, even after a sharp recent drop.

Two weeks ago, Biogen became the star of our earnings season. The biotech company reported Q2 earnings of $5.21 per share, which beat estimates by 54 cents per share. Traders loved that news, and the stock jumped 7.6% that day. Biogen also announced a $5 billion share buyback. The company said it sees EPS ranging between $19.70 and $20 this year.

On Wednesday and Thursday, Biogen’s stock pulled back as Merck, Allergan and Biogen all said there’s no deal on the table. Of course, that’s what they’re supposed to say. Still, the WSJ was confident enough to run with the story, so somebody somewhere knows something. It’s clear to me that Merck is the more likely suitor.

Here’s my view: Despite any official denials, Biogen is in play. There’s a weird dynamic in the merger game where one company may do a deal, not because they like it, but because they didn’t want a competitor to do it. A lot of companies would like to have Biogen in their tent. Even if a deal doesn’t come soon—and there’s no guarantee one will—this is a good time for Biogen shareholders. Let the bidders play! This week, I’m lifting my Buy Below on Biogen to $330 per share.

Fiserv and Cerner Beat Estimates

We had two more Buy List earnings reports on Tuesday, plus Cognizant Technology Solutions (CTSH) reports later today. Fiserv (FISV), the financial-services firm, reported Q2 earnings of $1.08 per share, which beat estimates by one penny. That’s an increase of 14% over last year’s Q2. So far, Fiserv has earned $2.14 per share for the first two quarters of this year. Revenues came in at $1.36 billion, which was below estimates.

Overall, this was a solid quarter from Fiserv:

“Our second -quarter results were highlighted by strong growth in the Payments segment, leading to double-digit gains in adjusted EPS,” said Jeffery Yabuki, President and Chief Executive Officer of Fiserv. “Strong sales results in the quarter should add to our momentum in the second half of the year.”

Fiserv was confident enough to raise its full-year range. The old range was $4.32 to $4.44 per share. The new range is $4.38 to $4.45 per share. To add context, Fiserv earned $3.87 per share last year, which means this will be Fiserv’s 30th-straight year of double-digit earnings growth. The shares pulled back on Wednesday, but it was nothing too dramatic. Fiserv is a consistent winner. I’m keeping Fiserv’s Buy Below at $110 per share.

Cerner (CERN) reported Q2 earnings of 58 cents per share, which was also a penny better than expectations. The company had previously given us guidance of 56 to 59 cents per share. Quarterly revenues rose 8% to $1.22 billion, which narrowly beat estimates.

“Cerner’s strong second-quarter results reflect good execution and competitiveness in the U.S. and abroad,” said Zane Burke, Cerner President. “We continued to gain share in what remains an active Electronic Health Record replacement market, while also having strong sales of revenue cycle and population health solutions that help our clients navigate the rapidly evolving reimbursement landscape.”

For Q3, Cerner sees earnings ranging between 59 and 61 cents per share. The Street had been expecting 61 cents per share. The company reiterated its full-year guidance of $2.30 to $2.40 per share, but it lowered its full-year revenue guidance to $4.9 billion to $5.0 billion. The previous range was $4.9 billion to $5.1 billion.

This was a solid report from Cerner, and Wall Street was impressed. Shares of CERN jumped 7% on Wednesday. I like this stock a lot. I’m lifting my Buy Below on Cerner to $71 per share.

Update on Stericycle

Last week, I promised you a detailed update on Stericycle (SRCL). The medical-waste stock got pounded for a 14.8% loss last Friday. At one point it was down more than 22% on the day. All told, SRCL fell to a four-year low.

Here’s what happened: The Q2 earnings report was fine. The company earned $1.18 per share, which matched Wall Street’s estimate, but the company also announced an accounting issue. That normally scares the bejeezus out of traders.

Stericycle said they improperly recognized loss reserves for two litigation issues. As a result, the company overstated its profit for last year’s Q1 by $46.5 million. But they also understated their profits by $27.4 million in last year’s Q2, and by $17.2 million in Q3. There was no difference in the company’s overall profit. Still, it’s embarrassing and doesn’t reassure investors.

I don’t believe the accounting issue is the tip of some kind of fraud. But I am concerned that Stericycle’s management has grown overly reliant on smaller mergers and “rollups” in an attempt to mask slowing organic sales. As a result, the earnings quality has gradually deteriorated. That’s a bad sign. I think it’s interesting that their earnings were inline with expectations, but sales were much less than expected.

