Archive for April, 2020

-

Globe Life Earns $1.73 per Share

Eddy Elfenbein, April 22nd, 2020 at 4:21 pmAfter the close, Globe Life (GL) reported that net operating income for the quarter was $1.73 per share compared with $1.64 per share one year ago. That was one penny above expectations.

Some highlights:

• Net income as an ROE was 9.6%. Net operating income as an ROE excluding net unrealized gains on fixed maturities was 14.1%.

• Life underwriting margin at the American Income Life Division increased over the year-ago quarter by 7%. Health underwriting margin at the Family Heritage Division increased over the year-ago quarter by 11%.

• Life premiums increased over the year-ago quarter by 7% at the American Income Life Division. Health premiums increased over the year-ago quarter by 8% at the Family Heritage Division.

• Life net sales at the American Income Life Division increased over the year-ago quarter by 9%.

• Total health net sales increased over the year-ago quarter by 9%.

• 1.6 million shares of Globe Life Inc. common stock were repurchased during the quarter.Globe Life sees full-year EPS ranging between $6.65 and $7.15. The earlier estimate was for $7.03 to $7.23 per share.

-

Silgan Beats Earnings and Raises Guidance

Eddy Elfenbein, April 22nd, 2020 at 8:48 amSilgan Holdings (SLGN) reported Q1 earnings of 57 cents per share this morning. Wall Street had been expecting 49 cents per share. Net sales rose 0.3% to $1.03 billion.

For Q2, Silgan sees earnings between 55 and 70 cents per share. For the whole year, Silgan estimates earnings will range between $2.30 and $2.50 per share. That’s an increase from the previous range of $2.28 to $2.38 per share.

CEO Tony Allott noted that Silgan has been declared “essential” by many government agencies.

“Volumes grew at their strongest rate in March, as the coronavirus began impacting our Western markets. In our metal container business, volumes were up 8 percent in the quarter and, combined with strong operating results, drove record first quarter operating income. In our closures business, volumes grew by 5 percent, with a less favorable mix of products sold as growth in lower margin pumps for soaps and sanitizers were offset by declines in more complex sprayers and pumps for beauty products. Our plastic container business had another record performance with volume growth of 6 percent over the prior year quarter and continued strong operating results.

In February, the company raised its dividend by 9%. Silgan has raised its dividend every year for the last 16 years in a row.

-

Morning News: April 22, 2020

Eddy Elfenbein, April 22nd, 2020 at 7:11 amWith Selective Coronavirus Coverage, China Builds a Culture of Hate

Brent Oil Drops to 21-Year Low, Spreading Pain Across the Globe

Why Oil at Negative $100 Isn’t a Crazy Bet Anymore

‘I’m Just Living a Nightmare’: Oil Industry Braces for Devastation

Global CEOs See U-Shaped Recession Due to Coronavirus

Fannie, Freddie May Soon Buy Home Loans in Forbearance to Help Mortgage Firms

The Death of the Department Store: ‘Very Few Are Likely to Survive’

Everyone You Know Just Signed Up For Netflix

‘A Disaster’: Roche CEO’s Verdict on Some COVID-19 Antibody Tests

Facebook Invests $5.7 Billion in Indian Internet Giant Jio

Nick Maggiulli: Who Feels Rich Really?

Jeff Carter: Oil Crash Isn’t A Sign Markets Don’t Work

Ben Carlson: The Collapse of the Energy Sector

Michael Batnick: The Only Thing Working Right Now

Joshua Brown: Stop Doing Stupid Stuff With Your Money & Why Credit Card Losses Could Explode: What Are Your Thoughts?

Be sure to follow me on Twitter.

-

Stepan Earns $1.04 per Share

Eddy Elfenbein, April 21st, 2020 at 11:17 amThis morning, Stepan (SCL) reported adjusted Q1 earnings of $1.04 per share. That includes the impact of a power outage at their Millsdale plant. Excluding that, Stepan is doing quite well. The consensus of the three analysts who follow Stepan was for earnings of 78 cents per share.

