CWS Market Review – January 24, 2023

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

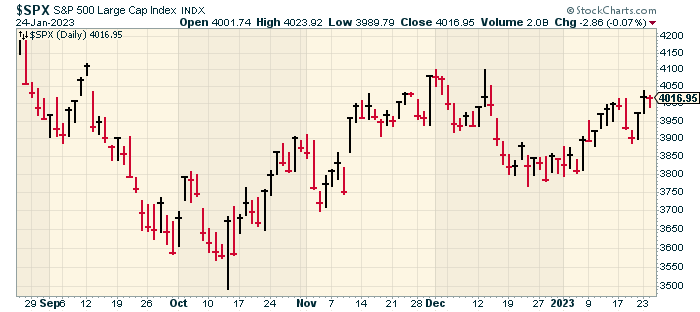

The S&P 500 Closes Above 4,000

Yesterday, the S&P 500 closed above 4,000 for the first time in six weeks. Previously, the index had popped its head above 4,000 a few times, but yesterday was the first time it had closed above 4,000 since December 13.

The stock market looked like it was going to close much lower today, but thanks to some strength in the afternoon, the S&P 500 only lost 0.07% and is still above 4,000.

We’re in earnings season and it’s still early but the numbers are looking favorable. On our Buy List, Danaher and Silgan solidly beat earnings (I’ll have more details later this week in the premium letter.)

So far, just 11% of the companies in the S&P 500 have reported results but 67% have reported an earnings surprise and 64% have reported a sales surprise.

One hitch is that prior to earnings season, Wall Street analysts dramatically cut back on their estimates. This means that while many companies are beating estimates, those are much-lowered forecasts.

According to FactSet, the market’s overall net profit margin is down for the sixth quarter in a row. In other words, sales are growing faster than earnings. That’s not necessarily a problem for the market, but it’s indicative of where we are in the economic cycle. When companies see growing inventories, that often leads to more generous pricing which leads to lower profit margins. This is what usually happens later in an economic cycle.

The Federal Reserve meets again next week, and it seems very likely that the Fed will raise short-term interest rates by another 0.25%. The central bank has all but admitted its plans. This is an admission that the inflation news has been encouraging, but I want to stress that the job isn’t done yet.

The Fed is entering a difficult spot because the economy appears to be weakening and inflation hasn’t completely faded. This is a problem because the Fed wants to appear vigilant against inflation, but at some point, the economy will need to lower interest rates. In fact, futures traders think that the Fed will start cutting interest rates before the end of this year.

The current outlook from the futures market is for two more 0.25% hikes. The first one will be next week. Another 0.25% will follow in March. That will bring the target for the Fed funds rate to 4.75% to 5%. After that, the futures market sees the Fed pausing for several months. Note that this is noticeably more lenient than the rhetoric coming from the Fed. By no means is the futures market accurate, but it shows you how people are betting.

Parts of the economy are starting to show some cracks. The housing sector has been weak for several months. Friday’s report on existing home sales showed the 11th monthly decline in a row. That’s the longest losing streak in the data’s history. For December, existing home sales were down by 1.5%. For the year, existing home sales fell by 34%. That was a worse calendar year drop than in 2007, 2008 or 2009—the key years of the housing bust. Except for the pandemic, this was the lowest sales rate since 2010.

While the overall labor market is still healthy, we’re seeing many layoff announcements, especially in the tech sector. This has even led some people to speak of a “Techcession.” Spotify just said that it’s laying off 6% of its workforce. Microsoft said it’s cutting 10,000 jobs. Amazon is letting 18,000 jobs go. Google said it’s getting rid of 12,000 jobs.

Speaking of Google, the Justice Department said it’s seeking to break up Google’s online ad business, claiming it has a monopoly-like hold over the industry. I should note that the government doesn’t have a great track record in going after high-tech companies.

The most infamous case may be when the government went after IBM in the 1970s. The case was filed in January 1969 in the closing days of the Johnson Administration. It dragged on in the courts for years. By 1982, the government saw little chance of winning. After realizing it had already spent so much, the government threw in the towel and gave up the case.

Even though nothing came of the anti-trust case, it had a big impact on Corporate America. A few years later, when Microsoft came along, any modern investor would have wondered why IBM didn’t simply buy out Bill Gates’s little company. Nowadays, that would be the easy way to take care of the problem, but back then, big companies were too scared of getting any attention from the DOJ.

What gets DOJ’s ire is if a company uses its strength in one market to gain an advantage in another market. There can be Acme Car Company. That’s fine, but Acme can’t say that it only runs on Acme Gasoline. The Justice Department said, “Google would no longer have to compete on the merits; it could simply set the rules of the game to exclude rivals.” For its part, Google says that the government is doubling down on the types of cases it has already lost. This is the fifth case the government has brought against Google since 2020.

Outside of any Techsession, big layoffs are hitting other industries as well. In finance, Goldman Sachs said it’s cutting 3,200 jobs. Both Bank of New York Mellon and BlackRock are cutting 3% of their respective workforces. In the crypto world, Coinbase said it’s cutting 20% of its workforce.

