CWS Market Review – March 7, 2023

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

There’s a classic bit from the original Saturday Night Live cast where they parody the Carter-Ford presidential debates from 1976.

During the skit, Jane Curtin, as one of the panelists, asks a very wonkish question alluding to several facts and figures. Chevy Chase, as President Ford (who doesn’t bother trying to look like the president), appears completely bewildered and famously responds, “it was my understanding that there would be no math.”

I mention this because the question Jane Curtin asks has to do with the Humphrey-Hawkins Act, which at the time was only a bill.

Today, it’s a law and its official name is the Full Employment and Balanced Growth Act of 1978. The act is more informally known for its two major sponsors, Congressman Augustus Hawkins and Senator Hubert Humphrey. The act was signed into law a few months after Humphrey died.

The act has an interesting history because it started out as a classic Keynesian bill that aimed for full employment. Instead, the final bill was stripped of those provisions, and it was given a Friedmanite flair. For example, the act requires the Fed to outline its targets for monetary aggregates.

Another mandate of Humphrey-Hawkins is that the Chairman of the Federal Reserve must testify before Congress twice a year on monetary policy. Each testimony lasts two days, one day each before the House Financial Services Committee and the Senate Banking Committee.

Several years ago, I went to the Senate hearing to see the festivities live. I was surprised to find that except for the senators and a few cameramen, the room was nearly empty. I even got the seat directly behind Chairman Bernanke.

Today, Jerome Powell gave his Humphrey-Hawkins testimony before the Senate Banking Committee. In his remarks, Powell said that interest rates will likely go higher than the central bank had expected. The big change is that inflation appears to have reversed its direction and it may be accelerating again.

“The latest economic data have come in stronger than expected, which suggests that the ultimate level of interest rates is likely to be higher than previously anticipated,” Powell said in remarks prepared for two appearances this week on Capitol Hill. “If the totality of the data were to indicate that faster tightening is warranted, we would be prepared to increase the pace of rate hikes.”

Home prices appear to be one of the few areas where prices are going down. This news is especially difficult for the Fed because it had recently downshifted to 0.25% rate hikes. That was seen as a sign that the Fed was winning the battle against inflation. Now that’s in doubt.

In December, the Fed updated its economic projections. At the time, the Fed saw interest rates peaking at 5.1%. In fact, Wall Street thought the Fed was being unduly alarmist. Not anymore. Now traders think the Fed was too optimistic.

Interestingly, Powell didn’t specify how high he thinks rates could go but his remarks had an immediate impact on the market. The two-year Treasury yield broke above 5% for the first time since 2007. Yesterday’s traders thought the odds of a 0.5% hike at the Fed’s next meeting (in two weeks) was 31%. Now it’s up to 70%.

After that, traders expect two more 0.25% increases, one in May and another in June. Traders then expect the Fed to hold tight through the end of the year. There are even some bets that the Fed will start cutting early next year.

I should caution that the futures market is merely a mass of traders placing bets on the future. There are no guarantees, but it’s interesting to note that the perceived ceiling for interest rates keeps rising.

I often talk about the 2/10 Spread because it has a good historical track record in predicting recessions. Today, the 2/10 Spread dropped below -100 basis points. The two-year Treasury now yields more than 1% over the 10-year Treasury. This hasn’t happened in 42 years.

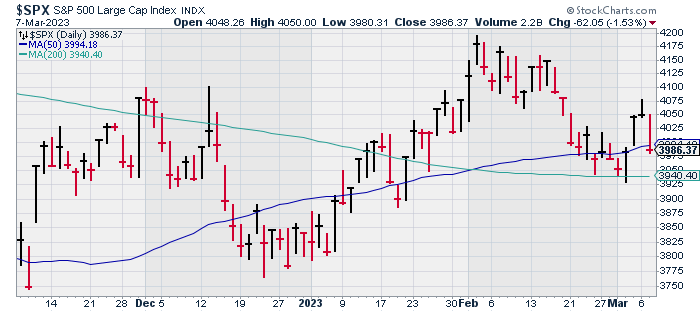

The stock market did not take the Powell news well. At its low, the Dow lost 593 points. The S&P 500 lost over 1.5% today and the index closed below 4,000. The banks got hit especially hard today. The S&P 500 Financial Index lost 2.54% today.

