CWS Market Review – March 28, 2023

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

First Citizens Bank Wins the Bidding War for SVB

Two weeks ago, Silicon Valley Bank collapsed in less than 48 hours. The bank lost one-quarter of its deposits in one day. One of the mysteries of this episode is that no one came forward to buy the bank, or even parts of it. The FDIC had to extend the deadline for bids.

Why? How could the collapse happen so quickly yet the bidding on the remains take so long?

Perhaps the remains of SVB were uglier than we were told. Normally, the FDIC likes to sell off any troubled banks as soon as possible to reassure depositors. This time, it had been two weeks and there were still no buyers. There was a deadline, in fact an extended deadline, set for last Friday.

My hunch is that any potential bidder realized that they were in a strong position and could thus extract very lucrative incentives from the FDIC. After all, time was on the bidder’s side and the FDIC isn’t in the bank-running biz.

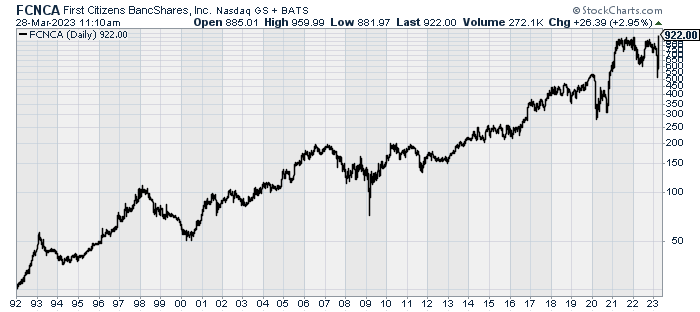

Then it happened. Just before we got to Friday’s deadline, we learned that Valley National Bancorp and First Citizens BancShares (FCNCA) had both submitted bids to the FDIC. Eventually, First Citizens won the deal, and—boy, oh boy—did they win concessions.

An Indirect Bailout

Let’s start with the price tag. First Citizens will take over $72 billion worth of SVB’s assets at a 23% discount. That works out to $16.5 billion, but that’s not all. The FDIC also said it will be part of a loss-sharing deal on the commercial loans that First Citizen is taking over. The deal is to last for eight years. The bank will also get a special credit line for “contingent liquidity purposes.”

As they say on late-night infomercials, “but wait, there’s more!” The FDIC is also giving First Citizens a $35 billion loan to help finance the deal. In exchange, the FDIC will get equity rights in the bank that could be worth up to $500 million.

If this lasted any longer, First Citizens probably could have gotten free Taylor Swift tickets thrown in. They got a sweet, sweet deal. But don’t just take my word for it: on Monday, shares of First Citizens jumped 53.7%. And yet, the FDIC still isn’t done yet with SVB. It’s currently holding about $90 billion of assets in receivership.

All told, the FDIC will take a hit of about $20 billion from SVB and another $2 billion from Signature Bank. That hole will be replenished by higher charges to member banks, which will ultimately be picked up by depositors. One benefit of the soaring share price is that the FDIC will make some money thanks to the equity rights I mentioned. The FDIC has two weeks to exercise those options.

The auction for SVB got a little complicated because most potential bidders were looking at First Republic as their preferred target. Recently, a group of big banks gave a First Republic a badly-needed cash injection, but that didn’t stem the tide.

With the First Republic deal lingering, that may have taken away more interest in SVB’s remains. There’s also the issue that I’ve mentioned before: once a banking panic starts, you never know where it will go next. Bank A can go under and then you suddenly learn that Bank B lent them tons of money and now Bank B is teetering. Then you learn that Bank C is exposed to Bank B. Once the panic gets going, even a well-run bank can be pulled under.

First Citizens Emerges a Big Winner

So who’s First Citizens? It’s a regional bank based in Raleigh, North Carolina. It’s not that big. Or I should say, it wasn’t that big, but it’s a lot bigger now.

