Archive for October, 2018

-

Ingredion Down 9%

Eddy Elfenbein, October 23rd, 2018 at 9:14 amShares of Ingredion (INGR) are currently down about 9% today. The company warned that Q3 earnings will be about $1.70 per share. Wall Street had been expecting $1.96 per share.

Previously, Ingredion had stood by its full-year guidance of $7.50 to $7.80 per share. Now INGR expects $6.80 to $7.05 per share.

From the press release:

During the third quarter, the Company experienced significant FX headwinds caused by weakening foreign currencies primarily in Argentina, Brazil and Pakistan, as well as the impact of Argentine peso devaluation with the adoption of hyperinflation accounting. In North America, the Company experienced several unplanned power outages at Argo, its largest sweetener plant, and these operating events resulted in unforeseen higher manufacturing and supply chain costs.

“Our performance this quarter was impacted in part by the rapid pace and magnitude of FX currency devaluations in Argentina and Pakistan. As a result we expect our business model will require more than a quarter to recover,” said Jim Gray, executive vice president and chief financial officer.

Jim Zallie, president and chief executive officer, said, “We are disappointed with the impact these unexpected circumstances had on our results during the latter half of the quarter, and remain focused on aggressively driving operational improvements and structurally reducing supply chain costs. We are making steady progress in addressing production and supply chain challenges while delivering on our customer experience commitments.”

Ingredion also announced that its Board of Directors has authorized the repurchase of up to an additional 8 million shares of the Company`s common stock from November 5, 2018 through December 31, 2023. Zallie said, “The Board`s increased share repurchase authorization reflects its confidence in the Company`s ability to generate strong cash flow from operations, support strategic investments, and fulfill its commitment to return capital to shareholders.”

-

Morning News: October 23, 2018

Eddy Elfenbein, October 23rd, 2018 at 7:07 amOlympic Steel Is Overlooked And Undervalued

Saudi Sees Deals Worth $50 Billion at Investment Conference Despite Boycotts

Paul Volcker, at 91, Sees `a Hell of a Mess in Every Direction’

Stocks Deepen Losses as Investors Flock to Havens

Unemployment Looks Like 2000 Again. Wage Growth Doesn’t.

Trump’s Tax Push to Help Middle Class Could Help Top Earners Too

What Happens When Banks Smear Their Exiting Brokers

Apple Supplier AMS Plummets Most in a Decade

Judge Denies Monsanto’s Request to Scrap $250 Million Punishment — But There’s a Catch

Why Goldman Sachs’s Marriage Of Marcus And Investment Management Makes Sense

Johnson & Johnson Makes $2.1 Billion Offer to Buy Out Japan Cosmetics Firm Ci:z

The Trade War’s Latest Casualties: China’s Coddled Cats and Dogs

Lawrence Hamtil: Global Discounts By Region & Sector

Michael Batnick: Higher Highs and Lower Lows

Momentum Monday – Lower Prices Ahead

Be sure to follow me on Twitter.

-

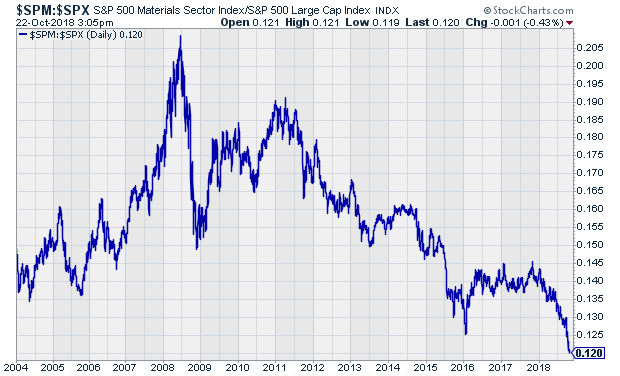

Crumbling Materials

Eddy Elfenbein, October 22nd, 2018 at 3:39 pmThe Materials sector has lagged the S&P 500 for more than ten years. Lately, however, it’s really gotten hammered.

In the last year, the S&P 500 is up just over 7% while the Materials are down 10%.

