Archive for January, 2021

-

Morning News: January 27, 2021

Eddy Elfenbein, January 27th, 2021 at 7:06 amFed on Hold As Officials Weigh Pandemic Against Vaccines, Fiscal Support

Renewed Demand for Treasurys Quells Fears of Rising Rates—for Now

The Covid-19 Pandemic Has Added $19.5 Trillion to Global Debt

Pfizer-BioNTech to Make 125 Million New Vaccine Doses in First-Ever Licensing Deal

GameStop Extends Meteoric Surge; Melvin Reportedly Closes Short

They Found a Way to Limit Big Tech’s Power: Using the Design of Bitcoin

Wall Street Expects Near-Record iPhone Sales Despite Delay, Shut Apple Stores

How to Pay for College (and Not Lose Your Shirt)

Walgreens Poaches Starbucks Executive Rosalind Brewer for CEO

Cullen Roche: Three Things I Think I Think – Civil WHAT?

Howard Lindzon: Gamestop Monday….WTF Happened?

Michael Batnick: Reflexivity Everywhere

Ben Carlson: For Better or For Worse, This is a Young Person’s Market Right Now

Be sure to follow me on Twitter.

-

Silgan Holdings Earns 60 Cents per Share

Eddy Elfenbein, January 26th, 2021 at 6:11 pmAfter the closing bell, Silgan Holdings (SLGN) reported fiscal Q4 net income of 60 cents per share. That’s an impressive number. Wall Street had been expecting 53 cents per share.

For the full year, Silgan made $3.06 per share. That’s up 42% over last year. It’s also well above Silgan’s earlier estimate of $2.92 to $2.97 per share (which itself was an increase over the prior estimate).

Cash flow from operations rose 19% to $602.5 million. Silgan had free cash flow of $383.5 million. Q4 net sales rose 17.0% to $1.23 billion.

Silgan has a bold forecast for this year.

“While 2020 presented us all with so many challenges, it also provided the Company with the opportunity to showcase the essential nature of our products, the strength and commitment of our team and the power of our performance-based culture, as the Company delivered record adjusted net income per diluted share of $3.06, a 41.7 percent increase over prior year adjusted earnings, and record free cash flow of $383.5 million,” said Tony Allott, Chairman and CEO. “Strong demand for our shelf-stable metal food packaging and our health and hygiene products sustained throughout the year, leading us to expect continued strong volumes in 2021. Therefore, we estimate adjusted net income per diluted share for 2021 for the Company to be in a range of $3.30 to $3.45, a 10.3 percent improvement over the record prior year period at the midpoint of this range. We also expect to continue to generate significant free cash flow of approximately $380 million in 2021, making acquisitions or other value creating uses of our cash an additional near-term opportunity,” concluded Mr. Allott.

So Silgan sees earnings this year between $3.30 and $3.45 per share.

-

Home Prices Surge at Fastest Pace in Six Years

Eddy Elfenbein, January 26th, 2021 at 11:34 amThe GameStop Saga continues. Today, shares of the videogame company are up above $86 per share. That’s still below yesterday’s intra-day high of $159.

The shares are somewhat volatile. Over Friday and Monday, 370 million shares of GME were traded. The float is 47 million.

Things are much calmer in the rest of the market. The S&P 500 broke out to another all-time high this morning. The index has been as high as 3,870.90 but it’s currently just barely negative.

This morning’s Case-Shiller report said that home prices rose by 9.5% in November. That’s one of the highest gains on record.

Prices nationally rose 9.5% in November, compared with November 2019, according to the S&P CoreLogic Case-Shiller Home Price Indices. That is the strongest annual growth rate in over six years, and a significantly stronger gain than in October, when prices were up 8.4%. It also ranks as one of the largest annual gains in the more than 30-year history of the index.

The 10-city composite annual increase in prices was 8.8%, up from 7.6% in October. The 20-city composite showed a 9.1% year-over-year gain, up from 8.0% in the previous month. Detroit was excluded, however, because of continued data reporting issues due to the pandemic.

“Recent data are consistent with the view that COVID has encouraged potential buyers to move from urban apartments to suburban homes,” said Craig Lazzara, managing director and global head of index investment strategy at S&P Dow Jones Indices. “This may represent a true secular shift in housing demand, or may simply represent an acceleration of moves that would have taken place over the next several years anyway. Future data will be required to address that question.”

