CWS Market Review – April 19, 2022

(If you haven’t done so, please sign up for our premium newsletter. It’s $20 per month or $200 per year. A bunch of our Buy List stocks are about to report results and I don’t want to see anyone left behind.)

Q1 Earnings Season Is Finally Here

We’re now in the thick of earnings season. This time of year can be brutal for stocks that come up short. In fact, it can even be brutal for companies that beat expectations.

Example: Netflix. After today’s close, Netflix said it earned $3.53 per share which easily beat Wall Street’s forecast of $2.91 per share. Still, traders were very displeased.

The problem is that Netflix lost 200,000 subscribers during Q1. That’s the first time Netflix has lost subscribers in more than 10 years.

The company estimates that they’ll lose another 2 million folks during Q2. The stock is down 25% in after-hours trading, and that’s on top of being down 40% YTD. We’re talking about a loss of something like $40 billion after beating expectations.

Ouch!

Of course, earnings season isn’t simply about how well you did. It’s also about your guidance for the coming quarter.

As far as Q1 goes, so far, the earnings numbers are looking pretty good. The S&P 500 is tracking Q1 earnings for growth of 5.13%. That’s down from 5.41% one month ago, but it’s still not too bad. The big winner is the Energy sector which is hardly surprising. The Energy sector is showing Q1 earnings growth of more than 260%. Of course, that’s coming off very weak comparisons.

So far, 77% of companies have topped their expectations. That’s above the historical average. (On Wall Street, you’re expected to beat expectations.) Another 77% of companies have beaten Wall Street’s revenues estimate. Nearly 63% of companies have beaten on both earnings and revenue.

With earnings up and stock prices down this year, that means the market’s P/E Ratio is down for 2022. The S&P 500 is currently on pace to report Q1 earnings of $51.13 per share. That’s the index-adjusted figure. (Each point in the S&P 500 is about $8.5 billion.)

For the year, the S&P 500 is tracking earnings of $225.17 per share. That means the index is going for just under 20 times this year’s earnings. Traditionally, the P/E Ratio goes down as long-term interest rates go up.

The good earnings news isn’t helping the market. On Wednesday, the S&P 500 closed at its lowest level since March 16. Interestingly, that was the same day that the Federal Reserve raised interest rates for the first time in more than three years.

After the Fed’s rate increase, the stock market started to rally. Now, however, the market has given back all those gains. Prior to Tuesday’s 1.6% rally, the S&P 500 had closed lower in seven of nine sessions.

How low will the market go? Well, that’s a tough one to answer. Still, we have to be aware that the market is swimming against the tide. Not only is there rising inflation but interest rates are going up, the yield curve has flattened and there are growing fears of a recession—and, of course, we can’t forget a nasty war in Eastern Europe.

On top of that, bond yields continue to rise. On Tuesday, the 10-year Treasury yield came close to breaking above 3%, a level it hasn’t seen since late 2018. As I noted before, those higher yields tend to weigh on earnings multiples for stocks.

The example of 1994 is a good one. During that year, the Federal Reserve increased interest rates. As a result, the market’s P/E Ratio dropped. However, the earnings figure —the E— was climbing rapidly while stock prices —the P— didn’t do much at all.

The Fed seems determined to raise interest rates all year. The central bank again meets in two weeks and futures traders think there’s a 91% chance the Fed will hike by 0.5%. But here’s what’s interesting. In the meeting after next, the one set for mid-June, futures traders think there’s a 36% chance that the Fed will hike by 0.75%. I doubt the Fed will go that far, but it’s not outlandish to think so.

Just this week, James Bullard, the president of the St. Louis Fed, said that the Fed shouldn’t rule out a 0.75% increase. According to Bullard, rates should be around 3.5% by the end of this year. He’s the most hawkish voice on the Fed and I think the facts have borne him out.

The Low Point in the Dow’s Decade Cycle

This June 27 will be a noteworthy day for the stock market. This day is the traditional low point for the stock market’s decade cycle. I crunched all the data from the entire history of the Dow Jones Industrial Average going back to its founding in 1896.

I found that the Dow historically reaches its low point on June 27 in the years ending with 2. Indeed, those years have marked some important bottoms for the Dow; 1932, 1942, 1982 and 2002 come to mind.

The Dow’s traditional peak comes on September 13 in years ending with 9. That’s not a surprise given 1929, 1969, 1989 and 1999.

Between those two days, September 13 of a year ending in 9 and June 27 of a year ending in 2, the Dow has lost an average of 19.3%. That covers 23% of the time. The rest of the time, the Dow has gained 185.9%.

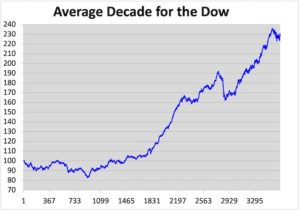

Here’s what the average decade looks like for the Dow. I used 100 as a base for January 1 of a year ending in zero.

The x-axis shows the number of days into the average decade.

There’s also a noticeable split between the first half of a decade and the second half. For the first five years, the Dow has averaged a gain of 11.6%. During the latter half, the Dow has averaged 106.2%.

