Archive for August, 2021

-

Morning News: August 25, 2021

Eddy Elfenbein, August 25th, 2021 at 7:08 amThe Pandemic Is Testing the Federal Reserve’s New Policy Plan

Inflation vs Jobs Hole: A Tradeoff the Fed Still Hopes to Skirt

SEC Chief Warns ‘Clock Is Ticking’ on Delisting Chinese Stocks

Banks Are Bingeing on Bonds, but Not Because They Want To

Biden’s Cybersecurity Summit Will Gather Very Important People to Solve America’s Hacking Problem

Desperate U.S. Cities Pitch Wall Street-Style Sign-On Bonuses

U.S. Holds Largest Sale of Strategic Oil Reserves in 7 Years

Higher U.S. Food Benefits Give Legs to Dollar Stores’ Fresh Food Push

GameStop, AMC Stock Surge in a Rally for Meme Stocks

‘Made in Afghanistan’ Once Symbolized Hope. Now It’s Fear.

Few Women Ascend Japan’s Corporate Ladder. Is Change Finally Coming?

Corporate America’s $50 Billion Promise

Takata’s Ticking Time Bomb Is Still On The Road

Be sure to follow me on Twitter.

-

CWS Market Review – August 24, 2021

Eddy Elfenbein, August 24th, 2021 at 8:21 pm(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year.)

The S&P 500 closed at another all-time high today. The index is up nearly 20% this year, and we’re not even at Labor Day.

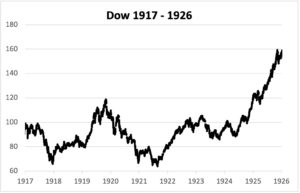

This comes at an interesting anniversary. One hundred years ago today, the Dow Jones Industrial Average closed at 63.90. That was the low point of a nasty bear market that began on November 3, 1919 when the Dow closed at 119.62.

This was a difficult and ugly time for the country. There had been several labor and race riots during the Red Summer of 1919, and in 1921 there was the infamous Tulsa Massacre. The country suffered a long recession that started in early 1920 and didn’t peter out until the summer of 1921.

As is often the case, bad times meant it was a great time to invest. The U.S. was about to embark on the Roaring Twenties. Americans became enthralled by new technologies like radio and movies (and even talking movies!).

The stock market started to boom. Less than one year after the low, the Dow broke 100. By 1925, it hit 150 and by 1927, the Dow topped 200. It nearly doubled again by the summer of 1929. (After that, things got a wee bit problematic.)

Still, the Roaring Twenties was a great time for investors. There were some cracks showing in the façade. Florida, for example, experienced a massive real estate bubble. This was lampooned in the Marx Brothers’ first movie, The Cocoanuts.

Groucho: You can have any kind of a home you want. You can even get stucco. Oh, how you can get stuck-oh!

The Dow had a fantastic run lasting eight years and ten days. The Dow rose nearly sixfold in that time. The index eventually peaked at 381.17 on September 3, 1929. While that was the high, the market didn’t break for another seven weeks. Interestingly, market crashes usually don’t happen at the peak. Instead, they happen on downward slides from the peak.

In this issue, I want to address a topic that I’m often asked about: how I go about selecting stocks to invest in. I like to find companies that have a competitive advantage. Warren Buffett refers to this as a company that has a strong “moat” protecting it. This concept is sometimes misunderstood, and I wanted to take some time to explain what it properly means.

Finding a Competitive Advantage

With investing I like to find companies with a distinct competitive advantage. Here’s a good way to think about this (I’m heavily borrowing from our friends at Investopedia for this example).

Let’s say you have a lemonade stand and business is going well. You suddenly have an idea. Normally, your stand buys lemons each morning. Instead of doing that, you decide to buy a bunch of lemons at the beginning of the week. Your supplier gives you a bulk discount.

Let’s say this cuts your cost of goods sold by 20%. In terms of economics, this is a huge deal. In fact, an innovation like this is what all business is about. This means you can cut your prices by 20%, thereby gaining market share, and it will have zero impact on your gross profit margins. This is great news for you and your business.

As much as we love this, there’s one small problem. While it’s a great idea, it’s just an idea—and one that can be easily copied by your competitors. Once they discover the secret, your advantage is gone.