On the earnings call, Stericycle said that this year’s earnings will range between $4.68 and $4.75 per share. That’s well below what I had been expecting. I have to be straight with you—I’m disturbed by Stericycle’s recent behavior. I suspected that management had been positioning the company for a sale, and they got sloppy (or greedy). Now I’m not sure that will happen. I’m going to lower my Buy Below on Stericycle to $95 per share.

Before I go, I want to give you an update on Ross Stores (ROST). Three months ago, Ross stunned Wall Street by reporting earnings that matched expectations. Clearly, no one had been expecting that. Think I’m joking? The stock dropped 5.5% after the expected earnings report.

At the time, I told investors not to worry, and that Ross was doing well. Sure enough, once the dust settled, Ross began to rally again, and it continues to be a big winner for us. The stock recently broke though $62 per share and touched an all-time high.

On August 18, the deep discounter will report fiscal Q2 earnings. This week, I’m raising my Buy Below on Ross to $63 per share.

That’s all for now. The July jobs report is due out later today. The June report showed an impressive gain of 287,000 jobs. We’ll have more economic reports next week. On Tuesday, the Q2 productivity report comes out. The job-openings report is due out on Wednesday. Then on Friday, the retail-sales report comes out. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Morning News: August 5, 2016

Eddy Elfenbein, August 5th, 2016 at 7:07 amRBS Slumps on Legal Costs From Past, Bleaker Outlook on Future

Bank of England Cuts Key Interest Rate to New Low

Which Rio Will Olympic Visitors See? It Depends on Your Tickets

Business Groups Sue U.S. Government Over Tax-Inversion Rules

Goldman Regulatory Advisers Were Too Friendly With Regulators

Goldman Sachs Warned It May Have to ‘Restructure’ Its Post-Brexit Business In The UK

Amazon Prime Air Is Here, But Not In the Expected Form

Why Walmart Buying Jet.com To Try And Compete With Amazon Would Not Be A Match Made In Heaven

Berkshire Said to Draw Fed Scrutiny Over Wells Fargo Investment

Takata Profit Drops 33% as Air-Bag Maker Plans Restructuring

Sluggish Cereal Sales Send Kellogg’s Second Quarter Revenue For a 6% Slide

LinkedIn’s Quarterly Loss Worsens, Though Revenue Grows

Allianz Says No More Cost Cuts at Pimco as Outflows Seen Ebbing

Cullen Roche: Do Savers Deserve a Risk-Free Return?

Roger Nusbaum: Turn the TV Off

Be sure to follow me on Twitter.

The Dangers of Market Timing

Eddy Elfenbein, August 4th, 2016 at 8:01 pmI noticed this tidbit in Bloomberg:

Fidelity Investments looked at the returns for 401(k) savers who moved out of equities at or near the market bottom in late 2008 or early 2009 and stayed out as of the end of 2015, comparing them with returns for investors who kept a stake in stocks. The resilient investors were about $82,000 better off.

Morning News: August 4, 2016

Eddy Elfenbein, August 4th, 2016 at 7:04 amA Coup, Terrorists and Inflation, Yet Investors Rush to Turkey

Pound Fluctuates Before BOE Announcement as European Stocks Rise

Goldman Settles Fed Leak Allegations for $36.3 Million

Wal-Mart in Talks to Buy Web Retailer Jet.com

Amid Hunt for Next ‘Thrones,’ Time Warner CEO Charts TV’s Future

Anheuser-Busch InBev to Dominate Combined Brewer’s Leaders

MetLife Profit Falls Short of Estimates on Weaker Underwriting

Siemens Boosted By Growth In Its Energy Operations

Bottled Water to Outsell Soda for First Time This Year

Tesla’s Big Loss Reflects Its Costly Ambitions

Musk Declares Tesla Free From Factory Hell With Targets Intact

The ‘Formula’ That Made Roger Ailes and Fox

Publicis Executive Is Out After Gender Diversity Remarks

Josh Brown: The Paradox of Quant

Jeff Miller: Is 2016 the Year of the Value Trap?

Be sure to follow me on Twitter.

European Bank Distress to Hit U.S. Stocks?

Eddy Elfenbein, August 3rd, 2016 at 8:00 pmWhy Won’t Stocks Budge?

Eddy Elfenbein, August 3rd, 2016 at 7:57 pm-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His