CWS Market Review – January 3, 2023

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

Happy 2023!

If you haven’t had a chance to see it, here’s our 2023 Buy List. I’m proud to say that after one day, we’re already beating the market this year. The bad part is that like much of 2022, we’re down, just by less than everybody else.

I’ll be honest with you, I’m not sorry to see 2022 go. It was a difficult year for investors.

Last year was the fourth-worst year for the stock market in the last 80 years. Some of that, I should add, is due to the calendar effect. The market peaked on the first day of trading in 2022, and things got worse from there.

Investors were also fooled by several bear-market rallies. It seems like the market knows exactly when to lure you in and then hit you with another downturn.

The major investing story this past year was the resurgence of inflation combined with the Federal Reserve’s interest rate hikes. In retrospect, it’s alarming how slow the Fed was to realize the scope of the problem.

I don’t expect the Fed to get everything right, but even after the evidence became clear, the Fed was still slow to react. I’ll give you an example. At the December 2021 meeting, the Fed released its economic projections for 2022. The FOMC members expected inflation to be just 2.6% in 2022. They weren’t even close.

The Fed finally raised interest rates in March 2022, but even that was by just 0.25%. They still didn’t get it. Only after the issue became unavoidable did the Fed snap into action. For the year, the Fed raised rates seven times, and four of those times were by 0.75%.

The Fed’s target range for interest rates is 4.25% to 4.50%, and that will most likely rise another 0.25% in four weeks.

The Fed consistently fights its current battle with what it should have done in its previous battle. When Covid appeared, the Fed and the Federal government responded massively.

I suspect they were trying to avoid the Fed’s slow response to the Financial Crisis. If you recall, Ben Bernanke famously said that the subprime mess was “contained.” The Fed got the message, eventually.

But in 2020, the Fed jumped into action and thanks to the Fed cutting interest rates to near 0% in 2020, that effectively took risk out of the market. Investors responded as you would guess—they frantically bid up all the risky areas of the market. “Why not? The Fed has our back!” was the reasoning.

Shaky stocks like Peloton (PTON) and Zoom (ZM) zoomed. Zoom did so well that shares of ZOOM also rallied even though it was the wrong ticker. That was the thinking at the time.

Not only that, but areas like Crypto and NFTs soared. Once the Fed started to raise rates, then the high-risk rally got undone. It’s not over. Even today, shares of Tesla (TSLA) fell to another 52-week low.

A little over a year ago, Tesla was going for $414 per share. Today it got down to $105 per share. The losses are so bad that Elon Musk became the first person to lose $200 billion. It’s the greatest loss of fortune of anyone in history. (Don’t worry about Elon, he still has plenty left.)

Our Buy List vs. the S&P 500

Let’s look at some market numbers for 2022. Last year, the S&P 500 lost 19.44%. If we include dividends, then the index was down 18.11%. Our 2022 Buy List was down 10.42%. Including dividends, we were down 9.28%.

If there’s a silver lining to 2022, it’s that the selling was largely concentrated away from the sectors of the market that we prefer. Just by looking at the stats, you can see how much better safe stocks did last year.

For the year, the S&P 500 Growth Index (all these numbers are with divs) was down by 29.41%. The S&P 500 Value Index lost only 5.22%. The S&P 500 High Beta Index was down by 20.31% while the S&P 500 Low Vol Index lost 4.59%. The S&P 500 High Dividend Index fell only 1.11%. Safety was in last year.

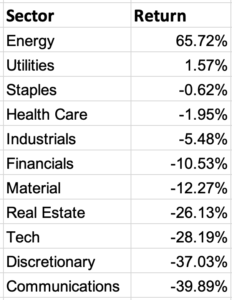

S&P divides the S&P 500 into 11 different sectors. Here’s how the sectors performed last year.

Energy was the big winner. Both Exxon (XOM) and Chevron (CVX) are poised to make a combined profit of $100 billion this year.