-

Stocks Above their 50-DMA

Eddy Elfenbein, October 22nd, 2018 at 10:15 amHere’s a chart that shows just how badly the market’s internals have deteriorated. This show the percentage of stocks in the S&P 500 that are trading below their 50-day moving averages.

On September 21, 73.2% of stocks in the index were trading above their 50-DMA. By October 11, that was down to 11%.

-

Hormel Looks to Meat Alternative

Eddy Elfenbein, October 22nd, 2018 at 9:18 amIn yet another sign that the mass craving for meat alternatives isn’t a passing fad, natural and organic meat company Applegate Farms, a subsidiary of processed meat giant Hormel Foods Corp., is thinking about moving into the plant-based space as well.

“We’re a brand that is always looking for better solutions and how do we continue to make progress,” Applegate President John Ghingo said in an interview with Bloomberg. “We are definitely considering creating new products.”

Consumer concerns about meat and dairy—including those related to health, animal welfare and the environment—are driving a $3.7 billion plant-based market, according to recent Nielsen data. Applegate would join such Silicon Valley favorites as Beyond Meat, which has products widely available at grocery stores and some restaurants, and Impossible Foods, which recently unveiled a promotion tied to the ubiquitous White Castle slider.

Ghingo was clear, however, about the company’s continued commitment to its core product line. “We love selling meat; we love our portfolio,” he said. Applegate, acquired by Hormel in 2015, recently introduced a no-sugar bacon, available in both its organic and natural lines, as well as a line of cheeses.

“But,” Ghingo added, plant-based meat alternatives are a “really interesting space.” Applegate pins its image to a promise that all of its animals are raised without antibiotics or growth promoters. Translating that into the vegan sphere is an interesting question, Ghingo said.

“How do we, as a progressive meat and food company, think about moving forward?” he asked.

-

Morning News: October 22, 2018

Eddy Elfenbein, October 22nd, 2018 at 7:05 amWhat It Takes to Understand China Right Now

New Trade Pact Leaves Most U.S. Industry at Mercy of Mexico’s Courts

Quants Now Trade Exotic Stuff. But Can They Handle Illiquidity?

Unemployment Looks Like 2000 Again. But Wage Growth Doesn’t.

Trump’s Pre-Election Tax-Cut Promise Leaves GOP Leaders Baffled

Foreigners Are Dumping Saudi Stocks Like Never Before

How Blackstone Landed $20 Billion From Saudis for New Fund

The World’s Fourth-Biggest Oil Producer Can’t Keep the Lights On

KKR-Backed Calsonic to Buy Fiat Chrysler’s Magneti Marelli Unit for $7.1 Billion

Richard Parsons Steps Down as Interim CEO of CBS

The Next Tech Talent Shortage: Quantum Computing Researchers

Inheriting an IRA? Here’s What You Need to Know

Jeff Miller: Major Market Misperceptions

Joshua Brown: How the Hidden Inflation Sausage Gets Made

Ben Carlson: A Lost Decade of Dollar Cost Averaging

Be sure to follow me on Twitter.

-

CWS Market Review – October 19, 2018

Eddy Elfenbein, October 19th, 2018 at 7:08 am“I’m always fully invested. It’s a great feeling to be caught with your pants up.”

– Peter LynchThe stock market has calmed down somewhat from its temper tantrum earlier this month. What’s striking about the recent unpleasantness wasn’t its degree; a drop of 5.2% in two days really isn’t that much in historical terms. Rather, it’s the jarring jump from a very placid market to a semi-violent one.

Goldman Sachs points out that we just experienced the fifth-largest rise in volatility on record. In our case, rising from very low to moderate. The other four times usually centered on major events like President Eisenhower’s heart attack in 1955. Consider that all five of the calmest quarters in the last 20 years have occurred since the start of 2017.

I have to warn you that the storm hasn’t passed. We’re due for some more turbulence soon. In five of the last six trading session, the S&P 500 has traded below its 200-day moving average. On Thursday, the index closed above its 200-DMA, but only by a teeny tiny fraction, just 0.03%.