Our first Buy List earnings report, Silgan Holdings (SLGN), is due out after today’s close. Wall Street expects 53 cents per share.

-

Morning News: January 26, 2021

Eddy Elfenbein, January 26th, 2021 at 7:09 amChina Asset Bubble Warning Threatens Stock Frenzy in Hong Kong

Senate Confirms Yellen as Treasury Secretary as Stimulus Talks Loom

Coronavirus: Seafarers Stuck At Sea ‘A Humanitarian Crisis’

Sizing Up the Wall Street Bets Phenomenon of Retail Trading

Investor Payouts and Job Cuts Jar with U.S. Companies’ Social Pledge

BlackRock Chief Pushes a Big New Climate Goal for the Corporate World

When Surveillance and Censorship Mean Profits for Private Equity

GE Surges as Cash-Flow Forecast Shows Turnaround Gaining Steam

More Carats and Sparkle: How LVMH Plans to Change Tiffany

Budweiser Joins Coke, Pepsi Brands In Sitting Out Super Bowl

Black Hangs On at Apollo as Epstein Scandal Costs Him CEO Role

Howard Lindzon: Momentum Monday…WHY LEAVE YOUR HOME?

Joshua Brown: Here Is Something You Can’t Understand

Ben Carlson: How Technology Ate The Stock Market

Michael Batnick: Timeless Lessons From Today’s Mania

Be sure to follow me on Twitter.

-

The GameStop Saga

Eddy Elfenbein, January 25th, 2021 at 3:48 pmAt Bloomberg, Brandon Kochkodin explains how GameStop become the hottest stock on Wall Street. Here’s a sample:

Before this year, GameStop was a cash register for bearish traders, who borrowed and sold more shares than the company issued. Hedge funds had been winning so long that they overlooked the tinderbox they were creating should sentiment turn.

Now it has, violently. GameStop, which isn’t expected to turn a profit before 2023, has seen its market value triple to $4.5 billion in three weeks, burning the skeptics whose any attempt to cover is likely to further propel its ascent.

A notable victim of the shift has been Citron Research’s Andrew Left, once Wall Street’s most celebrated iconoclast for his role hounding Bill Ackman out of another battleground stock, Valeant Pharmaceuticals, five years ago. Today, Left finds himself first among the hunted, his decision to stop publicly bashing GameStop helping drive it up as much as 78% on Friday.

“Price movement aside, I am most astounded by the thought process that goes in to making these decisions,” Left said in an email to Bloomberg News on Monday. “Any rational person knows this type of trading behavior is short lived.”

-

Shorted Stocks Soar

Eddy Elfenbein, January 25th, 2021 at 11:19 amThere seems to be two stock markets today. On the surface, the normal stock market appears to be, well, normal. The S&P 500 is down about 1% while the small-cap Russell 2000 is up by 0.5%. Not that much of a big deal.

On our Buy List, Trex (TREX) and Miller (MLR) are at new highs today. Trex is already a 20% winner for us this year. Both Miller and Thermo Fisher (TMO) are 10% winners this year.

That’s the normal market. The other market is what’s happening to stocks with strong short positions. Over the last six months, shares of GameStop (GME) have jumped more than 20-fold. Online message boards have led to heavy buying of GME and that’s caused shorts to close their position and buy the stock.

This has created a cycle that’s caused the stock to leave Earth’s orbit. Shares of GME nearly doubled on Friday and they doubled again today.

The same thing has happened to Bed Bath & Beyond (BBBY). At one point, it was up close to 60% today.

AMC Entertainment (AMC), the movie theater stock, more than doubled this morning. The company has managed to avoid bankruptcy (again).

-

Morning News: January 25, 2021

Eddy Elfenbein, January 25th, 2021 at 7:07 amEurope’s Bankruptcies Are Plummeting. That May Be a Problem.

China Wanted to Show Off Its Vaccines. It’s Backfiring.

Pandemic-Era Central Banking Is Creating Bubbles Everywhere

Yellen Passed the Economic Stability Baton to Powell. Now, He’s Handing It Back.