Now let’s say you come up with a second idea. You invent a revolutionary new lemon squeezer that’s so good, you get 20% more juice out of each lemon. Once again, this is a huge deal in terms of business economics. You’re effectively cutting your costs of goods sold by 20%, and again, you can pass those savings on to your customers with no impact on your gross margins.

But there’s a crucial difference between the first example and the second. In the second case, you can patent your lemon squeezer. That means you can line up state power to enforce your invention monopoly. The idea in the first example isn’t protected the same way. (In reality, you’d probably license your technology and draw a revenue stream.)

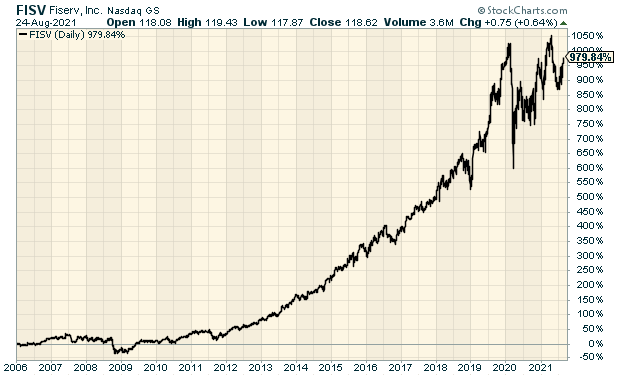

The second example shows the kind of company I look for. I look for firms that do things that no one else can do. Several stocks on our Buy List have strong competitive advantages. In particular, I think of companies like Moody’s (MCO) or Fiserv (FISV).

Check out our tenfold gain in Fiserv.

Keep the Competition Out

Harvard professor Michael Porter has said that a business is first and foremost concerned with differentiating itself and keeping competitors out. Ideally, you want to have a business with high barriers to entry and low barriers to exit, and you want to differentiate yourself with whatever it is you do. You can do that by exclusivity or by price. That’s your competitive advantage. Once you get that, then you get better managers, better advertising and a stronger brand name. But it starts with a competitive advantage.

I think people often have difficulty with the concept of competitive advantage because they want to see sinister forces at work. And make no mistake: I do believe the tempering forces of free enterprise can sometimes break down and give a particular firm a lasting advantage that has nothing to do with its own inherent merit. It could be that they were in the right place at the right time. Or they can use their excess profits to lobby the government to protect their advantage.

For example, many years ago, the Japanese government gave AFLAC (AFL) a monopoly on selling cancer insurance, and this translated into a huge market share today. Naturally, this is unsettling to those of us raised on the idea that the world wants a better mousetrap. But the truth is, it doesn’t. It wants the one it’s heard of. Just like in politics, the incumbent holds a lot of power.

Here’s an example. One of my friends who works with the U.S. Navy explained to me that there are only a handful of shipyards left that are capable of building modern, large-scale ships for the Navy. These shipyards have become, in effect, government sponsored quasi-monopolies. I doubt anyone wanted that to happen, but things turned out that way.

This is an important point that Warren Buffett has often discussed. Nowadays, Buffett is the “aw shucks” face of nice-guy American capitalism, but it wasn’t always this way. In the 1970s, he and Munger bought the Buffalo Evening News.. The Buffalo Courier-Express, a rival newspaper, did everything it could to make them seem like evil out-of-town capitalists. Buffett was beaten up hard in the press, and I think that episode has stayed with him ever since.

In the court case that followed, the opposing lawyer used Buffett’s words against him:

Warren Buffett once said that owning a monopoly newspaper was like owning an unregulated toll bridge. His words were, “…in an inflationary world, a toll bridge would be a great thing to own if it was unregulated.” When he was asked for his rationale, he said, “Because you have laid out the capital cost. You build the bridge in old dollars and you don’t have to keep replacing it.” He was then questioned whether he used the term “unregulated” to mean the ability to raise prices. Buffett said, “That is true.”

It sounds rough, but that’s about the best description of a competitive advantage I can think of. With that said, how do you know if a company has a strong competitive advantage? There are a few characteristics that typically show up.