The good news for us is that Q3 earnings season has arrived. This gives our Buy List stocks a chance to show their mettle. In this week’s CWS Market Review, I’ll cover our four earnings reports from this week. I’ll also preview seven more reports coming next week. This is a busy time for us, so let’s jump right into our Q3 earnings calendar.

Four Buy List Earnings Reports

Here’s a look at our calendar for this earnings season. Twenty of our 25 stocks are due to report over the next three weeks. I’ve listed each stock’s name, ticker, earnings date, Wall Street estimate and result.

Company Ticker Date Estimate Result Alliance Data Systems ADS 18-Oct $6.20 $6.26 Danaher DHR 18-Oct $1.08 $1.10 Signature Bank SBNY 18-Oct $2.83 $2.84 Snap-On SNA 18-Oct $2.86 $2.88 AFLAC AFL 24-Oct $0.99 Check Point Software CHKP 24-Oct $1.36 Torchmark TMK 24-Oct $1.53 Cerner CERN 25-Oct $0.63 Sherwin-Williams SHW 25-Oct $5.76 Stryker SYK 25-Oct $1.68 Moody’s MCO 26-Oct $1.78 Cognizant Technology Solutions CTSH 30-Oct $1.13 Wabtec WAB 30-Oct $0.95 Fiserv FISV 31-Oct $0.77 Intercontinental Exchange ICE 31-Oct $0.80 Church & Dwight CHD 1-Nov $0.54 Ingredion INGR 1-Nov $1.97 Becton, Dickinson BDX 6-Nov $2.93 Continental Building Products CBPX 8-Nov $0.49 Carriage Services CSV TBA $0.22 Our first four earnings reports all came on Thursday morning before the opening bell. Let’s start with Danaher (DHR). The diversified manufacturer reported Q3 earnings of $1.10 per share. That’s a 10% increase over last year. Core revenues rose 6.5%. The company had told us to expect Q3 earnings to range between $1.05 and $1.08 per share.

For Q4, Danaher expects earnings between $1.25 and $1.28 per share. The company also increased its full-year guidance. The old range was $4.43 to $4.50 per share. The new range is $4.49 to $4.52 per share.

I was particularly pleased to see Danaher’s operating margins expand to 17.1% from 16.8% a year ago. Traders took down shares of DHR for a loss of 3.5% during the day on Thursday. I’m keeping our Buy Below at $110 per share.

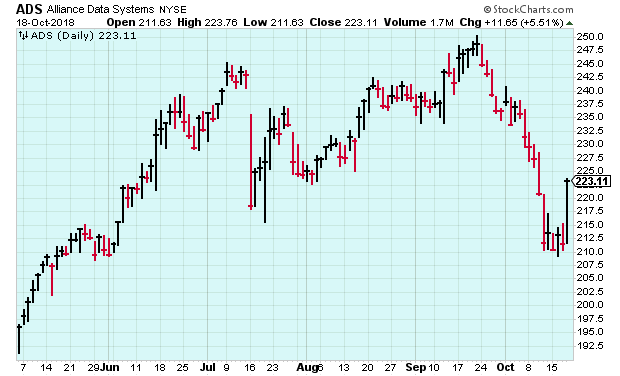

Next up is Alliance Data Systems (ADS). The loyalty-rewards stock reported Q3 core earnings of $6.26 per share. That’s six cents above expectations. So far this year, core earnings are up 20% to $15.70 per share. That puts ADS on track to hit its full-year target of $22.50 to $23.00 per share.

The most interesting part of the earnings report isn’t the financial numbers; instead, it’s what the CEO Edward Heffernan had to say about the company’s future:

“Shifting to our strategic direction, we have spent the better part of this year reviewing the portfolio of businesses that constitute Alliance Data. We are nearing the end of this process and feel it’s appropriate to share our current thinking.”