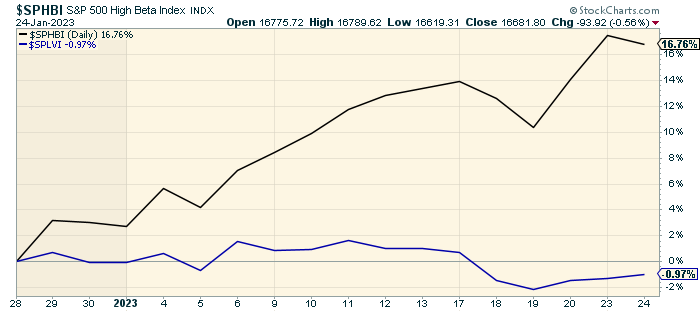

One interesting dynamic in the stock market this year has been the resurgence of riskier stocks. From December 28 through yesterday, the S&P 500 High Beta Index has gained over 17.4% while the S&P 500 Low Volatility Index is down 1.3%. That’s a huge gap for such a short time span.

Coming out of the pandemic, High Beta outperformed Low Vol by a substantial margin. Last year, Low Vol did much better, but so far this year, High Beta is out in front.

Part of this is related to Fed policy. When interest rates were near 0%, taking on a lot of risk was a no-brainer. Now that interest rates are going higher, risk is suddenly a lot more important. I think some traders assume that High Beta will soar out in front if the Fed starts cutting again. That might be a mistake. If the Fed does cut, it won’t be for several months, and I’m not sure if they’ll cut by a lot.

The next big economic report will be the Q4 GDP report which will be out on Thursday morning. This will be the first report on Q4 GDP growth. The report will be revised again in late February and again in late March.

You may recall that the GDP reports for Q1 and Q2 both showed declines. While that’s not technically a recession, it was cause for concern. The numbers for Q3 were much better. The U.S. economy grew in real annualized terms by 3.2% for the third three months of the year.

What should we expect for Q4? The consensus on Wall Street is for real annualized growth of 2.8%. That may be too low. I don’t think we’ll see recession-type numbers in the Q4 report, except for housing. However, I do believe that the economy will get weaker as the year goes on.

I checked which outstanding Treasury security has the highest current yield. The answer is the Treasury due in October of this year, roughly an eight-month bill. The current yield is 4.749%. Out of the trillions in Treasury debt, that’s the highest. It reiterates the idea that the Fed may start cutting rates later this year. The strong rhetoric coming from the Fed simply isn’t credible.

Stock Focus: U.S. Lime and Minerals

This morning, AmerisourceBergen announced that it’s changing its name to Cencora later this year. This is a reminder of how much I hate modern corporate names. Companies tend to spend tons of money coming up with names that sound like nothing. Verizon? Prologis? Yuck! As bad as Cencora is, at least it’s better than AmerisourceBergen.

In 1927, the Dow Jones Industrial Average had 20 stocks. Seven of them began with American, three with United and two with General. How I miss those names.

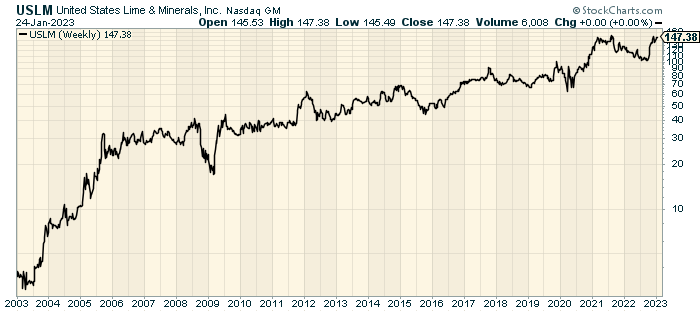

This leads me to this week’s stock in focus which is United States Lime & Minerals (USLM). Now that’s a name!

Twenty years ago, you could have picked up one share of USLM for $2.82. A few days ago, it was going for $154 per share. That works out to an average annualized gain of more than 22%.

Plus, that return doesn’t include any dividends. A dividend increase may be coming soon. One year ago this week, USLM increased its payout by 20%.

You might think that with a track record like that, USLM would have tons of analysts who follow it. Well, that’s not the case. Actually, not a single Wall Street analyst follows USLM. That’s a 54-fold gain in 20 years, and no one saw it. When earnings come out, we can’t say if it beat or not because there is no consensus.

So what does United Lime do? As the name suggests, lime. Lots of it. The company “is a manufacturer of lime and limestone products, supplying primarily the construction (including highway, road and building contractors), industrial (including paper and glass manufacturers), metals (including steel producers), environmental (including municipal sanitation and water treatment facilities and flue gas treatment processes), roof shingle manufacturers, agriculture (including poultry and cattle feed producers), and oil and gas services industries.”

The company has been doing well lately. The Q4 earnings report should be out within the next week or so. For Q3, Lime’s revenues increased 27% to $66.5 million. Net income increased 39% to $2.77 per share. For the first three quarters of 2022, Lime earned $6.10 per share. That’s up from $5.19 per share in 2021.

President and CEO Timothy W. Byrne, said, “We continue to see strong demand from our construction customers and have benefited from long stretches of dry weather in our Texas markets.”

My rough estimate is that USLM will report earnings of $1.60 per share for Q4 which would bring the full-year results to $7.70 per share. That would mean the company is going for about 19 times trailing earnings. That’s not bad.

USLM currently had a market value of $830 million. The company is based in Dallas and it has 308 full-time employees. I recently updated my Watch List and USLM continues to be among my favorites.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want to learn more about the stocks on our Buy List, please sign up for our premium service. It’s $20 per month, or $200 per an entire year.

Posted by Eddy Elfenbein on January 24th, 2023 at 7:38 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- August 2026

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His