What Does a Competitive Advantage Look Like?

Oftentimes, the company we’re looking at has a consistent operating history. Sales and earnings edge higher nearly every year. There may be bad years, but the positive trend is clear.

This tells me a few things about the business. First and most obviously, it’s a growing enterprise with a steady demand for its products. It also tells me that management is probably on the ball. That’s because in a dynamic marketplace, you need to make a lot of small corrections to keep the ship moving.

A company with a consistent operating history also probably has a loyal customer base. Never overthink a business. You can make a lot of money selling the same thing to the same people. Ask Starbucks (SBUX

The coffee shop went public in 1992 at $17 per share. Since then, it’s split 2-for-1 six times. That comes to 64-for-1 which means the adjusted IPO price is about 27 cents per share. SBUX closed today $115.08.

Lastly, investing in companies with a consistent track record is an easy way of reducing risk. I’m not a fan of “oil well” stocks. These are companies that appear flat broke but are pinning all their hopes on some deal that may never come. There are too many of these stocks around. When in doubt, I always prefer a stock that grows its business each year.

Tying back to what Buffett said before, a company with a strong moat should also be able to raise prices. This is a subtle rule, so let me explain what I mean.

You’ll notice that I didn’t say I look for companies that do raise their prices. Rather, the key is finding ones that, if the need arises, can raise their prices.

Think about the items in your home or office. Now imagine which ones you would still buy even if they raised their price by 10% or 15%. Some items you’d simply stop buying. But not all.

Why? Maybe you’re attached to a certain item. Or maybe it’s an integral part of your day. I have friends who would make their daily Starbucks run no matter what.

A company that can raise its prices most likely has a firm handle on its costs. There’s a risk component as well. No company wants to raise prices, but it’s nice to be in a position where they can do so if need be.

Ability to raise prices is often a sign that a company has a dominant position in its market. I often think of Harley-Davidson (HOG), the legendary hog stock and former Buy List member.

Is Harley-Davidson a monopoly? Well, in the legal sense, of course not. There are lots of motorcycle companies. Yet Harley is a brand so differentiated that it can be thought of as a pseudo-monopoly. Harley buyers would never view their hogs as just another bike. Harley is quite aware of this (a good portion of their revenue is apparel).

I also like to see a company that is the dominant player in a niche market. A company doesn’t have to own the world to be successful. Owning the best autobody shop in town, or the best Thai restaurant in town, can be a great business.

Why? Because the firm is doing something no else can do. In business, there’s a term called “switching costs.” This refers to the cost for a consumer to change his or her preference. With toothpaste, folks aren’t so picky. With eating habits, people can be very picky. Ross Stores (ROST) is a good example of a company with fairly tight margins (net income margin is around 10%), but high switching costs. Ross’s customers like it exactly where it is.

For a business, you want to be the dominant player, even if it’s in a very narrowly-defined market. Think of the ratings agencies. If you want to float a bond, you pretty much have to deal with Moody’s or S&P.

On our Buy List, we have Broadridge Financial Solutions (BR). This is the dominant player in share-voting proxies. This is the kind of business not one person in 20 ever thinks about, but it fills a concrete need. You can spot a dominant player because it often has modest debt levels, wide operating margins and strong cash flow.

I want to touch on First-Mover Advantage. This was a huge idea in the 1990s, and I think it served as unrecognized fuel for the Tech Bubble. The idea also goes by the name Winner-Take-All.

The idea is that an early entrant could establish an industry standard which remains in place simply because it’s already there. It’s not better—it’s just there. I can’t tell you how many times I was told that some Internet stock was just like the QWERTY keyboard.

In the 1990s, Microsoft was an obvious example of a first mover that became enormously successful, but investors wanted to see where the next standard would be. There was even a magazine called the Industry Standard. Wikipedia tells us that “in 2000, it sold more ad pages than any magazine in America.” Unfortunately, the magazine went belly-up in August 2001.

While being a first mover can certainly give one a competitive advantage, it doesn’t mean it will last. It’s also a bit more complicated than being first. For example, it’s nice to have lots of upgrade cycles.