Heffernan continued: “Stated simply, we firmly believe that our current stock price does not reflect the intrinsic value of our portfolio of businesses across the enterprise. We are evaluating which assets would likely thrive under a different steward, while also unlocking value for our stockholders. We know that the right answer could involve significant realignment of our businesses and we are actively evaluating that optimal strategy. We expect to crystallize a game plan of precisely − what and how − before year end, and will continue to communicate our path forward when appropriate.”

The company is looking to sell off its non-card business. ADS thinks that side of the business is depressing the share price, and they’re probably right. The stock is going for less than 10 times earnings. ADS hopes to make a big announcement soon. On the earnings call, Heffernan was very clear:

Regarding our upcoming announcement for non-cards, make no mistake, we will be moving very aggressively on this and that it will be significant in size. This is not going to be minor surgery. Our Board and management are in full agreement as to the needed actions, and frankly, we like what we’re seeing from a market demand perspective.

Look for more news from ADS soon. The market likes this move, and so do I. The shares gained 5.5% in Thursday’s trading. ADS remains a solid buy up to $245 per share.

Snap-On (SNA) was our big winner last earnings season, but it may be our big loser this time. For Q3, SNA’s sales fell from $903.8 million to $898.1 million. That was well below Wall Street’s estimates of $931 million. The reason isn’t hard to find: tariffs.

Snap-on says that costs have risen sharply. For example, steel costs are up 30%. For the most part, Snap-on has absorbed these price hikes. Despite its poor sales numbers, Snap-on’s earnings were above expectations. For Q3, Snap-on earned $2.88 per share which was two cents better than estimates.

Traders, however, were not pleased. Snap-on plunged for a 9.5% loss on Thursday. I’m lowering my Buy Below price on Snap-on to $167 per share.

Finally, Signature Bank (SBNY) reported Q3 earnings of $2.84 per share. That’s up from $2.29 per share from last year. It also beat Wall Street’s estimate by one penny per share. Let’s look at some numbers. Total deposits are up 7.2% so far this year to $36.09 billion. Loans are up 12.6% to $35.13 billion. For Q3, net interest margin was 2.88%.

Overall, this was a solid quarter for Signature. The shares gained 3.2% in Thursday’s trading. For now, I’m keeping my Buy Below at $131 per share.

Seven Buy List Earnings Reports Next Week

Next week will be another busy one for Buy List earnings reports. It kicks off with three reports on Wednesday.

During the summer, I had been concerned about AFLAC’s (AFL) poor stock performance. Fortunately, the duck stock’s Q2 report put my fears at ease.

For Q2, the company made $1.07 per share, which topped its range of 91 cents to $1.05 per share. AFLAC also increased its full-year guidance range to $3.90 to $4.08 per share. That assumes ¥112.16 to the dollar. The previous range was $3.72 to $3.88 per share. For Q3, AFLAC expects earnings of 87 cents to $1.02 per share. That assumes an exchange rate of ¥110 to ¥115 to the dollar.

Check Point Software (CHKP) did very well for us last earnings season. The cyber-security folks had been expecting $1.15 to $1.35 per share. They made $1.37. Check Point also doubled their share buyback from $1 billion to $2 billion.

For Q3, CHKP expects revenues between $454 million and $474 million and EPS in the range of $1.30 to $1.40. The full-year outlook is unchanged at $5.45 to $5.75 per share. In April, they lowered their full-year guidance, so it’s good to see that the concerns from earlier this year have passed.

Also next Wednesday. Torchmark (TMK) is slated to report its Q3 results. Don’t let these quiet stocks fool you. Torchmark is a very good company.

For Q2, TMK made $1.51 per share. That beat estimates by two cents per share. The company also raised guidance. Torchmark’s initial guidance for this year was $5.93 to $6.07 per share. At the time, I said I thought that was too low and that they could probably hit $6.10 per share in 2018. In July, they upped their full-year range to $6.02 to $6.12 per share. If that’s right, it means Torchmark is going for 14 times earnings. For Q3, Wall Street expects $1.53 per share.

We have three more earnings reports next Thursday. Let’s start with Cerner (CERN). Three months ago, Cerner reported earnings of 62 cents per share, which was a two-cent beat. Revenue for Q2 was up 6% to $1.368 billion. For Q3, Cerner expects revenue between $1.335 billion and $1.385 billion and earnings between 62 and 64 cents per share. Cerner’s current full-year EPS range is $2.45 to $2.55.