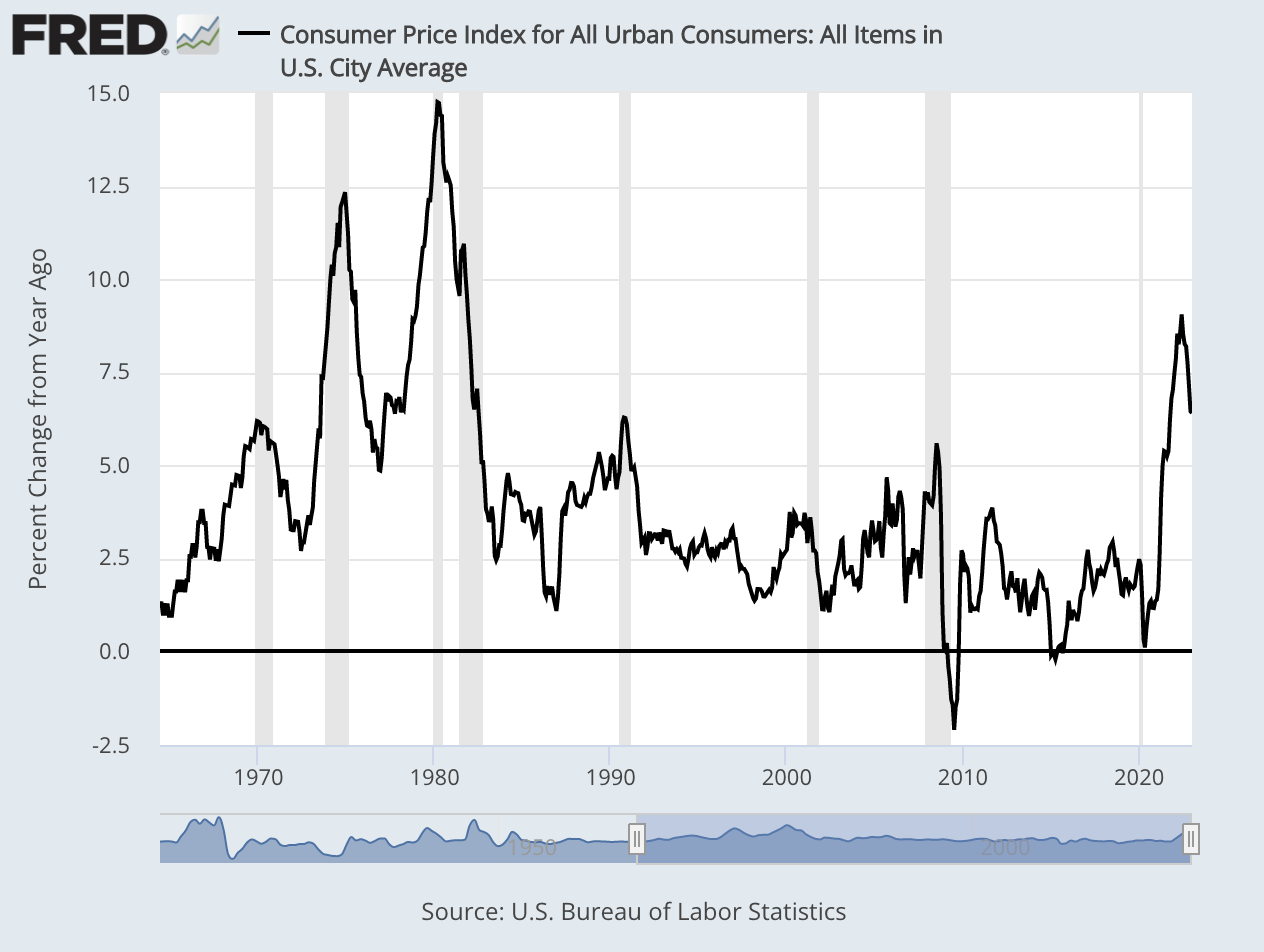

I need to stress how dangerous inflation is for investors. The recrudescence of inflation is the most important obstacle Wall Street currently faces. A depreciating currency may appear beneficial in the short-term, as anyone who remembers the 1970s can attest, but it’s eventually very destructive. In 1977, Warren Buffett wrote an essay on this subject called, “How Inflation Swindles the Equity Investor.”