If you’re not familiar with Stepan, the company is a major manufacturer of specialty and intermediate chemicals that are used in a broad range of industries.

Although Stepan is classified with other specialty chemical companies, it’s unique in the industry. Stepan doesn’t have a competitor or competitors to precisely match its businesses because its products have a specific focus.

Stepan makes surfactants, the key ingredients in consumer and industrial cleaning compounds. That includes things like detergents, fabric softeners, shampoos, and lotions. Surfactants make them clean and foam.

Stepan has three operating divisions. For Q1, Surfactants had operating income of $36.2 million. Polymers was at $7.5 million, and Specialty Products did $4.0 million.

The company is also in a strong position financially. Stepan currently has more than $250 million more in cash than in debt. Plus, it has access to a credit line of $350 million.

CEO F. Quinn Stepan, Jr. said:

“Excluding the impact of the Millsdale power outage, the Company had a solid start to the year. Surfactant operating income, excluding the Millsdale incident, was up significantly. Global Surfactant sales volume declined 1% due to strong volumes in the global consumer product end markets driven by increased demand for cleaning and disinfection products, as a result of COVID-19, offset by lower demand within our Functional Product end markets.

Mexican operations delivered strong year-over-year earnings growth. The Polymer business was down primarily due to the Millsdale power outage, impacting mostly our phthalic anhydride business. Rigid Polyol volume was flat as growth within North America and China was fully offset by lower demand in Europe as a result of COVID-19. Global Specialty Polyols results were up with all regions growing operating income year-over-year. Our Specialty Product business results were higher due to improved volume and margins within our MCTs product line due to pantry loading and higher demand in the infant nutrition market, as a result of the COVID-19 outbreak.”

Compared with last year’s Q1, Surfactant sales were down 6%. Polymer was down 11%. Specialty Products was off by 15%. Last quarter, Stepan paid out $6.2 million in dividends and bought back 260,605 shares for $7.2 million. Stepan has increased its dividend every year for 52 years.

The outlook from the CEO:

“2020 is going to be a difficult year for the world, our country, our industry and Stepan Company. However, we believe that in the current environment our business is positioned better than most,” said F. Quinn Stepan, Jr., Chairman, President and Chief Executive Officer. “With empty store shelves around the world for disinfection and cleaning products, our surfactant volume in the Consumer Products end markets should remain relatively strong. Falling raw material prices may provide an opportunity for margin improvement. With dramatically lower oil prices, demand for surfactants within the oil field end-markets will be down. We anticipate our Agriculture business should approximate last year. Overall, we believe our Surfactant business should remain relatively recession resistant.

Our Polymer business most likely will face a reduction in demand as people defer or cancel re-roofing and new construction projects. We also anticipate higher North American costs due to the Illinois River lock closure scheduled during the second half of 2020. The long term prospect of this business remains attractive as energy conservation efforts and more stringent building codes should increase demand.

Our Specialty Product business should continue to benefit from higher MCT demand in the infant nutrition market as pantry loading and retail restocking occur. Our flavor and pharmaceutical product sales should be stable for the year.

We have a strong Balance Sheet with significant cash on hand. We have a $350.0 million revolver which is essentially untapped. Our debt maturity in 2020 is only $23.6 million. Given our balance sheet and available liquidity, we are well positioned to operate in the challenging near-term environment. We have paid a dividend for 62 consecutive years and expect to do so in the future. Despite the difficult current environment, we remain optimistic about the future at Stepan Company and our ability to deliver value for our customers and shareholders.”

The shares are basically unchanged today.