Fed Set to Look Beyond Possible Post-Pandemic Inflation Shock

U.S. Corporate Buybacks Are on the Rise, Lifting Investor Hopes

Goldman Team Sees ‘Unsustainable Excess’ in Parts of U.S. Market

Investor Payouts and Job Cuts Jar with U.S. Companies’ Social Pledge

Kuaishou, TikTok’s Rival in China, Could Be the Biggest IPO Since the Pandemic Began

Taboola, Purveyor of Clickbait Ads, Will Go Public

Merck Shuts Down Covid Vaccine Program After Lackluster Data

These Are the World’s Top-Performing Hedge Funds of 2020

Howard Lindzon: Sunday Sentiment…Tiny Bubbles

Cullen Roche: Rational Reminder Podcast – Understanding the Modern Monetary System

Joshua Brown: Dear Samantha & How America Invests (with Vanguard’s Ryan Barrows), Barry Ritholtz Takes a Victory Lap, “That’s fascinating”

Michael Batnick: Resist the Temptation, Game On & Animal Spirits: Investing in Fixed Income

Ben Carlson: 9 Uncomfortable Facts About the U.S. Stock Market & Getting Your Stock Picks From Podcasts

Be sure to follow me on Twitter.

-

CWS Market Review – January 22, 2021

Eddy Elfenbein, January 22nd, 2021 at 7:08 am“Never buy at the bottom, and always sell too soon.” – Jesse Livermore

This week, we got a new president. Also, the stock market rallied to another new all-time high. Although I strongly doubt the former caused the latter. Instead, we’re in the midst of Q4 earnings season, and so far, the results have been pretty good.

All told, corporate earnings are expected to fall by 15% for 2020. But for this year, Wall Street expects earnings to rebound by 24%. As the Q4 reports come out, we’ll learn more about Corporate America’s outlook for this year.

None of our Buy List stocks has reported yet, but that will soon change. In this week’s issue, I’ll preview six Buy List stocks that are due to report earnings next week. I’m expecting good results. Later on, I’ll highlight HEICO, one of this year’s new additions. But first, let’s look at this season’s Earnings Calendar.

Six Buy List Earnings Reports Next Week

Here’s the Earnings Calendar for this season. Twenty-two of our 25 stocks will report earnings over the next few weeks. I’ve listed each stock’s earnings date and Wall Street’s earnings consensus.

Stock Ticker Date Estimate Result Silgan SLGN 26-Jan $0.53 Abbott Labs ABT 27-Jan $1.35 Stryker SYK 27-Jan $2.55 Danaher DHR 28-Jan $1.87 Sherwin-Williams SHW 28-Jan $4.85 Church & Dwight CHD 29-Jan $0.52 Thermo Fisher TMO 1-Feb $6.50 Broadridge Financial Sol BR 2-Feb $0.70 AFLAC AFL 3-Feb $1.05 Check Point Software CHKP 3-Feb $2.11 Hershey HSY 4-Feb $1.43 Intercontinental Exchange ICE 4-Feb $1.09 Fiserv FISV 9-Feb $1.29 Cerner CERN 10-Feb $0.78 Disney DIS 11-Feb -$0.44 Moody’s MCO 12-Feb $1.94 Zoetis ZTS 16-Feb $0.86 Trex TREX 22-Feb $0.36 Ansys ANSS TBA $2.54 Middleby MIDD TBA $1.40 Miller Industries MLR TBA n/a Stepan SCL TBA $1.08 Silgan Holdings (SLGN) kicks off the show after the close on Tuesday when it reports its Q4 earnings. The container company had a solid Q3. Silgan made $1.04 per share. That was up 37% over last year’s Q3. Wall Street had been expecting 95 cents per share.

The metal-containers business saw volume growth of 17% thanks to more folks eating at home. The closures business was helped by increased demand for household-cleaning products. Their plastic-containers business had volume growth of 14%.

Best of all, Silgan raised its full-year guidance range to $2.92 to $2.97 per share. The previous range was $2.70 to $2.85 per share. Last year, Silgan made $2.16 per share.

For Q4, Silgan now expects earnings of 47 to 52 cents per share. They made 38 cents per share for last year’s Q4.