Starting in May, Sherwin-Williams (SHW) staged a nice rally for us, but it’s been down sharply over the past month. In fact, almost any stock related to construction or homebuilding has been feeling the heat.

In this summer’s Q2 report, Sherwin not only beat earnings but also raised full-year guidance. The current range is $19.05 to $19.35 per share. Fortunately, the Valspar merger seems to be going well. For Q3, Wall Street expects earnings of $5.76 per share.

Stryker (SYK) was uncharacteristically weak three months ago. The company beat earnings, but the stock dropped more than 10%. On the plus side, Stryker has raised its full-year guidance twice this year. For all of 2018, Stryker now expects earnings to range between $7.22 and $7.27 per share. For Q3, they’re looking for earnings between $1.65 and $1.70 per share.

Moody’s (MCO) is due to report next Friday. The credit-ratings agency had a very good report three months ago. Moody’s earned $2.04 per share which beat consensus by 15 cents per share. Overall, Q2 was a solid quarter for Moody’s. Quarterly revenue rose 17%, and I was impressed by the growth of the Moody’s Analytics business, plus Bureau van Dijk.

Still, shares of Moody have been weak since this summer. The stock is currently 13% below its September high. Frankly, I’m not worried about Moody’s. Most importantly, Moody’s recently reaffirmed their full-year EPS guidance of $7.65 to $7.85. For Q3, the consensus on Wall Street is for $1.78 per share.

That’s all for now. Next week will be dominated by earnings reports. In addition to earnings results, many companies will offer preliminary guidance for next year. The major economic report next week will be Friday’s GDP report. This will be our first look at growth for Q3. The report for Q2 was quite good, but we’ve had a hard time stringing together two or three decent reports in a row. Let’s hope we break this trend. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Syndication Partners

I’ve teamed up with Investors Alley to feature some of their content. I think they have really good stuff. Check it out!

Buy These 3 Stocks to Profit From Marijuana Legalization

High Yield Plus Safety from These 3 Commercial Mortgage REITs

Morning News: October 19, 2018

Eddy Elfenbein, October 19th, 2018 at 7:07 amOil Prices Could Fall Further on Rising U.S. Supplies, OPEC Report Says

Suddenly Toxic, Saudi Prince Is Shunned by Investors He Courted

China’s Economy Slows Amid Darker Outlook at Home and Abroad

Top Chinese Officials Have Staged an Extraordinary Intervention to Stem the Stock Market Bleeding

Musk’s Tweets Aside, The $35,000 Tesla Model 3 Remains As Elusive As Ever

PayPal Quarterly Profit Beats Estimates, Shares Rise

Coca-Cola Shuffles Executives; CEO Names a No. 2

Sears’s Edward Lampert Was a Wizard. Now He’s Coming to Terms with Failure.

Novartis to Buy Cancer-Drug Maker Endocyte for $2.1 Billion

U.S. Recession Chances in Next Two Years Top 60%, JPMorgan Says

Bill Gates: How Paul Allen Changed My Life

StarKist Pleads Guilty To Price Fixing In Alleged Collusion In Canned Tuna Industry

Ben Carlson: How To Stay in the Game

Cullen Roche: Funding in an Endogenous Money System (Nerdy)

Jeff Carter: Return On Investment

Be sure to follow me on Twitter.

Four Earnings Reports

Eddy Elfenbein, October 18th, 2018 at 8:26 amThis morning, Danaher (DHR) reported Q3 earnings of $1.10 per share. That’s a 10% increase over last year. Core revenues rose 6.5%. For Q4, Danaher expected earnings between $1.25 and $1.28 per share. The company again increased its full-year guidance. The old range was $4.43 to $4.50 per share. The new range is $4.49 to $4.52 per share.