-

Morning News: April 21, 2020

Eddy Elfenbein, April 21st, 2020 at 7:15 amToo Much Oil: How a Barrel Came to Be Worth Less Than Nothing

Oil Meltdown Spreads Beyond Expiring Contracts as WTI Slumps 42%

What the Negative Price of Oil Is Telling Us

London Stock Exchange Committed to Refinitiv Deal in Pandemic-Hit Markets

U.S. Debt to Surge Past Wartime Record, Deficit to Quadruple

Corporate America Seeks Legal Protection for When Coronavirus Lockdowns Lift

The Fed Is Buying $41 Billion of Assets Daily and It’s Not Alone

Trump Says He Will Suspend Immigration

Pandemic’s Costs Stagger the Nursing Home Industry

Huawei First-Quarter Revenue Growth Slows Sharply Amid U.S. Ban, Virus Headwinds

Howard Lindzon: Oil…We Got a Bleeder

Joshua Brown: The Day Oil Went to Zero & 6 in 10 Americans Are More Concerned With “Reopening” Too Soon

Ben Carlson: Different Strategies For Putting Cash to Work During a Bear Market

Michael Batnick: Is Inflation Coming Back?

Be sure to follow me on Twitter.

-

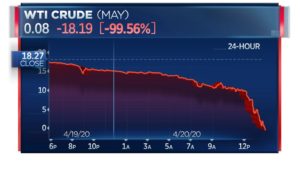

Oil Implodes

Eddy Elfenbein, April 20th, 2020 at 5:38 pmThe big news today wasn’t from the stock market. Instead, it came from the oil pits. The demand for oil plunged. As a result, the price for oil dropped through the floor.

Actually, not just through the floor, but several inches into the ground.

Since supply and demand are out of whack, there’s tons of oil that needs to be stored but there’s no place to put it. As a result, no one wants to own it—and I mean no one! The price for the May futures contract for West Texas Intermediate actually went negative.

That’s not a typo. They literally were paying people to take oil. The lowest price I saw was minus $37.63 per barrel.

I have to point out that we’re talking about the May futures contract. The later months aren’t so dire. The difference is that the over-supply shouldn’t be a big problem later this year. But right now, it’s a big deal. We’ve actually run out of places to store oil and that’s why no one wants to touch it.

-

Wow!

Eddy Elfenbein, April 20th, 2020 at 2:02 pm

-

Oil Plunges to a Multi-Decade Low

Eddy Elfenbein, April 20th, 2020 at 11:40 amThe stock market is down this morning, but the big news is from the oil pits. The price for oil has dropped to a 22-year low. At its low, the price for a barrel of oil was $10.53. As the old joke says, that’s not a bad price for a barrel.

The crash in the price of oil has been remarkable. There are two benchmarks for oil: West Texas Intermediate and Brent Crude. There’s an unusual gap between the two since Brent Crude is now much more. This suggests we have a problem with the storage of oil. American capacity is quickly running out.

Callie Cox points out an interesting stat. Last week, the Russell 3000 Growth Index rose 5.1% while the Russell 3000 Value Index lost 0.1%. That’s the biggest gap in nearly 20 years.

Tomorrow we have an earnings report from Stepan (SCL).

-

Morning News: April 20, 2020

Eddy Elfenbein, April 20th, 2020 at 7:12 amOil Drops Past $15 in New York to 21-Year-Low

The U.S. Tried to Teach China a Lesson About the Media. It Backfired.

The Food Chain’s Weakest Link: Slaughterhouses

A $1.2 Trillion Fund Says Skip Earnings Season, Buy U.S. Stocks

Coronavirus Relief Deal for U.S. Small Businesses May Come Monday, Trump Says

Shake Shack Will Return Its Entire $10 Million U.S. Government Loan

As Amazon Rises, So Does the Opposition

A Speculator’s View On Gilead Sciences And Its Hopes To Treat The Coronavirus Pandemic

Goldman Sees Record U.S. Corporate Spending Cuts This Year

Michael Batnick: Animal Spirits: The Second Wave, Shades of the Dotcom Bubble & It’s A Stock Picker’s Market

Ben Carlson: The Wild World of Yield Chasing & Stocks Just Took the Elevator Down & The Elevator Up

Roger Nusbaum: Is The 4% Rule Dead?