CEO Tony Allott said, “While we are still completing our annual budget process for 2021, at this time we anticipate overall operating earnings for the Company remaining at these strong levels.”

We have two more reports on Wednesday. Stryker (SYK) can’t offer guidance for Q4, but I’m optimistic. Three months ago, the orthopedics company reported solid numbers for Q3. Stryker earned $2.14 per share. That was up 12% over last year. Wall Street had been expecting earnings of $1.41 per share. That was a huge beat.

For Q3, reported net sales rose by 4.2% to $3.7 billion. Orthopaedics sales rose 4.4% to $1.3 billion. MedSurg sales were up 3.2% to $1.6 billion. Neurotechnology and Spine sales increased 6% to $0.8 billion.

Stryker is currently above our $240 per share Buy Below price. I may raise it next week, but I want to see the earnings results first. Stryker is an excellent company.

The big change to Danaher (DHR) this year was the addition of Cytiva. That’s the new name for GE’s biopharma business, which Danaher bought last year. For Q4, Danaher expects revenue growth, excluding Cytiva, in the low-single digits.

Three months ago, Danaher’s CEO said, “We delivered outstanding third-quarter results, achieving double-digit revenue growth, over 60% adjusted EPS growth, and we more than doubled our free cash flow year-over-year.”

For Q3, Danaher earned $1.72 per share. That beat the Street by 36 cents per share. For Q4, Wall Street expects $1.87 per share. I’m expecting another earnings beat.

Abbott Labs (ABT) is one of our new stocks this year, and it’s due to report earnings on Thursday. In October, Abbott reported 98 cents per share for Q3, which topped the Street by seven cents per share.

I was also impressed to see ABT raise its quarterly dividend by 25%. This marked the company’s 49th annual dividend increase. Many times, stocks with long dividend streaks raise their payouts by a tiny amount just to keep the streak alive. That’s not the case with Abbott.

In fact, Q3 was so good for Abbott that it raised its full-year 2020 guidance to $3.55 per share. Since the company has already made $2.20 per share for the first three quarters, that implies Q4 earnings of $1.35 per share.

There was also more good COVID news.

Abbott Laboratories’ rapid COVID-19 antigen test is highly likely to correctly detect if people have ever contracted the virus and could help with earlier isolation, according to the U.S. Centers for Disease Control and Prevention.

Sherwin-Williams (SHW) is also scheduled for Thursday. Three months ago, Sherwin reported third-quarter earnings of $8.29 per share. That easily beat Wall Street’s forecast of $7.75 per share. Sales rose 5.2% to $5.12 billion.

CEO John G. Morikis said, “Continued and unprecedented strength in our DIY business, solid demand across our residential repaint and new residential segments and improving demand in our industrial coatings businesses and regions drove our strong third-quarter results.”

Let’s look at the breakdown by each business segment. Net sales in The Americas Group increased by 2.8% to $2.98 billion. Consumer Brands Group increased its sales by 23.5% to $838.1 million, and Performance Coatings Group’s net sales increased 1.2% to $1.31 billion. All in all, this was a solid quarter. Sherwin generated $2.56 billion so far this year. That’s up 54% over last year.

For Q4, Wall Street expects earnings of $4.85 per share.

Last is Church & Dwight (CHD). The household-products company reported Q3 earnings of 70 cents per share. That beat estimates by three cents per share. You really can’t go wrong with condoms and baking soda.

C&D’s results were pretty good considering the environment. Q3 net sales grew 13.9% to $1,241.0 million. COVID has actually helped some of C&D’s business.

The company was able to increase its full-year guidance. Before, they saw reported sales rising by 9% to 10%; now they see them up 11%. Not a big increase, but it’s good to see. Most importantly, C&D sees full-year earnings of $2.79 to $2.81 per share. That’s a slight increase over the previous guidance.

So far this year, Church & Dwight has earned $2.30 per share, so that implies Q4 earnings of 49 to 51 cents per share. C&D should easily beat that.

Profile of HEICO (HEI)

At the start of the year, I added five new stocks to our Buy List. Each week, I’ve taken some time to highlight one of our new stocks. I’ve already profiled Miller Industries and Thermo Fisher Scientific. This week, it’s time for HEICO (HEI) of Hollywood, FL.

