CWS Market Review – August 22, 2023

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

China’s Growth Model Hits the Wall

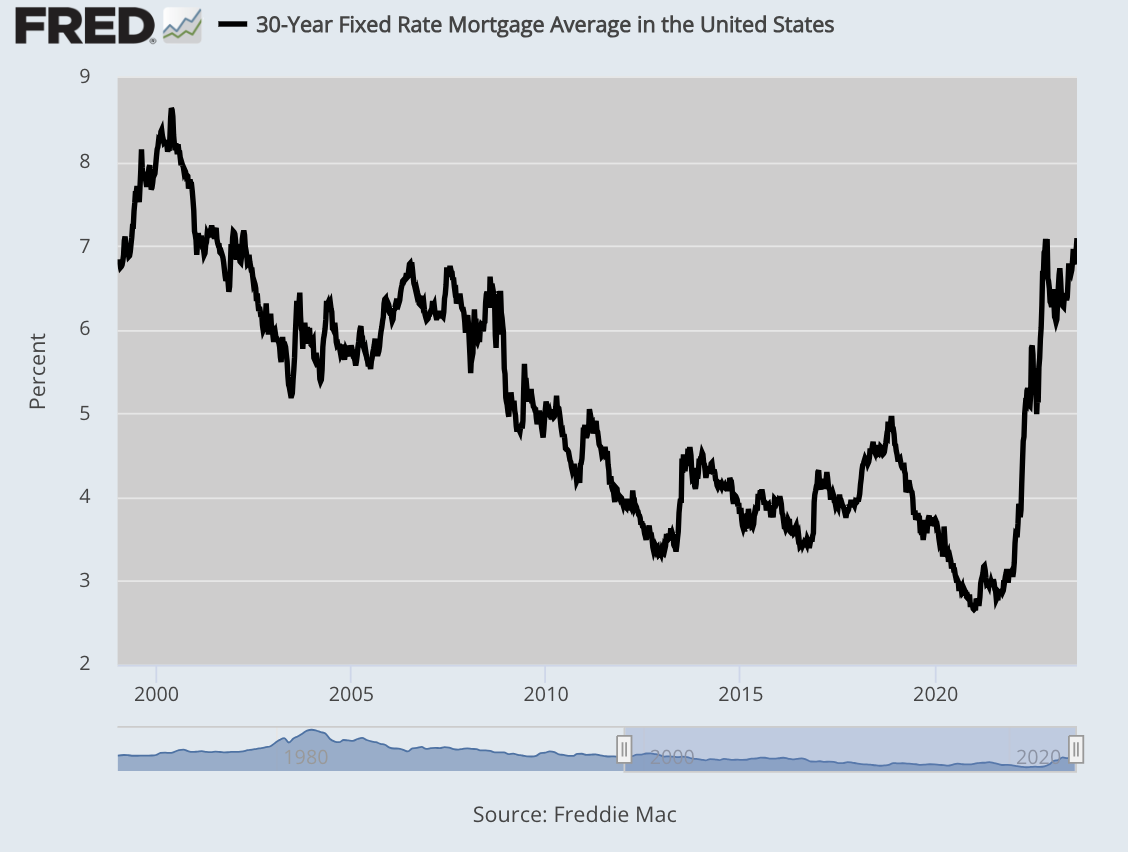

Americans have been unnerved by the recent rise in mortgage rates. According to Freddie Mac, the average 30-year fixed-rate mortgage is now over 7%. That’s a 21-year high.

On Tuesday, the existing-home sales report said that sales in July were down 2.2% from sales in June. Compared with one year ago, sales are off by more than 16%. This was the slowest July since 2010.

Last month, there were only 1.11 million homes on the market. That’s tiny. For context, that’s about half as many homes as were on the market before Covid, and it’s the lowest number in nearly a quarter of a century.

As rough as those numbers are, they’re peanuts compared with what’s happening in China. That country’s real estate sector appears to be going through a full core meltdown, and the damage isn’t limited to real estate. It’s starting to get folks to wonder if China’s entire model for economic growth is flat-out wrong.

The Chinese economy used to be the gem of the Far East and a global growth superpower. Not anymore. The country is mired in debt, and it’s addicted to overbuilding.

For four decades, the Chinese economy roared ahead. We heard countless stories about China’s emergence as a global superpower. We even heard from some observers in the West that China provided a blueprint for future development. Soon, we were told, China would replace the United States as the world’s largest economy.

The old playbook was simple: borrow and build. When in doubt, borrow and build. That was followed by even more borrowing and even more building. To help spur all the borrowing, Chinese state banks set rates artificially low. Now China has millions of apartments with no tenants and cities with no people. Even some small cities have multiple airports.

Don’t get me wrong. The borrow-and-build model is a great idea, but it needs two things. One is tons and tons of Western money pouring in. The other is rising prices. As long as you have those, there’s nothing to worry about.

Once the reverse happens, then things get bad. Really bad.

On Monday, the People’s Bank of China (i.e., the Chinese Fed), responded to the real estate mess by, what else, cutting interest rates. The problem was that the cut was only by 0.1% which was less than expected. In fact, a lot of observers ignored it as a token gesture, which it is.