I hope this issue has helped you better understand what competitive advantage is, and how it can help your investing. If you want to see a list of companies with competitive advantages, you can see my Watch List (subscriber only). Another good resource is the holdings of the VanEck Vectors Morningstar Wide Moat ETF (MOAT). I don’t always agree with them, but at least we’re looking for the same things.

I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you haven’t had a chance, you can subscribe to our premium newsletter. It’s only $20 a month or $200 a year. Please join us!

-

Heico Earns 56 Cents per Share

Eddy Elfenbein, August 24th, 2021 at 4:47 pmHEICO CORPORATION (NYSE:HEI.A)(NYSE:HEI) today reported an increase in net income of 42% to $76.9 million, or $.56 per diluted share, in the third quarter of fiscal 2021, up from $54.3 million, or $.40 per diluted share, in the third quarter of fiscal 2020. Net income was $218.2 million, or $1.58 per diluted share, in the first nine months of fiscal 2021, as compared to $251.7 million, or $1.83 per diluted share, in the first nine months of fiscal 2020.

While net income, operating income and net sales in the third quarter and first nine months of fiscal 2021 were adversely affected by the COVID-19 global pandemic (the “Pandemic”) as discussed below, those impacts are declining over time. Improvement in commercial aerospace market conditions has been evidenced by four consecutive quarters of sequential growth in net sales and operating income at the Flight Support Group.

Net sales increased 22% to $471.7 million in the third quarter of fiscal 2021, up from $386.4 million in the third quarter of fiscal 2020. Operating income increased 47% to $100.8 million in the third quarter of fiscal 2021, up from $68.4 million in the third quarter of fiscal 2020. The Company’s consolidated operating margin increased to 21.4% in the third quarter of fiscal 2021, up from 17.7% in the third quarter of fiscal 2020.

Net sales were $1,356.3 million in the first nine months of fiscal 2021, as compared to $1,360.8 million in the first nine months of fiscal 2020. Operating income was $277.9 million in the first nine months of fiscal 2021, as compared to $287.6 million in the first nine months of fiscal 2020. The Company’s consolidated operating margin was 20.5% in the first nine months of fiscal 2021, as compared to 21.1% in the first nine months of fiscal 2020.

EBITDA increased 36% to $123.9 million in the third quarter of fiscal 2021, up from $91.0 million in the third quarter of fiscal 2020. EBITDA was $347.9 million in the first nine months of fiscal 2021, as compared to $353.7 million in the first nine months of fiscal 2020. See our reconciliation of net income attributable to HEICO to EBITDA at the end of this press release.

Consolidated Results

Laurans A. Mendelson, HEICO’s Chairman and CEO, commented on the Company’s third quarter results stating, “We are very pleased to report much improved quarterly operating results within both Flight Support and Electronic Technologies. Consolidated operating income and net sales in the third quarter of fiscal 2021 improved 47% and 22%, respectively, as compared to the third quarter of fiscal 2020, which was the quarter in which our operating results were most negatively affected by the Pandemic. Our performance principally reflects quarterly consolidated organic net sales growth of 17%, and the favorable impact from our fiscal 2020 and 2021 acquisitions.

Earlier this month, we announced that Flight Support acquired 89% of Ridge Engineering, Inc. and The Bechdon Company, Inc. The purchase price of these acquisitions was paid in cash using cash on hand and we expect these acquisitions to be accretive to our earnings per share within the first twelve months following closing.

Our total debt to shareholders’ equity ratio improved to 17.4% as of July 31, 2021, as compared to 36.8% as of October 31, 2020. Our net debt (total debt less cash and cash equivalents) of $117.1 million as of July 31, 2021 to shareholders’ equity ratio improved to a very low 5.3% as of July 31, 2021, down from 16.6% as of October 31, 2020, which provides the Company with substantial acquisition capital in the balance of our $1.5 billion revolving credit facility and other available capital.

Our net debt to EBITDA ratio improved to .25x as of July 31, 2021, down from .71x as of October 31, 2020. During fiscal 2021, we successfully completed four acquisitions and have no significant debt maturities until fiscal 2024. We plan to utilize our financial strength and flexibility to aggressively pursue high quality acquisitions of various sizes to accelerate growth and maximize shareholder returns.

