CWS Market Review – March 21, 2023

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

RIP: Credit Suisse

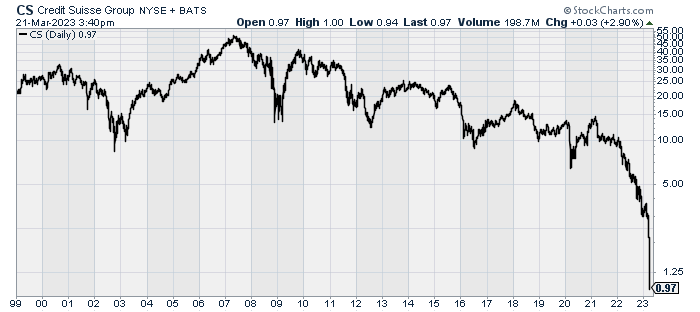

After 167 years, Credit Suisse is no more. The bank has ceased to be. It is bereft of life. This is an ex-bank.

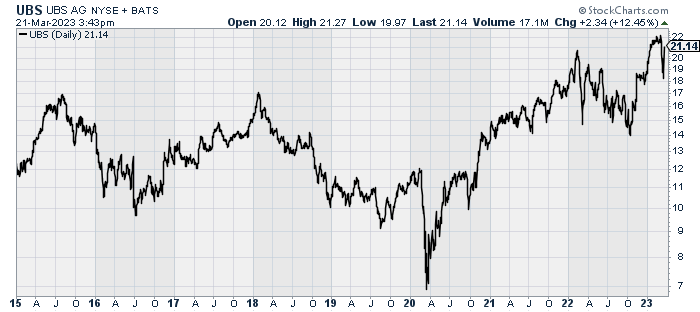

Over the weekend, UBS bought out its long-time rival, Credit Suisse, for $3.24 billion.

This is a major event in global banking. Consider that at the end of last year, Credit Suisse had a balance sheet of half a trillion dollars and 50,000 employees globally. Shares of CS closed Monday at 94 cents.

To say this was a fire sale badly understates the events. The Swiss government essentially forced this deal to happen. They aimed to stop the banking crisis cold. To give you an idea of how far they went, the settled price for Credit Suisse was less than half of Friday’s closing price. It works out to 7% of CS’s tangible book value.

CS shareholders will get one share of UBS for every 22.48 shares of CS they own. That values a share of CS at 0.76 Swiss francs which is 99% below its high.

The Swiss government even sweetened the pot for UBS. The government said it would chip in $9 billion to backstop any losses from the deal. The Swiss National Bank said it would provide $100 billion in liquidity. Investor lesson: When the government—any government—wants a financial outcome badly enough, it’s hard to say “no.”

Mind you, the authorities weren’t crazy. The Swiss government strongly preferred a buyout over a wind-down that would be run by courts, lawyers and regulators. Plus, they wanted a deal done fast. The goal was to have something complete before Asian markets opened on Sunday evening. They made it, but barely.

Frankly, they had to do something. The mess at Credit Suisse was bad and getting worse. The bank was hemorrhaging $10 billion a day. Credit Suisse’s Chairman, Axel Lehmann, said, “The acceleration of the loss of trust and the worsening of the last few days made it clear that Credit Suisse cannot continue to exist in its current form.” That statement was one of the few things they got right.

Banking Is About Confidence

This wasn’t a story of garbage loans. Instead, all the customers headed for the exits. Quite simply, no one believed in them anymore.

That’s the thing about banking. Most people think banking runs on money. It doesn’t. A bank runs on confidence. Once that’s gone, the whole game’s up. It doesn’t matter how much money SNB threw at the problem; without confidence, it wasn’t enough, and it never could be enough.

It’s hard not to have some sympathy for Credit Suisse, but they made just about every mistake they could. They recently got a $4 billion cash injection from the Saudi National Bank on the hopes they could engineer a turnaround. That didn’t happen. Perhaps CS’s biggest mistake was going bust so close behind SVB and Signature.

Last Thursday, the Swiss government extended CS a $54 billion lifeline to make sure they would last until the weekend. Later, they had to double that amount.

Not surprisingly, UBS clearly didn’t want any part of a deal. They realized they were in the strong position, so they asked for a lot, and they got it. During any normal time, the hitching of these two would have been an obvious anti-trust red flag. Not this time. Funny how the government can decide which rules to enforce, when and to whom.

The initial deal that UBS offered was for $1 billion. After shareholders complained, the price tag was lifted to $3 billion, which is still very cheap. As a result of the deal, UBS said it would halt its stock buyback program and pare back its plans for CS First Boston, CS’s investment banking business.

One of the big issues is CS’s investment banking business. CS had been looking to spin it off, and that’s probably not going to happen. They could lose a bundle in scrapping the deal. That’s one of the reasons why UBS was so reticent about taking CS on.

Over the weekend, there was one last-ditch attempt to save CS. A group was planning to inject $5 billion into CS if the government promised to make the bondholders whole. The government turned it down.

