CWS Market Review – May 9, 2023

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

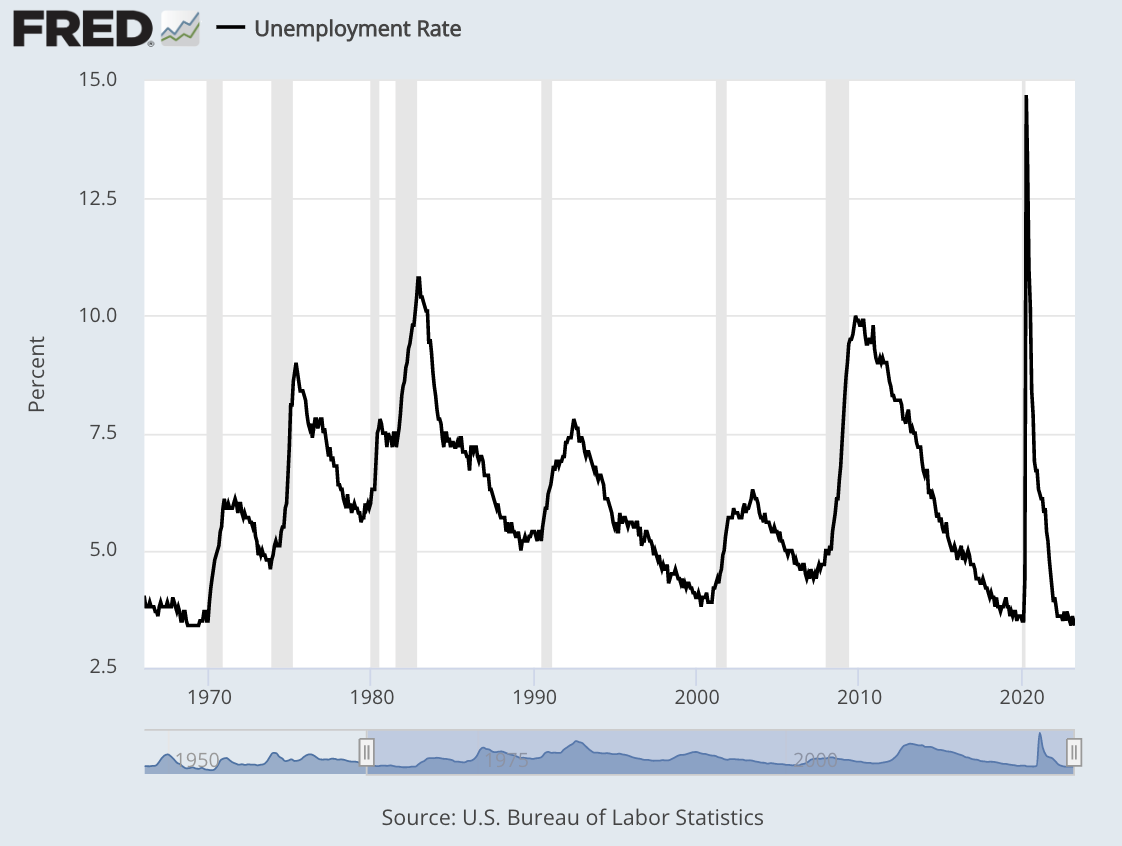

The Unemployment Rate Is at a 54-Year Low

The labor market is as strong as ever. Some folks thought we’d finally see some weakness in jobs, but that is not the case. At least, not yet. The important fact here is that it takes time for the Fed’s policies to work their way to the regular economy.

On Friday, the government reported that the U.S. economy created 253,000 net new jobs last month. That was above estimates for 180,000. The unemployment rate fell to 3.4%. If we work out the decimals, we now have the lowest jobless rate since May 1969 (although the methodology has changed).

The details of the report were pretty good. The broader U-6 rate is at 6.6%. The unemployment rate for African Americans fell to 4.7% which is the lowest since the government started tracking this data in 1972.

It’s also important to look at the workforce participation rate. The Labor Department only counts a person as being unemployed if he or she is actively looking for work. If you’ve given up looking, then you’re no long considered unemployed.

One problem with the workforce participation rate is that it can be heavily influenced by demographics. In this case, that means America’s growing ranks of retired folks. That’s why I prefer to look at the labor force participation rate for prime working-age adults (meaning ages 25 to 54). For April, that was 83.3%. That’s very close to a 21-year high. Ryan Detrick points out that prime working-age employment is also at a two-decade high.

The weak spot continues to be wages. For April, average hourly earnings rose by 0.5%. That’s not that bad, but the problem is that inflation is eating up much of those gains. Over the past year, average hourly earnings are up 4.4%. Tomorrow, the government will release its inflation data for April. I expect to see the trend of declining inflation continue.

What’s the Fed’s Next Move?