Cash flow provided by operating activities was very strong, increasing 33% to $124.0 million in the third quarter of fiscal 2021, up from $93.1 million in the third quarter of fiscal 2020. Cash flow provided by operating activities remained strong, increasing 12% to $334.1 million in the first nine months of fiscal 2021, up from $299.0 million in the first nine months of fiscal 2020.

Looking ahead to the remainder of fiscal 2021 and to fiscal 2022, we remain cautiously optimistic that the ongoing worldwide rollout of COVID-19 vaccines will positively influence commercial air travel and will benefit the markets we serve. But, as we’ve all learned, it is difficult to predict the Pandemic’s path and effect, including factors like vaccination rates and new variants, which can impact our key markets. Therefore, we feel it would not be responsible to provide fiscal 2021 net sales and earnings guidance at this time. However, our ongoing conservative policies, strong balance sheet, and high degree of liquidity enable us to invest in new research and development, execute on our successful acquisition program, and position HEICO for market share gains as the industry recovers.”

Flight Support Group

Eric A. Mendelson, HEICO’s Co-President and President of HEICO’s Flight Support Group, commented on the Flight Support Group’s third quarter results stating, “We are very pleased to report quarterly increases of 250% and 33% in operating income and net sales, respectively, as compared to the third quarter of fiscal 2020. These substantial increases principally reflect increased demand for the majority of our commercial aerospace products and services resulting from some recovery in global commercial air travel as compared to the prior year. This marks the fourth consecutive quarter of sequential growth in net sales and operating income at the Flight Support Group.

The Flight Support Group’s net sales increased 33% to $237.1 million in the third quarter of fiscal 2021, up from $178.2 million in the third quarter of fiscal 2020. The net sales increase is principally from organic growth of 32%. The organic growth is mainly attributable to increased demand for our commercial aerospace products across all of our product lines.

The Flight Support Group’s operating income increased 250% to $42.1 million in the third quarter of fiscal 2021, up from $12.0 million in the third quarter of fiscal 2020. The operating income increase principally reflects the previously mentioned net sales growth and an improved gross profit margin principally from the previously mentioned increased demand for our commercial aerospace products. Additionally, we had a decrease in bad debt expense due to certain commercial aviation customers filing for bankruptcy protection in the third quarter of fiscal 2020 as a result of the Pandemic’s financial impact.

The Flight Support Group’s operating margin improved to 17.7% in the third quarter of fiscal 2021, up from 6.7% in the third quarter of fiscal 2020. The operating margin increase principally reflects the previously mentioned increase in net sales, improved gross profit margin, and lower bad debt expense.

The Flight Support Group’s net sales were $666.7 million in the first nine months of fiscal 2021, as compared to $731.2 million in the first nine months of fiscal 2020. The net sales decrease in the first nine months of fiscal 2021 is principally organic and reflects lower demand for the majority of our commercial aerospace products and services resulting from a decline in global commercial air travel attributable to the Pandemic.

The Flight Support Group’s operating income was $103.4 million in the first nine months of fiscal 2021, as compared to $121.6 million in the first nine months of fiscal 2020. The operating income decrease principally reflects the previously mentioned lower net sales, as well as higher performance-based compensation expense and the impact from fixed cost inefficiencies stemming from the Pandemic, partially offset by a decrease in bad debt expense.

The Flight Support Group’s operating margin was 15.5% in the first nine months of fiscal 2021, as compared to 16.6% in the first nine months of fiscal 2020. The operating margin decrease principally reflects an increase in SG&A expenses as a percentage of net sales mainly from the previously mentioned higher performance-based compensation expense and fixed cost inefficiencies, partially offset by the previously mentioned lower bad debt expense.”

Electronic Technologies Group

Victor H. Mendelson, HEICO’s Co-President and President of HEICO’s Electronic Technologies Group, commented on the Electronic Technologies Group’s third quarter results stating, “Despite the Pandemic continuing to moderate demand for certain of our products, we are pleased to report quarterly increases of 14% and 11% in net sales and operating income, respectively, as compared to the third quarter of fiscal 2020. These operating results reflect the impact from our profitable fiscal 2020 and 2021 acquisitions, as well as strong quarterly organic net sales growth for the majority of our products.