I find stats like this fascinating for a few reasons. One, I simply find markets intrinsically interesting and any behavior that stands out from over 125 years’ worth of data grabs my attention.

But let me stress that I don’t think there’s any worthwhile trading strategy to be gained from this data. Quite the opposite. I think data like this shows the futility of basing a long-term investing strategy on trying to time the market.

The data shows that as a general rule, the stock market is in rally mode about three-quarters of the time, and it’s in a bearish mood about one-quarter of the time. That certainly seems to pan out according to my experience. There are times when the market rallies despite terrible headlines. Conversely, there are times when the market can’t seem to catch a break. There’s no magic to it; it’s just the nature of financial markets.

What Happened with Masimo

Last year I told you about one of my favorite growth stocks, Masimo Corporation (MASI) of Irvine, CA.

As much as I said I liked the story, I confessed that I wasn’t a fan of Masimo at $270 per share. However, I wrote, “if it gets back to $200 or so, then it could be a very compelling buy.”

Where is Masimo today? Answer: $136 per share.

Dear Lord, what happened? Let’s take a step back and look at this story.

Masimo is a medical-technology company based in Irvine, CA. This is a fascinating company that’s not well-known but it’s a cool story, and the company has a definite competitive advantage.

Masimo was founded by Joe Kiani, an Iranian immigrant. Kiani came to the U.S. when he was only nine years old and he knew three words of English. Still, he graduated from high school at 15 and by 22 he had a bachelor’s and master’s degree in electrical engineering. Kiani founded Masimo in 1989 when he was 25 years old.

Today, Masimo is a $7 billion enterprise. It employs 2,200 people and last year it had sales of $1.2 billion. Masimo is perhaps best known for its pulse oximetry. This is a noninvasive method for monitoring a person’s oxygen saturation. This is a great product with enormous potential.

Masimo has developed a SafetyNet device which is a disposable smart wristband with a pulse oximeter that’s taped around your finger. It monitors your vitals like your pulse and oxygen levels. If there’s a problem, an update is sent to your smart phone, and it alerts your doctor. It can also be connected to a central monitor like a hospital.

Each year, over 200 million patients are monitored with Masimo’s technology. Nine of the top ten hospitals rated by U.S. News primarily use their technology.

Did you know that unpredictable reactions to opioids kill more people than car crashes? It’s impossible to know who’s at risk. But with continuous monitoring, we can spot adverse reactions quickly.

Interestingly, the device was meant to be used for opioid addicts, but plans changed once Covid-17 hit. Now it’s being used on coronavirus patients. Since the technology is wireless, it’s also safer for healthcare workers.

Interesting side note: Masimo has been in a big legal fight with Apple. Masimo claims that Apple poached their trade secrets for their Apple Watch. I should add that Kiani is no stranger to these kinds of legal battles, and he’s already won a few cases with big settlements. The odd thing with this one is Apple’s complete intransigence.

Kiani said that Apple has also picked off some of Masimo’s top talent. I guess rules are a little different when you have a market cap of $2.5 trillion. Still, my money’s on Kiani in any courtroom.

Tying back to my earlier point, Masimo had been a great growth stock. Consider these numbers. Masimo’s earnings-per-share rose from $2.13 in 2016 to $2.45 in 2017 to $3.03 in 2018 and to $3.22 in 2019. Earnings then rose to $3.60 per share in 2020 and to $3.99 per share last year.

What about for this year? Well, that may be a big problem. The next earnings report is due out on May 3. The company recently said that sales for Q1 will be lower than expectations. Kiani, said, “In prior quarters, we were able to weather the storm of COVID-related supply chain issues. However, these issues impacted us in the first quarter.” The good news is that Masimo reiterated its full-year revenue guidance of $1.35 billion.

Previously, MASI said it expected full-year earnings of $4.34 per share for 2022. They haven’t lowered that yet, but downward guidance is widely expected. The consensus on Wall Street is for $4.03 per share, and some analysts are pegging earnings at less than $3 per share. I’m afraid those lower projections are the more accurate ones.

In all of this, Masimo’s stock has been badly damaged. In November, MASI was over $300 per share. Earlier this week, it got to a new 52-week low of $129.68 per share. It’s one thing to pay a big premium for the company that’s growing at a blistering rate, but it’s quite another when earnings may shrink this year.

That’s the problem when growth stocks no longer grow. The stock is doubly punished with lower earnings and a lower multiple. The other problem for Masimo is that it recently shelled out a little over $1 billion to buy Sound United, “a consumer technology company that owns a portfolio of premium brands, including Bowers & Wilkins, Denon, Polk Audio and Marantz.” Wall Street doesn’t like this deal at all. The stock dropped 37% on the news.

In this case, we were wise to pass on Masimo. Now we know that the lower price is still no bargain. Sometimes the best investing moves you make are when you decide to do nothing.

I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you haven’t had a chance, you can subscribe to our premium newsletter. It’s only $20 a month or $200 a year. Please join us!

Posted by Eddy Elfenbein on April 19th, 2022 at 7:42 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- August 2026

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His