CWS Market Review – July 18, 2023

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

China’s Economy Misses Expectations

On Tuesday, the Dow Jones Industrial Average rose for its seventh day in a row. This is the index’s longest winning streak since 2021. Across those seven days, the index added more than 1,200 points. One of the old sayings on Wall Street is that good markets tend to build on themselves.

There’s some truth to this. Bespoke Investment Group said that this year was the 23rd year since 1945 that the S&P 500 rallied more than 10% during the first half of the year. Of those 22 previous times, 18 saw gains in the second half of the year. The median gain for the back half of the year was 10%.

Of the 55 years when the Dow lost ground or gained less than 10% in the first half of the year, the median second half performance was a gain of just 3.5%. Of course, we’re barely halfway through the year and a lot could happen between now and December 31.

Lately, the big concern hasn’t been about our economy. Instead, the worry is about China’s economy. Yesterday, the Chinese government said that its economy grew at a slower-than-expected rate for the second quarter. This was a bit of a shock. Analysts had been expecting an increase of 7.3%. Instead, it grew by 6.3%.

That number sounds healthier than it really is because it’s compared against a very weak number from a year ago when China was still locked down during Covid.

China’s sour news poses a novel issue for Americans. Many countries around the world have become used to having problems in their economies due to the U.S. economy having problems of its own. For Americans, however, this spillover effect is a new phenomenon. The idea that we can be doing everything right and yet some policy mistake in China redounds on us is rather new. We’re now just dealing with what everyone else has had to contend with.

The problems in China may get worse. The unemployment rate for people aged 16 to 23 is 21.3%. That’s a new record. The unemployment rate for people in cities was 5.2% in June. Earlier this year, China set a growth target for this year of 5%. That may have been overly optimistic.

A few months ago, China relaxed its Covid controls and that helped the economy get an initial boost, but that boost has clearly faded. In fact, the government recently said that China had 0% inflation for June. For the most part, the government has shied away from doing a large-scale stimulus program. It appears that shoppers in China are wary of buying more.

Many countries around the world depend heavily on growth in China to keep their own economies afloat. Plus, many jobs in developed nations have been outsourced to China.

The fear is that slower growth from China could help push the U.S. economy into recession, and this is happening at the same time the Federal Reserve is trying to kill off inflation. This could put the Fed in a tight spot with a need to cut rates at the same time it wants to fight inflation. Treasury Secretary Janet Yellen said that problems in China could impact the U.S. economy but not enough to push us into a recession. We’ll see.

A lot of observers are hoping for a soft landing in the U.S., but weaker growth from China could make that more difficult. It’s not a major problem yet for the U.S. but it could become one soon.

This is coming at the same time as earnings season starts. All in all, I think this will be a fairly mediocre earnings season for Wall Street. Some good and some bad, but it easily could have been a lot worse. For this earnings season, Wall Street expects a 9% drop in profits. If that’s right, then Q2 will be the worst quarter for GDP growth since Q2 2020.

We already have some early numbers. So far, 79.3% of reports have beaten their earnings estimates and 73.3% have beaten their revenues estimates. A total of 62.1% have beaten on both. That’s not bad, but it’s still early.

The major weak spot is Energy. That’s not a surprise. That sector is on pace to post an earnings drop of 48.59%. On the plus side, Consumer Discretionary looks to see earnings growth of 20%.

This earnings season is on track to be the third quarter in a row with an earnings decline. The silver lining is that Q2 will likely be the earnings trough.

Here are some key stats I got from John Butters at FactSet. Quarterly earnings growth for the S&P 500 has exceeded estimates 37 times in the last 40 quarters. Over the last ten years, the average earnings beat has been 6.4%. An average of 73% of companies have topped estimates. In other words, you’re expected to beat expectations. Over the past four quarters, earnings have beaten estimates by “only” 3.2%.

On Thursday, Abbott Laboratories (ABT) will be our first Buy List stock to report this earnings season. Three months ago, ABT topped earnings and the stock jumped 8% in one day. This time, Wall Street expects ABT to report earnings of $1.05 per share. My numbers say it will be closer to $1.10 per share. ABT is a very good company.

The U.S. Dollar Tumbles

One area of concern lately has been the slumping U.S. dollar. There’s been a lot of scaremongering about the “pending collapse” of the dollar for a long time. In fact, the dollar already gave us a bearish head fake a few months ago. I use these words cautiously, but this time may really be different.

With investors betting that the Fed’s rate hike cycle is coming to an end, and with possible rate cuts not too far off, this leaves the dollar in a tight spot. Bear in mind that rate cycles tend to last a few years rather than a few weeks. Traders see the Fed starting to cut rates in March of next year.

Currency traders aren’t wasting any time. The U.S. dollar is currently going through its worst drop since November and is now at its lowest level in more than a year. Not only is the dollar weak, but it may stay weak for some time. The recent drop has also helped spark gains in oil and gold.

The Fed meets again next week and will almost certainly raise interest rates by 0.25%, but what about after that? The outlook gets murkier, but the Fed may stay on the sidelines for several months.

The fear is that there could be a mismatch between Fed policy and the European Central Bank. For example, if the Fed calls off its inflation battle at the same time the ECB is hiking, that could lead to a dollar rout. I doubt it will happen, but it’s not an unreasonable fear.

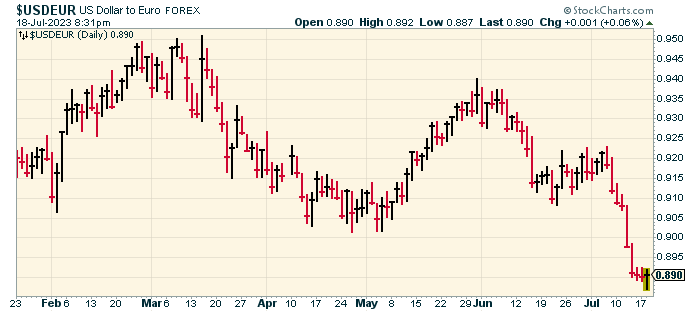

Here’s a very ugly chart of the dollar versus the euro:

It’s hard to avoid the simple fact that the dollar is probably overvalued. Bloomberg notes that the real effective exchange rate for the Japanese yen is at its lowest point in decades.

We may be witnessing an unwinding of the “carry trade.” This refers to a strategy of borrowing in a low-yield currency like the yen and buying a higher-yielding one like the dollar. So far in 2023, this has been a no-brainer move but it may be coming to an end.

The yen-dollar is only one such pairing. Investors have also been playing the carry trade with emerging market currencies.

On Tuesday, we got the retail sales report for June. This is an important report because if shoppers are in a good mood, then the economy will likely do well. Unfortunately, shoppers were a little sluggish last month.

For June, retail sales rose by 0.2%. That’s not adjusted for inflation. Economists had been expecting an increase of 0.5%. The rate for May was revised to 0.5%. Consumer spending makes up roughly two-thirds of the economy.

Consumer spending tends to be tied to the strength of the labor market. The June payroll figure, while still positive, came in well below the figure for May. Gary Alexander reminds me that the Conference Board said earlier this year that a recession in the coming 12 months was 99% certain. The same group recently reported that their June Consumer Confidence survey turned positive for the first time since January of 2022.

Interestingly, Goldman Sachs just cut its odds of a recession happening over the next 12 months from 25% to 20%. I’m ready to christen 2023 “the year of the recession that never came.” We’ll know more on July 27 when the government releases its initial estimates for Q2 GDP growth.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want more info on our ETF, you can check out the ETF’s website.

Posted by Eddy Elfenbein on July 18th, 2023 at 6:23 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His