Cullen Roche: Understanding the COVID-19 Aid Package

Jeff Miller: Weighing the Week Ahead: Curb Your Enthusiasm

Joshua Brown: CARES Act vs TARP vs New Deal (Chart)

Be sure to follow me on Twitter.

-

CWS Market Review – April 17, 2020

Eddy Elfenbein, April 17th, 2020 at 7:08 am“The economy is clearly in ruins here.” – Chris Rupkey, chief financial economist at MUFG Union Bank

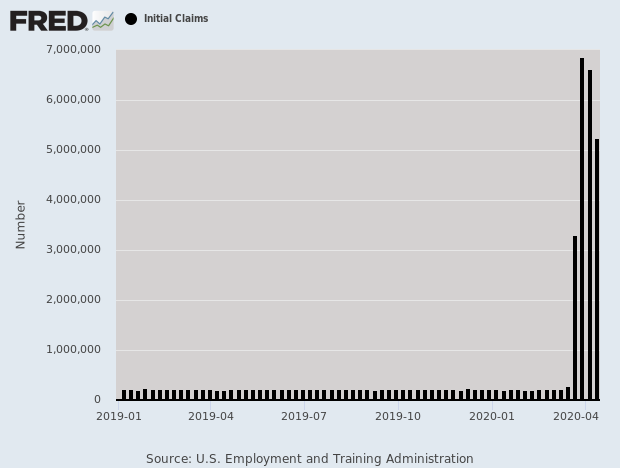

On Thursday, we got another jobless-claims report and it was more bad news. For the week, 5.245 million Americans filed for first-time jobless claims. We’re assuming that number is accurate, but I’m not sure if the system can handle 20 times the normal volume. I’m hearing stories of lots of delays.

Over the past four weeks, 22 million Americans have filed first-time claims. That’s more than all the jobs lost in 2008. We seem to be in a race to flatten the curve before the curve flattens us.

Despite the dire economic news, the stock market has held up fairly well. Will it last? That may depend on Q1 earnings season, which just began. In this week’s issue, we’ll take a closer look at our upcoming Buy List earnings reports. I have a complete earnings calendar for you with all our earnings dates and Wall Street’s consensus.

But first, let’s take a closer look at where the market stands and why we’re rallying in the face of such lousy news.

The Market Rallies on Terrible News

Since March 23, the stock market has had a very impressive run. Based on closing prices, the S&P 500 has gained more than 25% in 17 trading sessions. Of course, that’s following a very nasty spill. Still, it’s one of the biggest bounces in years.

The stock market is, by nature, forward-looking, so it tends to move first. Economic reports, however, are by nature backward-looking. That’s why it’s only now that we’re learning how bad things truly are. The mismatch between the focus of the market and that of the economic reports also explains why the market is rallying amid such ugly news.

Last week was the second-best week for the Dow in 80 years, while the best week came two weeks before. We’re even seeing some big-name stocks like Walmart, Amazon and Netflix make new highs. All of those are helping people cope during the shut-in. On our Buy List, Silgan Holdings (SLGN) just touched a new 52-week high.

I want to reiterate my position that I won’t predict a testing of the recent low, but it’s safe to act like that will happen. We can only go by history which suggests that it’s too early to sound the all-clear. Bear-market rallies are tempting, but they can end badly.

The market continues to be very volatile. I’ll give you an example. The S&P 500 had already had 24 daily moves this year of more than 3%. There was only one 3% day all of last year. Going back a little, there were no 3% days in 2012, 2013 and 2014.

I want to cover some of the recent economic news in more detail because it gives us a picture of just how severe the recession is. The retail-sales report for March showed a decline of 8.7%. That’s more than twice the previous record decline. This report is often a good indicator of consumer spending. The consumer is 70% of the economy.