For businesses, inflation has an unusual impact on the bottom line. Bear in mind that not all earnings are the same. Inflation exacts a heavy toll on asset-heavy businesses. Inflation has an impact similar to putting a magnet near a compass. Everything gets a little screwy. For example, companies with high assets relative to their profits tend to report ersatz earnings.

At first, inflation gives the illusion of prosperity. Businesses create their products in fewer and more expensive dollars and then sell them for cheaper dollars and more numerous dollars. As an accounting item, the business may appear more profitable, but no wealth has been created.

Inflation also favors the debtor in favor of the creditor. Again, any benefit is short-lived. In fact, once lenders see the impact of inflation, the ultimate outcome is to price the marginal borrower out of the credit markets.

Stocks have historically not performed well during periods of high inflation. Inflation is, at root, a tax on capital. In the late 1970s, the stock market’s P/E Ratio dropped well below 10. I don’t even want to think we could return to those kinds of valuations. It’s no accident that Walmart was such a big winner during the 70s since it was so focused on giving shoppers lower prices.

Professor Robert Shiller, a Nobel prize winner, maintains an online database of historical market data. It goes back 150 years. A few years ago, I went through the numbers to see how the stock market has responded to differing levels of inflation.

The stock market has performed well up until inflation gets to about 7%. Anything above that, and the stock market gets ugly. The math isn’t hard. Equity prices are squeezed on two ends. Inflation causes interest rates to rise and that makes for higher borrowing costs. Also, equity valuations are discounted at a higher rate, which translates to lower earnings multiples.

Things may get more dramatic soon. The February jobs report is due out this Friday. Wall Street’s consensus is that the U.S. economy added 250,000 net new jobs last month. After that, the February CPI report comes out next Tuesday.

Stock Focus: Donaldson

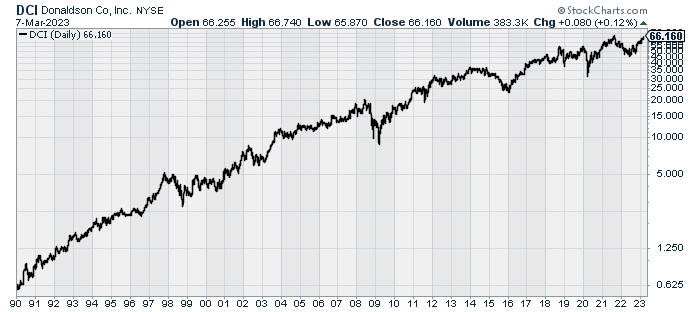

This week, I want to feature Donaldson (DCI). This was a former Buy List stock that I stupidly let get away. Since 1990, shares of DCI are up more than 10,800%.

Donaldson is in the filtration biz which is one of those areas that few people ever think about, but it’s a lot bigger than you might imagine. The company was founded by Frank Donaldson in 1915 and it’s based in Minneapolis, MN.

Donaldson currently has a market value of about $8 billion. It’s a member of the S&P 400 Mid-Cap Index. A few Wall Street analysts follow it, but not many. In the last 35 years, Donaldson has split its stock 2-for-1 five times and once 3-for-2. That works out to 48-for-1.

Last week, Donaldson reported fiscal Q2 earnings of 75 cents per share. That was two cents more than estimates. Donaldson also narrowed its full-year guidance to a range of $2.99 to $3.07 per share. That’s an increase of eight cents to its low end. The company has already made $1.50 per share for its first two quarters. Donaldson expects sales to rise by 2% to 6% this year.

Donaldson currently pays out a dividend of 23 cents per share. The company has increased its dividend for 27 consecutive years. In 1987, DCI paid out a dividend of about one-third of a penny per share.

Wall Street expects DCI to earn $3.17 per share next year. That means the stock is going for just under 21 times next year’s earnings. That’s not bad.

Donaldson reminds me of Peter Lynch’s advice to find companies that are boring. They sound boring. The product is boring and industry is boring. I’d rather not have to wince each time the CEO decides to tweet something.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on March 7th, 2023 at 6:51 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His