Thomas P. Joyce, Jr., President and Chief Executive Officer, stated, “We are very pleased with our performance in the third quarter, as the team maintained strong momentum and delivered outstanding results. We achieved 6.5% core revenue growth, solid operating margin expansion and double-digit adjusted earnings per share growth. Four of our five platforms delivered mid-single digit or better core revenue growth, and we believe our investments in innovation and commercial execution are driving market share gains in many of our businesses.”

Joyce continued, “Our recent performance is a testament to the team’s execution and drive for continuous improvement. We believe the strength and differentiation of our portfolio – combined with the power of the Danaher Business System – provides us with the foundation to deliver sustainable, long-term shareholder value.”

Alliance Data Systems (ADS) reported Q3 core earnings of $6.26 per share. That’s five cents above expectations. Core earnings are up 20% this year to $15.70 per share. That puts ADS on track to hit its full-year target of $22.50 to $23.00 per share.

“There were three significant achievements during the third quarter. First, we are now seeing the benefits from shifting to in-house recovery of charged-off accounts in our Card Services segment as recovery rates moved from a multi-quarter drag toward a growing benefit. Second, also in the Card Services segment, we are trending to a record level of new client signings, which will add as much as $4 billion in card receivables growth over time. And third, our LoyaltyOne® segment had another solid quarter of pro forma revenue growth, coupled with momentum in our AIR MILES® Reward Program as evidenced by a nice step-up in AIR MILES issued.

“Shifting to our strategic direction, we have spent the better part of this year reviewing the portfolio of businesses that constitute Alliance Data. We are nearing the end of this process and feel it’s appropriate to share our current thinking.”

Heffernan continued: “Stated simply, we firmly believe that our current stock price does not reflect the intrinsic value of our portfolio of businesses across the enterprise. We are evaluating which assets would likely thrive under a different steward, while also unlocking value for our stockholders. We know that the right answer could involve significant realignment of our businesses and we are actively evaluating that optimal strategy. We expect to crystallize a game plan of precisely − what and how − before year end, and will continue to communicate our path forward when appropriate.”

Snap-On (SNA) earned $2.88 per share which beat estimates by thee cents per share. Sales fell to $898.1 million from $903.8 million in the year-earlier period. Wall Street had been expecting $931 million according to FactSet.

Chairman and Chief Executive Nick Pinchuk said: “While we experienced sales turbulence in our Repair Systems & Information Group this quarter, we believe the vehicle repair markets in which we operate remain robust and afford ongoing opportunity.”

The company said it expects capital expenditures in 2018 will be in the range of $90 million to $100 million, of which $68.5 million was incurred in the first nine months of the year.

Signature Bank (SBNY) reported Q3 earnings of $2.84 per share. That’s up from $2.29 per share from last year. It also beat Wall Street’s estimate by one penny per share.

Total Deposits increased by $1.10 billion to $36.09 billion. Loans increased by $979.7 million, or 2.9%, to $35.13 billion. Net Interest Margin was 2.88% compared with 2.94% for Q2.

Morning News: October 18, 2018

Eddy Elfenbein, October 18th, 2018 at 7:05 amTreasury Opts Against Labeling China A Currency Manipulator

Trump Opens New Front in His Battle With China: International Shipping

Are Jumpy U.S. Equities Hiding a Nasty Surprise?

Trump Attacks the Weak Link Powell Can’t Ignore in Fed Rate Plan

Invesco to Buy OppenheimerFunds, Adding $246 Billion in Assets

Who’s Ahead in the Battery Race?

Powerful Executives Have Stepped Away From the Saudis. Not Softbank’s.

Netflix’s Cash-Fueled Road to Streaming Dominance

Tesla: A Tough Time To Chase Profits

Trump Administration Releases Prudential From Strict Post-Crisis Oversight

Takeda Gets Japanese Approval for $62 Billion Shire Purchase

Dividend Windfall: Santander Latest Target in Germany’s Giant Fraud Probe

Roger Nusbaum: Are Alternatives Working?

Michael Batnick: Animal Spirits: The Healthy Correction

Howard Lindzon: The Common Knowledge Game and Too Small to Fail

Be sure to follow me on Twitter.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His