The industrial-production report for March fell by 5.4%. Capacity utilization fell 4.3% to 72.7%. That’s 7.1% below the long-run average.

Homebuilder confidence was a doozy. It fell from 72 to 30. There’s never been a decline anywhere close to that. Economists had been expecting 55.

Earlier this week, the price for oil dropped below $20 per barrel and hit an 18-year low. OPEC wants to cut production, but that isn’t the issue. The obvious problem is demand.

The New York Fed puts out the Empire State Manufacturing Survey. (I read it so you don’t have to.) I have to confess that it normally makes for pretty dry reading. Not this month. Check out the opening paragraph.

Business activity plunged in New York State, according to firms responding to the April 2020 Empire State Manufacturing Survey. The headline general business conditions index plummeted fifty-seven points to -78.2, its lowest level in the history of the survey—by a wide margin. New orders and shipments declined at a record pace. Delivery times lengthened, and inventories fell. Employment levels and the average workweek both contracted at a record pace. Input price increases slowed considerably, while selling prices declined modestly. Though current conditions were extremely weak, firms expected conditions to be slightly better six months from now.

Trust me. For economists, that’s freaking out.

The main issue is still the virus. We’ve certainly made progress, and the number of new cases appears to have peaked, but there’s still a long way to go. Many states are closed until mid-May, and that’s at the earliest. I can already see grumblings from voters, and that could grow.

The equation isn’t hard. Once things are better, the economy can reopen. I assume it will happen in stages. Once businesses can get back to a full footing, employment and profits will grow.

First-quarter earnings season has begun, and we’re seeing how much damage has happened to corporate profits. At the start of the year, Wall Street had expected the S&P 500 to report Q1 earnings of $40.29 per share. (That’s the index-adjusted figure. Each point is about $8.3 billion.) That’s been revised down to $34.71 per share.

If that’s correct, then it would be a decline of 8.6% from last year’s Q1. Bear in mind that the first half of Q1 was largely unaffected by Covid-19. For Q2, Wall Street expects an earnings decline of 18.4%.

Q1 Earnings Calendar

Our Buy List is close to a five-week high. Thanks to the market’s rally, we now have six stocks that are up for the year, and 15 of the 25 are beating the market this year.

Here’s a look at our Q1 Earnings Calendar. Over the next few weeks, 21 of our 25 Buy List stocks will report their earnings. I’ve listed each stock’s name, ticker symbol, earnings date and Wall Street’s consensus. I don’t have all the reporting dates just yet. (Some companies are quite good at corporate communications. Others are somewhat less so.)

Company Ticker Date Estimate Stepan SCL 21-Apr $0.78 Silgan Holdings SLGN 22-Apr $0.50 Globe Life GL 22-Apr $1.72 Eagle Bancorp EGBN 23-Apr $0.97 Hershey HSY 23-Apr $1.70 Check Point Software CHKP 27-Apr $1.38 Cerner CERN 28-Apr $0.70 Sherwin-Williams SHW 29-Apr $3.94 AFLAC AFL 29-Apr $1.11 Church & Dwight CHD 30-Apr $0.77 Intercontinental Exchange ICE 30-Apr $1.23 Stryker SYK 30-Apr $1.88 Moody’s MCO 30-Apr $2.19 Trex TREX 4-May $0.61 ANSYS ANSS 6-May $0.80 Becton Dickinson BDX 7-May $2.40 Danaher DHR 7-May $1.02 Fiserv FISV 7-May $1.03 Broadridge Financial Solutions BR TBA $1.74 Disney DIS TBA $0.88 Middleby MIDD TBA $1.36 We have five earnings reports due next week.

Stepan (SCL) will be our first Buy List stock to report this earning season. The results are due out on Tuesday morning, April 21. In February, Stepan said it made $1.10 per share for its fourth quarter. Technically, analysts had been expecting 88 cents per share, but that’s a consensus of just two analysts. One expected 86 cents, and the other 90 cents. For the year, SCL made $5.12 per share.