I had difficulty keeping up with all of Credit Suisse’s misdeeds. Here are a few.

In 2020, the CEO resigned after it was learned that the COO hired a private investigator to spy on the bank’s former head of wealth management. They wanted to see if he was poaching clients or employees as he had recently transferred to UBS.

Even though the CEO resigned, an investigation found that he had no knowledge of the plan, which raised the question of why was he out of the loop. The scandal later took a tragic turn when the hired private investigator committed suicide.

The following year, Credit Suisse was fined after it was revealed that the bank had bribed government officials in Mozambique and accepted kickbacks. The bank was supposed to be organizing loans to help Mozambique’s tuna industry. The fines would have been higher, but CS agreed to write off some of the loans.

Credit Suisse was also involved in the very strange story of Bill Hwang and his firm, Archegos Capital. Hwang seemed to have no idea what he was doing. Naturally, he was managing several billion dollars.

As you might guess, this came to an unpleasant end. Hwang made a giant and highly-leveraged bet on ViacomCBS (now called Paramount Global). The media company announced a stock sale, and the shares took a big hit. Hwang’s leveraged position started to plunge and he got a margin call. One of my first jobs in finance was making margin calls to clients. When you get a margin call, you have two options: put up more money or sell. If you don’t sell, the firm will do it for you.

According to Bloomberg, Hwang lost $20 billion in two days. He had borrowed tons of money from Wall Street banks, and they were suddenly left exposed. Goldman Sachs and Morgan Stanley moved fast to protect themselves. Credit Suisse did not, and the bank got stung for a loss of $5.5 billion.

Hwang was later arrested and charged with racketeering, securities fraud and wire fraud. Credit Suisse’s reputation never recovered.

What Are CoCo Bonds?

Another odd aspect of this Credit Suisse debacle is that the bonds have been far more volatile than the equity. CS shares are getting shares of UBS. That’s pretty straightforward, but some of the bondholders have been wiped out.

Credit Suisse has what are called additional tier 1 (AT1) bonds. More formally, these are called convertible contingency bonds. Less formally, they’re known as CoCos.

CoCos are bonds that convert into stock if some pre-specified event happens. For example, going bankrupt. CoCos can even be declared worthless, and that’s exactly what happened with Credit Suisse.

On Sunday, the Swiss regulators announced that as part of the deal, Credit Suisse’s AT1 bonds will get a brand-new price of $0. The AT1 investors are furious, and I’m sure this will all be headed to court.

This is one of the hidden aspects of a financial blowup. You never know exactly where it will spread. The AT1 bonds are turning into a major issue. According to the regulators, $17.3 billion of CS’s CoCo bonds have gone up in smoke.

So now folks are wondering why the CoCos got torched when the stockholders didn’t. Traditionally, bondholders outrank equity owners. This has roiled the entire CoCo market. For example, Invesco has an ETF that invests in AT1 bonds. On Monday, it lost close to 6%.

CoCos came about after the financial crisis and became popular with many European banks. Today, there’s more than $250 billion of outstanding AT1 bonds. The bonds were popular with investors. They paid a good deal and the prospect of going bust seemed improbable. Raymond DeVoe famously said, “More money has been lost reaching for yield than at the point of a gun.”

In 2020, Credit Suisse was able to float $1.5 billion in AT1s and they got a rate of 5.25%. They were seen as a safe way of shifting bailout risk to bondholders from taxpayers. That’s why they were afterward called bail-ins instead of bailouts.

But now, the whole CoCo market has gone cuckoo. Everyone had assumed these bonds were safe. Hey, what’s the worst that can happen? Well, now we know. I’ve seen several clips this week of investors furious that their Cocos have been zeroed out. Don’t play the game if you don’t know the risks. In Monday’s trading, Deutsche Bank saw its AT1 bonds drop sharply. So did UBS. Importantly, CoCos are not issued by American banks.

Thanks to this deal they didn’t want, UBS is now one of the largest and most important financial institutions in the world.

Expect the Fed to Hike by 0.25%

I got a good response from last week’s issue when I did a deep dive on what happened at Silicon Valley Bank. That’s why I decided to do the same with Credit Suisse.

But I didn’t want to leave without discussing this week’s Fed meeting. The Fed’s two-day meeting began today and will wrap up tomorrow. The policy statement will be released on Wednesday at 2 p.m. ET.

I expect the Fed will once again hike interest rates by 0.25%. Until recently, I was leaning toward a 0.50% increase, but the events of late have changed that outlook.

At the next meeting in May, I expect another 0.25% hike. After that, however, I think things may change. There’s a good chance that the Fed will take a break for a few months and leave rates unchanged. Of course, this is just a guess and much of what the Fed will do will depend on the behavior of inflation and the economy.

There’s even a decent chance that the Fed will soon shift its bias toward rate cuts, especially if the slowdown in housing spreads to other sectors. The simple fact is that the economy will probably weaken as we get closer to 2024. I hope the Fed will address these issues in tomorrow’s press conference. I’ll have more details in our next premium issue.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on March 21st, 2023 at 6:08 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His