If you’ve been with us for a while, you may recall that HEICO was on our Buy List in 2016 and 2017, before I unwisely decided to sell the stock. (Ugh, what was I thinking?) The stock promptly doubled over the next three years. Once again, I relearned the valuable lesson about buying good stocks and then doing nothing. Yes, even your humble editor is prone to such mistakes.

HEICO is the kind of niche business I love. With investing, the only thing better than a monopoly is a near-monopoly. (The full-on monopolies tend to get too much government attention.)

HEICO makes replacement parts for the airline industry. Sexy, right? Well, not exactly, but let’s consider a few things. If a commercial aircraft needs some obscure new part, the airline can’t run down to the local hardware store. Instead, it needs to special-order it. Moreover, there’s a great deal of cost pressure on the airlines to keep the older planes serviceable.

Also, the aircraft parts often need to meet strict regulatory guidelines. The part maker really has to know what it’s doing. That’s where HEICO comes in. The business is lean and well run.

HEICO is one of our three “off-cycle” stocks. The company’s fiscal year ended in October, so it reported its Q4 earnings last month. (That’s why it’s not listed in the earnings calendar.)

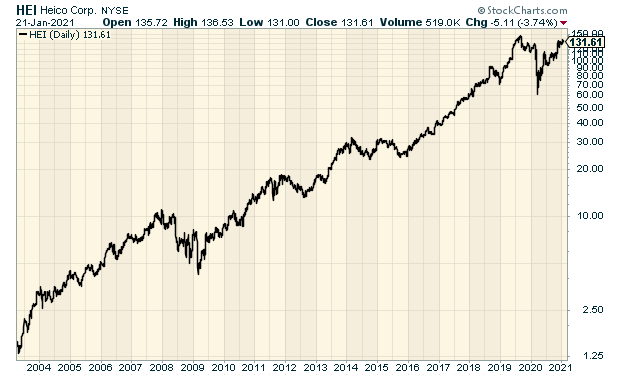

Last year, HEICO did $1.78 billion in business. The company would have probably cracked $2 billion this year if not for the economic lockdowns. HEICO’s long-term track record is very impressive—and the stock is still below its high from mid-2019:

I can’t tell the HEICO story without mentioning the Mendelson family. Larry Mendelson is the current chairman and CEO. In the 1950s, he took a finance class taught by David Dodd. Fans of value investing will recognize Dodd’s name. He was the co-author of Security Analysis with Ben Graham. Security Analysis is probably the foundational text of value investing.

Mendelson took those lessons to heart. He made a good deal of money in real estate and wanted to diversify his holdings. That led him to invest in an under-performing industrial company. He really didn’t care what he bought, as long as it was cheap and had potential to be retooled for future growth. He chose well.

HEICO was originally founded in 1957 by Dr. William Heinicke as Heinicke Electronics. By the 1980s, Mendelson controlled a sizeable share in the company and was able to make himself CEO. The still family owns a large chuck of the voting shares, and several family members hold key positions within the company.

(Important side note: HEICO trades with regular shares and with “A” shares. The A shares afford fewer voting rights for stockholders, which is why they have a lower price. That’s common with business that are controlled by a family. For our purposes, I’m discussing the regular shares.)

When airplane owners need a new part and go back to the original equipment manufacturer (OEM) to get replacements, they’re often charged a steep price. The profit margins can exceed 30%. That provides enormous opportunity for HEICO. Consider that many aircraft are over 20 years old.

The aviation industry is broadly diversified, and HEICO is also able to get sales from commercial and military customers. That means that if there’s a drop-off on one end of the business, the other side can pick up the slack. Wherever there’s a demand to cut costs, HEICO has the potential to do well.

In some respects, I see HEICO’s role as similar to that of a generic drugmaker. HEICO provides a low-cost copy of the original product, which is regulated by the Federal Aviation Administration. By the way, HEICO does more than aircraft parts. They also supply parts for satellites, rockets, missiles and even medical instruments.

HEICO is in an enviable position and nearly dominates its market. The company sells to 19 of the top 20 airlines in the world, and their customers love them. Like nearly everyone else, though, HEICO has felt the squeeze of the economy, and COVID was especially rough on the airline industry.