Stepan is one of our new stocks this year. The company is a major manufacturer of specialty and intermediate chemicals. It’s pretty boring but quite profitable. Stepan has increased its dividend for 52 years in a row.

Stepan’s CEO said, “Despite significant challenges during the year, driven by the equipment failure in Ecatepec, the wet weather in the U.S. farm belt, the sulfonation exit in Germany and FX headwinds, the Company exceeded its 2018 record full-year adjusted net income and grew adjusted EPS 7%.”

For Q1, the three analysts expect earnings of 78 cents per share. That’s down from $1.31 per share last year. My Buy Below on Stepan is currently at $110 per share, but I’ll probably lower it next week after I get a chance to see the earnings report.

Silgan Holdings (SLGN) is our second-best performing stock this year. Through Thursday, SLGN is up 7.46%. The stock made a new 52-week high on Thursday.

The company is due to report earnings on Wednesday, April 22. Three months ago, Silgan reported Q4 earnings of 38 cents per share. That pinged Wall Street’s forecast on the nose. Silgan had said they expected earnings between 34 to 39 cents per share, which seems like a wide range.

Frankly, Silgan did not have a great 2019, but I see a lot of promise for them going forward. The company is one of the leading makers of metal containers in the world. In North America, Silgan holds the #1 position in metal food containers. Silgan’s containers are used by folks like Campbell’s Soup, Del Monte and Nestlé.

For 2020, Silgan sees earnings ranging between $2.28 and $2.38 per share. I expect to see that lowered. Silgan recently raised its quarterly dividend by 9% to 12 cents per share. This was their 16th consecutive annual dividend increase. For Q1, Wall Street expects earnings of 50 cents per share.

Globe Life (GL) is also scheduled to report on Wednesday. The insurance stock has been hit hard this year. In February, GL reported Q4 operating income of $1.70 per share. That was two cents below estimates. For 2020, GL expects operating earnings of $7.03 to $7.23 per share. For Q1, Wall Street expects $1.72 per share.

Eagle Bancorp (EGBN) will report earnings on Thursday, April 23. This bank has been our problem child this year. It’s our second-worst performer, trailing only Middleby (MIDD). The bank was hit especially hard by the corona-induced bear. In 16 sessions, EGBN fell 43%.

Still, the actual results haven’t been that bad. For Q4, Eagle earned $1.06 per share. That was one penny below estimates. For all of 2019, Eagle made $4.18 per share. That’s down from $4.44 per year in 2018.

The big issue for Eagle is their legal fees. For Q4, the bank’s legal, accounting and professional fees and expenses rose 68% to $4.1 million. That’s about 12 cents per share.

Looking past these expenses, the bank’s doing just fine. For Q4, Eagle had a return-on-equity of 11.78%. The bank’s efficiency ratio was 39.7% for Q4 and 40% for the entire year. The legal expenses aren’t pleasant, but it’s a manageable problem.

For Q1, Wall Street expects 97 cents per share. At the current price, the dividend yields 3.1%. I’ll probably lower the $48 Buy Below price, but I want to see the earnings first.

Hershey (HSY) will also report on Thursday. HSY is another of our better-performing stocks this year. Hershey is a classic defensive stock, which means it hasn’t been as severely impacted by the bear market. In January, the chocolatier reported Q4 earnings of $1.28 per share. That was four cents better than estimates. The company had been expecting $1.18 to $1.24 per share. For the year, Hershey made $5.78 per share. Last year was a good year for them.

For 2020, Hershey sees earnings between $6.13 and $6.24 per share. For Q1, Wall Street expects earnings of $1.70 per share.

That’s all for now. There are a few key economic reports due out next week. We’ll get the existing-home sales report on Tuesday. The next jobless-claims report is due out on Thursday. This report has become the most-watched economic report on Wall Street. The new-homes sales report will also be out on Thursday. Then on Friday, the durable-goods report is due out. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His