The Electronic Technologies Group’s net sales increased 14% to $239.5 million in the third quarter of fiscal 2021, up from $210.9 million in the third quarter of fiscal 2020. The net sales increase principally resulted from our fiscal 2020 and 2021 acquisitions as well as organic growth of 5%. The organic growth principally reflects increased demand for our other electronic, defense, medical, and commercial aerospace products, partially offset by decreased net sales of commercial space products.

The Electronic Technologies Group’s operating income increased 11% to $69.0 million in the third quarter of fiscal 2021, up from $61.9 million in the third quarter of fiscal 2020. The operating income increase principally reflects the previously mentioned net sales growth, partially offset by a slightly lower gross profit margin mainly from a decrease in net sales of commercial space products.

The Electronic Technologies Group’s operating margin was 28.8% in the third quarter of fiscal 2021, as compared to 29.4% in the third quarter of fiscal 2020. The operating margin decrease principally reflects the previously mentioned lower gross profit margin.

The Electronic Technologies Group’s net sales increased 11% to a record $706.2 million in the first nine months of fiscal 2021, up from $638.3 million in the first nine months of fiscal 2020. The net sales increase principally reflects our fiscal 2020 and 2021 acquisitions as well as organic growth of 2%. The organic growth principally reflects increased demand for our other electronic and defense products, partially offset by decreased net sales of our commercial aerospace and space products.

The Electronic Technologies Group’s operating income increased 8% to a record $200.4 million in the first nine months of fiscal 2021, up from $184.9 million in the first nine months of fiscal 2020. The operating income increase principally reflects the previously mentioned net sales growth, partially offset by a lower gross profit margin mainly from a less favorable product mix for defense products and a decrease in net sales of commercial space products, partially offset by an increase in net sales of other electronic products.

The Electronic Technologies Group’s operating margin was 28.4% in the first nine months of fiscal 2021, as compared to 29.0% in the first nine months of fiscal 2020. The operating margin decrease principally reflects the previously mentioned lower gross profit margin.”

-

Another New High

Eddy Elfenbein, August 24th, 2021 at 11:31 amYesterday, the S&P 500 closed just 0.004% below its all-time high close from last Monday. Don’t worry, the market is up again this morning. This could be our ninth up day in the last 11 sessions.

Heico’s (HEI) earnings are due out after the close today. Wall Street is looking for earnings of 55 cents per share.

This morning’s new-home sales report showed an increase of 1% for July. The numbers for June were revised higher as well. The bottom line is that the housing market is still growing but the rate of growth is cooling off. That’s thanks to higher prices and tight inventory.

-

Morning News: August 24, 2021

Eddy Elfenbein, August 24th, 2021 at 7:11 am‘Distressed’ Crude From Venezuela, Iran Stacks Up Off Singapore

Powell’s Charm Offensive in Congress Positions Him to Keep Job

Goldman Sachs Raises Odds on U.S. Fed Taper Announcement in November

U.S. SEC to Scrutinize Firms’ Digital-Engagement Practices As Investor Worries Grow

Hedge Funds Are Hot Again. Good Luck Finding One That’ll Take Your Money

Investors Are Terrified … of Missing Out On the Market Rally

Apple and Google’s Fight in Seoul Tests Biden in Washington

Battery Pioneer Akira Yoshino on Tesla, Apple and the Electric Future

Luxury’s Gray Market Is Emerging From the Shadows

U.S. Retailers Bring Back ‘Above-the-Keyboard’ Clothes as Delta Surge Persists

With Holidays Around the Corner, Walmart Starts Last Mile Delivery Service

Antivaxxers Become Social Outcasts on Wall Street

Purdue Pharma Judge Says Sacklers Face ‘Substantial Risk’ of Liability

Be sure to follow me on Twitter.

-

100th Anniversary of the 1920s Bull Market

Eddy Elfenbein, August 23rd, 2021 at 1:36 pmThe great bull market of the 1920s began 100 years ago tomorrow.

On August 24, 1921, the Dow closed at 63.90. Eight years and 10 days later it closed at 381.17.

And everybody lived happily ever after!!!