I generally steer clear of making economic predictions, but I’m going to make a few qualified exceptions. The first is that I think it’s very likely the U.S. economy will enter a mild recession this year. The timing may take longer than people think, but that is the safe assumption.

By no means do I encourage investors to cut and run. In fact, times like these are often very good times to invest. That’s what bear markets are good for. I’m most concerned about the weakening housing market. Unfortunately, the housing market always finds itself placed between the Federal Reserve and the economy. When the Fed fights off inflation, the housing sector is collateral damage. That’s what’s happening right now.

From Reuters a few days ago:

U.S. single-family homebuilding tumbled to a 2-1/2 year low in November and permits for future construction plunged as higher mortgage rates continued to depress housing market activity.

The dour report from the Commerce Department on Tuesday followed on the heels of news on Monday that confidence among homebuilders plummeted for a record 12th month in December. The housing market has borne the brunt of the Federal Reserve’s fastest interest rate-hiking cycle since the 1980s as the U.S. central bank wages war against inflation.

I also expect the U.S. dollar to lose some steam this year. The greenback has had a good run from early 2021 until a few months ago, but now the European and American economies are out of sync. Our friends across the pond are still hiking and the Fed could be looking to cut rates before the end of the year. In fact, the dollar has already started to pull back since November. A weaker dollar could help cushion the blow of any weaker growth we may face.

Stock Focus: Dollar General

Speaking of the dollar, that reminds me of this week’s stock which is Dollar General (DG). This has been a remarkably successful company and it has a remarkably simple business model. You can get basic items at a discount.

I came close to adding DG to this year’s Buy List as a good replacement for Ross Stores (ROST). What troubled me was its recent earnings report which showed that Dollar General still has supply chain issues. Still, this is a very good company, and it may be worth a closer look.

First, let’s look at how successful DG has been. In 2009, the company IPO’d at $21 per share. Last March, it got to an all-time high of $262 per share. That works out to a return of more than 21% per year for over a decade.

There are now more 18,000 locations across the United States. Dollar General says it has more brick-and-mortar locations than any other retailer in the country. The company was founded in Kentucky in 1939. Even today, the company has a strong southern focus. There are currently more stores in Mississippi than in New York.

Dollar General didn’t get the present name until 1955. The company IPO’d for the first time in 1968. It was later taken private in 2007, slimmed down and then IPO’d again. The company now has a market value of $55 billion.

A few years ago, the company was part of the great Dollar Bidding War of 2014. This involved Dollar General, Dollar Tree and Family Dollar. Dollar General offered nearly $10 billion to buy Family Dollar. The bid was rejected, and Dollar Tree agreed to merge with Dollar General. Honestly, I’m glad Dollar General lost.

It wasn’t a total loss. Dollar General picked up Dollar Express which was a spinoff from the Family Dollar-Dollar Tree deal.

Dollar General works hard to get the lowest possible prices for its customers. DG’s operating margin runs about 10%. This business is all about cost control. Dollar General is also a good business when consumers are worried about inflation.

Dollar General currently pays a dividend 55 cents per share. That’s a tiny yield but I expect to see the dividend increased soon.

Last month, DG reported its fiscal Q3 results. Net sales were up 11.1% to $9.5 billion and same-store sales were up by 6.8%. EPS rose 12% to $2.33 per share.

The problem was that that was an earnings miss of 20 cents per share. It seems that Dollar General continues to face supply chain issues. This has been a big issue for them. Last year, it helped snap the company’s 31-year run of higher same-store sales.

Along with the earnings report, Dollar General slashed its Q4 earnings range to $3.15 to $3.30 per share. Wall Street had been expecting $3.66 per share. The stock fell more than 7% on the news.

I’m going to continue watching Dollar General, but I want to see these problems get behind them before I can consider it a good investment. It’s a great business and it’s a good example of a stock that’s probably not fully valued due to its capacity for growth.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want to learn more about the stocks on our Buy List, please sign up for our premium service. It’s $20 per month, or $200 per an entire year.

Posted by Eddy Elfenbein on January 3rd, 2023 at 6:48 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- August 2026

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His