Still, Larry Mendelson managed HEICO well during a rough patch. For last year, HEICO’s operating margin was 21%, which is quite good, and the company’s cash flow exceeded $409 million. Historically, HEICO has used its cash flow to buy out smaller operators. HEICO currently pays a very small semi-annual dividend of eight cents per share.

Last year’s bear market was brutal on HEICO. In two weeks, the stock plunged 48%. The shares have come back a long way, but I still have some concerns about how quickly the airline industry will rebound. With so few planes flying, not as many will need repairs. I currently rate HEICO a buy up to $140 per share. The company’s fiscal Q1 earnings report will be out sometime in late February.

That’s all for now. The Federal Reserve gets together again next week, on Tuesday and Wednesday. I don’t expect any policy change, but it will be interesting to hear what the central bank has to say in its policy statement. On Thursday, the government will report its first estimate for Q4 GDP growth. I suspect that it will be worse than what Wall Street is expecting. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Morning News: January 22, 2021

Eddy Elfenbein, January 22nd, 2021 at 7:00 amEurozone on Brink of Another Recession Amid Covid Wave

Wall Street Hedges Against Possible Bumps in U.S. Vaccine Rollout

Continuing Job Losses Put Spotlight on Economic Relief

Biden Seeks Immediate Help for Millions as Big Stimulus at Risk

Yellen Vote in U.S. Senate Committee to Test Support for Biden Economic Plan

Fed to Taper Asset Purchases in 2022 or Later, Say Economists

U.S. Is Losing the Battery Race Despite Having the Right Stuff

The N.R.A. Wants to ‘Dump’ Its Regulators via Bankruptcy. Will It Succeed?

China Cracks Down on Fake Divorces That Let People Buy More Properties

Judge Refuses To Reinstate Parler After Amazon Shut It Down

Instacart is Firing Every Employee Who Voted to Unionize

Google Parent Alphabet to Shut Down Loon, Its Internet-Beaming Balloon Project

Joshua Brown: “That’s Fascinating!” with Barry Ritholtz

Howard Lindzon: The Stock Market and Crypto Market Are The Ultimate Platform and Game

Michael Batnick: Can Growth Go Out Of Style?

Ben Carlson: Markets That Are Definitely NOT In A Bubble & Animal Spirits: Micro Bubbles

Be sure to follow me on Twitter.

Trex and Miller Breakout to New High

Eddy Elfenbein, January 21st, 2021 at 11:46 amThe stock market is mostly unchanged this morning although the S&P 500 did make another new all-time intra-day high. The index got as high as 3,861.45.

The earnings parade continues. Bank of America said that its Q4 earnings fell by 22%. On Wall Street, however, it’s all about expectations and B of A topped Wall Street’s forecast. The bank earned 59 cents per share last quarter but that beat Wall Street’s consensus by four cents per share.

On our Buy List, several of our stocks are close to new 52-week highs but only Trex (TREX) and Miller Industries (MLR) have managed to punch through.

This morning’s jobless claims report showed that 900,000 Americans filed for jobless claims. To have the same jobs-to-population ratio that we had before the pandemic, we would need about 10 million more jobs. The current stats roughly divide that in half. They show unemployment rising by 5 million and another 5 million people who have left the jobs market. (If you’re no longer looking for work, you’re not counted as unemployed.)

Earlier this week, Janet Yellen, President Biden’s pick to lead the Treasury, made the case for fiscal stimulus:

Forget about the amount being borrowed, Yellen, a former Federal Reserve chair, told members of the Senate Finance Committee. Focus instead on the interest rate being paid and the returns it will generate, an approach that argues the country’s future economic potential can support more borrowing today and makes the roughly $26.9 trillion in U.S. IOUs seem less formidable.

“The interest burden of the debt as a share of (gross domestic product) is no higher now than it was before the financial crisis in 2008, in spite of the fact that our debt has escalated,” Yellen said. “To avoid doing what we need to do now to address the pandemic and the economic damage that it is causing would likely leave us in a worse place … than taking the steps that are necessary and doing that through deficit finance.”

The Senate will vote on Yellen’s appointment tomorrow.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His