In the 1920s there was a real estate bubble, especially in Florida. That’s the backstory of the Marx Brothers first movie, The Cocoanuts.

“You can even get stucco. Oh how you can get stuck-o.”

-

Energy Stocks Lead the Market Higher

Eddy Elfenbein, August 23rd, 2021 at 10:45 amThe stock market is up again this morning. The energy stocks are leading the charge. Many of the big-name oil stocks are up 3% or more while the rest of the market is up just a bit.

In the crypto-world, bitcoin is back above $50,000. Just over a month ago, it slipped below $30,000. Given bitcoin’s volatility, this could all change in a few days.

The Federal Reserve has its big Jackson Hole conference this week. The meeting runs from Thursday to Saturday. Fed watchers everywhere are watching for news. If I had to guess, I think it’s slightly early to hear any tapering news from the Fed. Maybe around Thanksgiving.

This morning’s existing-home sales report rose for the second month in a row. One bright spot is that housing inventory is down 12% over the last year. The median price for an existing home is now $359,900. That’s up 17.8% in the last year.

“The housing sector appears to be settling down,” said Lawrence Yun, chief economist for the Realtors. “The market is less intensely heated as before.”

It may be cooling, but it still appears to be competitive. Homes are spending, on average, just 17 days on the market. First-time buyers represented just 30% of the market, whereas they are usually around 40% historically. Nearly a quarter of all buyers are using all-cash, also a higher share than normal.

The latest read on sales of newly built homes from June showed a sharp decline both monthly and annually, according to the U.S. Census. That data set is based on signed contracts, so it is looking at roughly the same activity as the July data on existing homes. Newly built homes come at a price premium to similar-sized existing homes, and builders say they are now seeing even more buyers unable to afford what they would like.

-

Morning News: August 23, 2021

Eddy Elfenbein, August 23rd, 2021 at 7:01 amXi Doubles Mentions of ‘Common Prosperity,’ Warning China’s Rich

China Halts Over 40 IPOs Amid Regulatory Probe Into Law Firm, Broker

China Muscles In on Middle East Renewables With Alcazar Deal

The Shipping Crisis Is Getting Worse. Here’s What That Means for Holiday Shopping

Delta Variant, Having Put Kibosh on Fed Event, Begins to Menace Recovery

Jerome Powell’s Policy Revolution Was Blindsided by Covid-19

Fed Experts Say Powell Framework Needs Endgame, Inflation Reset

It’s Called The Bond Taper. Yes, It’s Geeky. But This Is Why You Should Know About It

New Appetite for Mortgage Bonds That Sidestep Fannie and Freddie

Biden and the Fed Wanted a Hot Economy. There’s Risk of Getting Burned.

New York’s Economy, Poised for Comeback, Finds Setback Instead

B-Schools Must Evolve for Future Business Demands, Employers Say

Battle for Meggitt Shows Bigger-Is-Better Is Back in Aerospace

Pfizer to Buy Trillium Therapeutics in $2.26 Billion Deal

God, Money, YOLO: How Cathie Wood Found Her Flock

What Say ‘Money Multiplier’ Fabulists As Corporations Stockpile Trillions?

Be sure to follow me on Twitter.

-

Ross Stores Drops in Today’s Trading

Eddy Elfenbein, August 20th, 2021 at 1:31 pmShares of Ross Stores (ROST) got clocked hard this morning. At its low, Ross was down by 6%. It’s made back some lost ground and at the time I write this, Ross is down 2.6%.

Wells Fargo apparently agrees with me that Ross is being too conservative with its guidance:

Wells Fargo says the outlook doesn’t match the better-than-expected results the company announced late Thursday. “We get it, 2H has headwinds-but we view this 2H outlook as a tad overly conservative following such a strong 2Q-not an atypical approach for this management team,” wrote analysts led by Ike Boruchow. Wells Fargo rates Ross Stores stock overweight with a $135 price target.

(…)

Credit Suisse says the company has an “unwavering dedication to its conservative/value-leader narrative” and “struck a conservative tone” during its earnings report.

-

Fiserv’s CEO Talks With Jim Cramer

Eddy Elfenbein, August 20th, 2021 at 1:15 pm

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His