Last week, the Federal Reserve decided to raise interest rates for the tenth time this cycle, but this could be the last increase for some time. In previous policy statements, the Fed said that “some additional policy firming may be appropriate.” In last week’s statement, those words were gone.

As you know, dear reader, I’m fluent in the esoteric, jargon-laden language known as Fedspeak. Trust me, those missing words are a big deal. This time, the Fed said that it will “closely monitor incoming information and assess the implications for monetary policy.” This means they’re going to cool off for a few months.

Futures traders took the hint. The Fed meets again in mid-June and the futures prices currently show an 82% chance that the Fed will leave rates alone. For the meeting after that, the one in late July, traders see a 57% chance that rates will be left alone.

Then it gets interesting, For September, the odds are in favor of a rate cut. In other words, traders see the Fed taking back its rate hike from five months before. It’s no secret why: Wall Street is afraid of a recession. The chart above shows the spread between the two- and ten-year Treasuries. It’s been negative for 10 months. A negative spread has often been a precursor of a recession.

Earlier this week, Austan Goolsbee, the top banana at the Chicago Fed, said “I think you have to say that recession is a possibility.” I think that’s the case and financial markets are reflecting that reality.

It’s not all dreary news. One positive note is that this has been a good earnings season. Most of the numbers are in, and Wall Street has been pleasantly surprised with the resilience of corporate earnings.

Q1 Earnings Summary

Here are some numbers from FactSet. So far, 85% of companies in the S&P 500 have reported results. Of that, 79% have topped their earnings estimates. That’s above the 10-year average of 73%. (That’s right. On Wall Street, you’re expected to beat expectations.) The average “beat” has been by 7.0%. That’s also above the 10-year average of 6.4%.

At the current rate, it looks like Q1 earnings will be down about 2.2% from last year’s Q1. This would be the second quarterly decrease in a row. While earnings are down, not too long ago, Wall Street was expecting a larger drop of 6% or 7%. We may not be out of an earnings recession just yet. Wall Street currently forecasts an earnings drop of 5.7% for Q2.

In particular, strong earnings from the Tech and Healthcare sectors have aided the overall earnings environment this season.

Of the companies that have reported, 75% have beaten Wall Street’s revenue forecast. That compares favorably with the 10-year average of 63%. On average, revenues are 2.7% higher than estimates. That’s 1% higher than the 10-year average.

Revenue for Q1 2023 is on pace to be 3.9% above last year’s Q1. That would be the slowest growth rate since Q4 of 2020.

Wall Street expects to see earnings growth return later this year. As I mentioned before, earnings are expected to fall by 5.7% for Q2. For Q3, analysts expect earnings to grow by 1.2% and that will increase to 8.5% in Q4.

I should mention that Wall Street analysts have been known to be somewhat less than precise with their forecasting abilities. FactSet notes that the forward P/E Ratio for the S&P 500 is 17.7. That’s below the five-year average of 17.3.

Trex Jumps 8% on Earnings Beat

After the close on Monday, our favorite deck stock, Trex (TREX), reported very good results for Q1. The stock rallied more than 8% on Tuesday to reach a nine-month high.

I should be humble in talking about our track record with Trex. We added the stock in 2000 and it was an instant home run. Trex was the top-performing stock on our Buy List in 2000 and again in 2001.

Then came the Fed. As the central bank raised interest rates, Trex’s business plunged, and the shares followed. Last year, Trex was our worst-performing stock by far, but we held on.

That’s why Monday’s report was so important. While Trex’s business is still down from last year, the company is healthy again and it continues to deliver profits.

For Q1, Trex has sales of $239 million which was $1 million ahead of expectations. The company earned 38 cents per share which beat the Street by four cents per share.

Thanks to today’s rally, Trex is again our top-performing stock this year (+44%). Not only that, but Trex has beaten the overall market since we first added it more than three years ago, and that includes the disaster year of 2022. This is an important lesson for investors. All companies go through difficult periods, but the strong ones pill through.

“Our performance in the first quarter demonstrated the broad-based appeal of our product line and the continued attractiveness of the outdoor living category as an ongoing secular trend. Supported by our industry-leading brand, manufacturing efficiency, and the strength of our decades-long relationships with best-in-class channel partners in the industry, Trex continued to generate industry-leading margins and profitability,” said Bryan Fairbanks, President and CEO of Trex.

Now for the best news. Trex sees Q2 earnings coming in between $310 million and $320 million. That’s above Wall Street’s forecast for $309 million.

Also, Trex’s Board of Directors approved a big repurchase program of up to 10.8 million shares. That’s 10% of all the outstanding shares. This program has no expiration date.

Shares of Trex closed today up 8.15% to reach $60.89. I’m raising our Buy Below to $65 per share.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want more info on our ETF, you can check out the ETF’s website.

Posted by Eddy Elfenbein on May 9th, 2023 at 6:55 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His