The benchmark for one-year corporate loans fell from 3.55% to 3.45% while the benchmark for five-year loans was unchanged at 4.2%.

That’s not enough to do the trick. The ultimate judge on any policy is how the markets react, and traders didn’t like the puny rate cut. The Hang Seng Index, which is based in Hong Kong, fell 1.8%. It’s now down more than 12% this month. The yuan recently hit a 16-year low.

The real estate mess is bad and it’s getting worse. Country Garden is the latest to run into trouble. The developer “has hundreds of billions of dollars in unpaid bills,” and it just got booted off the Hang Seng.

Not that long ago, Country Garden was hailed as the model company. The New York Times notes that, “More than 50 developers have already defaulted or stopped paying on overseas bonds.” They’ve simply run out of money.

So much of China’s economy revolves around real estate. In July, new-home sales in China were down by one-third from last year. In June, new home sales were off by 28%.

For years, millions of Chinese citizens moved from rural areas into big cities. In response, the country built massive amounts of urban housing. They struggled to meet demand. They built way too much and now demand has plunged.

It’s not just housing. The government has spent billions of dollars trying to make a world-class independent semiconductor industry. That hasn’t worked out. In terms of sophistication, their chips are still way behind Taiwan’s.

China’s problems don’t end there. Two weeks ago, I told you about how the American and Chinese economies are being decoupled. That’s threatening China’s foreign investment and trade. Now economists are concerned about China’s future.

What will the future look like? The International Monetary Fund puts China’s GDP growth at below 4% in the coming years, less than half of its tally for most of the past four decades. Capital Economics, a London-based research firm, figures China’s trend growth has slowed to 3% from 5% in 2019, and will fall to around 2% in 2030.

In 2020, President Xi Jinping said his goal was to double China’s economy by 2035. That looks like it won’t happen. Nor is China about to dethrone America as the world’s largest economy.

Normally, if you want to get an economy moving, you can try boosting credit and leverage your way forward. China is at the point where it can’t do that anymore.

Truthfully, cracks have been showing in China’s economy for some time. Covid just sped things up. China’s explosive housing market helped masked the problems that had been growing just beneath the surface. Now the housing bubble has popped.

The outlook has darkened considerably in recent months. Manufacturing activity has contracted, exports have declined, and youth unemployment has reached record highs. One of the country’s largest surviving property developers, Country Garden Holdings, is on the cusp of a possible default as the overall economy slips into deflation.

The big fear is that China won’t merely slow down but that it will enter a multi-decade period of low growth similar to what Japan’s been through. There is, however, one major difference. When Japan hit the wall, it was already rich. China isn’t nearly as developed.

800 Million Have Been Lifted Out of Poverty

Another fear is that a weaker economy might lead to a more aggressive foreign policy. That may already be happening. President Biden recently said that China’s economy is a “ticking time bomb” that will cause it to do “do bad things.” That didn’t exactly go over well in Beijing.

Youth unemployment is so bad that the government has stopped reporting the numbers. The last report was for June. It said that the jobless rate for urban 16 to 24-year-olds was 21.3%.

The growth story dates back to 1978 when Deng Xiaoping opened China’s economy to free enterprise. It’s hard for us today to imagine how poor and backward China was. Millions of Chinese lived as peasants, not very different from how their ancestors lived.

According to numbers from the World Bank, since the free market reforms, China’s per capita has increased 25-fold, and 800 million people have been lifted out of poverty.

Forty-five years later, China has massive ghost cities. It’s estimated that 20% of China’s urban apartments are vacant. That’s 130 million units. They’ve built cities that no one lives in, and airports and rail networks that no one uses.

The borrow-and-build philosophy has already picked the low-hanging fruit. Now the return on investment in China is far lower. Instead of facing the problem, the government has encouraged even more borrowing. In ten years, China’s total debt has grown from 200% of GDP to 300% of GDP.

Here’s a chart of the yuan to the dollar:

There is an obvious solution to China’s problem: make the economy more balanced. For that, it needs to promote its consumer sector. That means that Chinese consumers need to spend more and save less. The problem with that is that the government would have to give up some control over the economy and replace it with individual choice. That kind of thinking doesn’t come easy to the Chinese Communist Party.

The big worry is that China’s problems will spill over into the United States, but for now, I think that’s very unlikely.

This may sound odd, but the U.S. economy really isn’t heavily exposed to China. Of course, we’re talking about very large sums.

The U.S. currently has about $215 billion in direct investment in China and about $300 billion in portfolio investment. Paul Krugman points out that U.S. office buildings are worth about $2.6 trillion which is about five times our total investment in China.

What about demand from China? That’s not that big, either. Last year, China bought about $150 billion worth of goods from us. That’s less than 1% of our GDP. That means a downturn in China will barely be felt in the U.S. As troubling as the mess in China is, we don’t have much to be fearful of.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want more info on our ETF, you can check out the ETF’s website.

Posted by Eddy Elfenbein on August 22nd, 2023 at 6:51 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His