First Citizens is an interesting bank because it enjoys snatching up banks from the FDIC. Since 2009, it’s bought more banks from the FDIC than anybody else.

The bank has over 550 branches, and thanks to this deal, First Citizens has joined the big leagues. Three years ago, First Citizens had assets of $42 billion. That will now increase to $219 billion.

One challenge for First Citizens is that banking for the high-tech community traditionally hasn’t been their main business. But First Citizens knows a lot about taking over troubled banks. Over the past few years, First Citizens has taken over Temecula Valley Bank, Venture Bank, Sun American Bank and United Western Bank in Colorado. It’s become adept at folding these troubled banks into its larger business.

From the WSJ:

The longer-term challenge for First Citizens will be running a bank that has dramatically transformed in a short period. The bank will need to hold on to the $56 billion of deposits left at SVB after the majority fled the bank during its meltdown and seizure by the FDIC. It will also have to manage a book of loans to venture-capital firms and startups, and persuade those companies to continue to do new business with the bank.

Executives will have to do that while still digesting another big deal. First Citizens’s $2.2 billion purchase of commercial lender CIT Group Inc. closed in January 2022. CIT owned the remnants of IndyMac Bank, one of the biggest banks to fail during the 2008 financial crisis.

First Citizens has long been controlled by the Holding family. Frank Holding, Jr. is the current Chairman and CEO. The bank has a special class of shares that gives family members 16 times the voting power of ordinary shares.

The line of credit that First Citizens is getting is highly unusual. The idea is that it will protect First Citizens against a mad flight of capital. Between the lines, this tells me how badly the FDIC wanted a deal. Bear in mind that the folks taking over Signature Bank aren’t getting this nice little present from the FDIC.

To its credit, the FDIC has gone out of its way to show the public that SVB is not getting bailed out. The shareholders certainly aren’t. But you could say that there’s an indirect bailout in play. Instead, it’s the new owners who are benefiting from the government’s largesse. I won’t be surprised to see more of these in the future.

Home Prices Are Falling

Earlier today, we got the latest Case-Shiller report on home prices, and housing seems to be the one area of the economy that’s been cured of inflation. Home prices have now fallen for seven months in a row.

Over the last 12 months, ending in January, home prices increased by just 3.8%. That’s down from the 12-month figure for December of 5.6%. According to the report, “All 20 cities reported lower prices in the year ending January 2023 versus the year ending December 2022.” The hottest housing markets are Miami, Tampa and Atlanta, and the coldest are San Francisco, Seattle and Portland.

It’s no secret what’s happening. Higher mortgage rates have made homebuying more expensive. As a result, many potential homebuyers have been driven from the market.

This is the odd part about the Federal Reserve’s interest rate policy. Higher rates don’t slow down the economy broadly. Instead, the housing market stands in between higher mortgage rates and the Fed’s goal of taming inflation. The Fed started hiking rates one year ago, and we still have inflation in the economy, yet housing is under pressure.

Housing analyst Bill McBride points out that with seasonal adjustment, San Francisco has fallen 13.2% from the peak in May 2022, and Seattle is down 11.4% from the peak.

During Covid, mortgage rates dropped to the floor. In November, the average yield on a 30-year fixed rate mortgage peaked at just over 7%. It’s come down some since then. In fact, lower mortgage rates probably saved today’s Case-Shiller report from being worse than it was.

The outlook for housing may change soon. The latest futures prices show that traders see the Fed pausing on interest rates for the next six months. I’ll caution you that these prices are merely guesses as to what the Fed will do. Actually, the next move traders expect is a Fed rate cut in September. If that’s true, it would very beneficial for stock prices.

The next event coming is this Thursday when the government will revise the Q4 GDP. According to the last report, the U.S. economy grew in real annualized terms of 2.7% for Q4. On Friday, we’ll get the latest numbers for personal income and consumption. The Fed prefers to use this data to measure inflation.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want more info on our ETF, you can check out the ETF’s website.

Posted by Eddy Elfenbein on March 28th, 2023 at 6:19 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His