CWS Market Review – August 29, 2023

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

Jay Powell Gives Stocks a Boost

“August, die she must.” So sang Simon and Garfunkel. Indeed, the month of August is nearly over, and it’s been a slightly negative one for Wall Street. Through Tuesday, the S&P 500 is down 2% for the month. Of course, that’s not a very big drop in any historical context, but it could be our first monthly loss since February.

Interestingly, when the mini-selloff started at the beginning of the month, growth stocks took much of the heat. That’s standard for a downward market, but then things changed, and it was value suffering the most.

The S&P 500 even closed below its 50-day moving average for nine days in a row. The streak finally ended today thanks to a nice three-day rally on Wall Street. In fact, the S&P 500 just posted its best three-day run since March.

On Tuesday, the S&P 500 had its best day since June 2. If you want to split hairs, Tuesday’s gain was a millimeter behind the gain from June 2 (1.453% to 1.451%).

What’s the cause for the late-August optimism? That’s no secret. It was largely due to the Fed Chairman Jerome Powell’s tempered outlook at Jackson Hole this past weekend.

On the weekend before Labor Day, the Federal Reserve holds its annual powwow in Jackson Hole, WY. On Friday, Jerome Powell gave a speech in which he stressed the need to be vigilant against inflation. That’s pretty much boilerplate for any big Fed conference although he did say that more rate hikes may be coming.

Powell didn’t give a lot of details, but he did say that the Fed has made considerable progress in fighting inflation. Last summer, the 12-month inflation rate peaked at more than 9%. It’s down by about two-thirds since then. Bear in mind that prices are still rising, just at a slower rate.

Powell said, “We are prepared to raise rates further if appropriate and intend to hold policy at a restrictive level until we are confident that inflation is moving sustainably down toward our objective.”

While that sounds tough, it’s noticeably different from last year’s Jackson Hole conference. That’s when Powell made headlines by saying that “some pain” will be needed to confront inflation. That line seriously rattled the markets. In fact, stocks didn’t turn positive until October.

This year, markets are far more pleased. I think many observers were concerned that Powell would deploy more “some pain”-type of rhetoric. That didn’t happen and stocks and bonds are rallying. Over the last week, the yield on the 10-year Treasury has fallen by 0.2%.

We don’t have the August inflation numbers yet, but the core inflation rates for both June and July were 0.2%. That’s pretty good. Powell agreed that those numbers are good, but he added that it’s “only the beginning of what it will take to build confidence that inflation is moving down sustainably toward our goal.”

The Fed is winning the war against inflation, but it’s important to stress that the battle isn’t over just yet.

Another good development is that the Fed has reduced its gigantic balance sheet. The Fed has allowed nearly $1 trillion worth of bonds to roll off since the middle of last year.

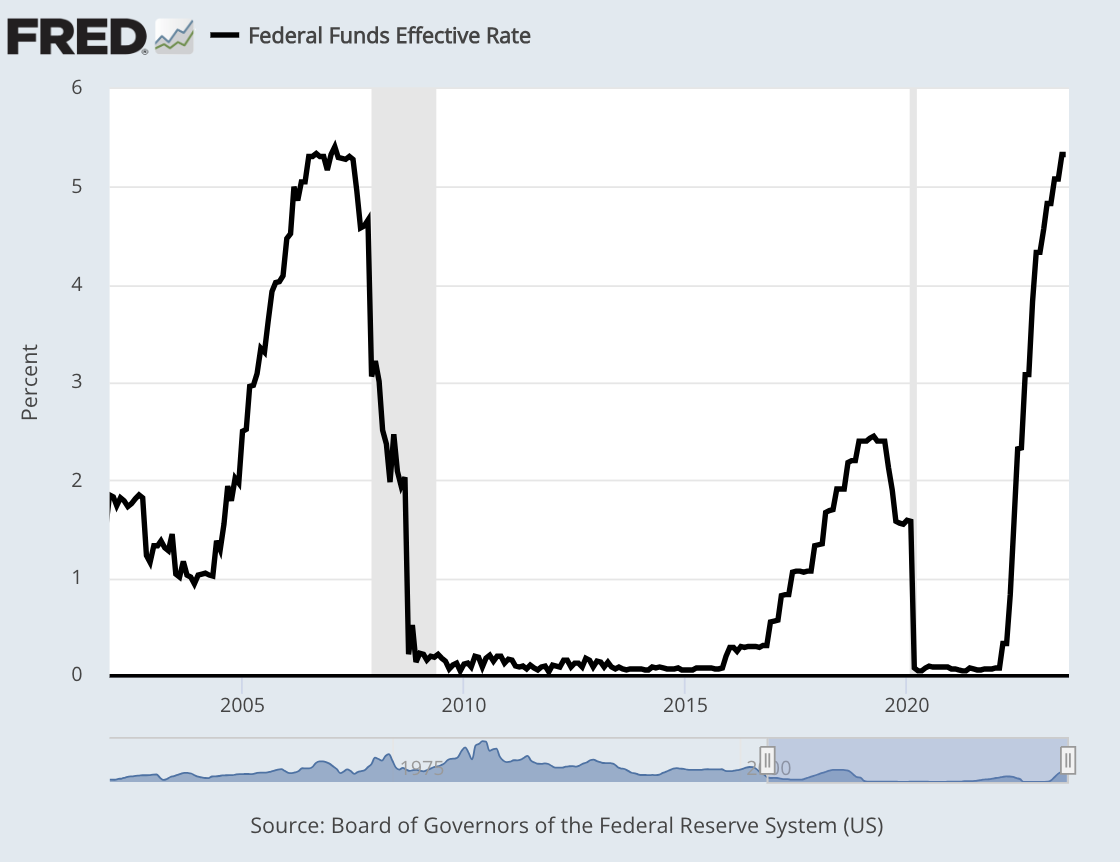

The Fed meets again in three weeks. This will be another meeting where the Fed will update its economic forecasts. For now, the futures markets largely expect another pause from the Fed. That means the central bank will vote to keep its target range for the Fed funds rate at 5.25% to 5.50%. Interest rates haven’t been this high in 22 years.

After next month’s meeting, things get a little cloudy. The Fed won’t meet again until early November. Right now, it looks to be a tossup on the odds for another rate hike. Futures traders are about evenly divided between a 0.25% rate hike and another rate pause. Obviously, the data between now and then will help tip the balance.

We can’t say for certain, but this could be end of the Fed’s rate-hiking cycle. Even if there’s another hike or two coming, the long series of hikes is mostly likely past us. Traders currently think there’s a decent shot of a Fed rate cut by May. I’m skeptical but I understand that investors are concerned about future economic growth.

Higher interest rates have an important influence on investors as they force investors to become more conservative with their portfolios. Cheap money can initially reward foolish ideas. Those rewards often don’t stay for long.

Better’s SPAC Goes SPLAT

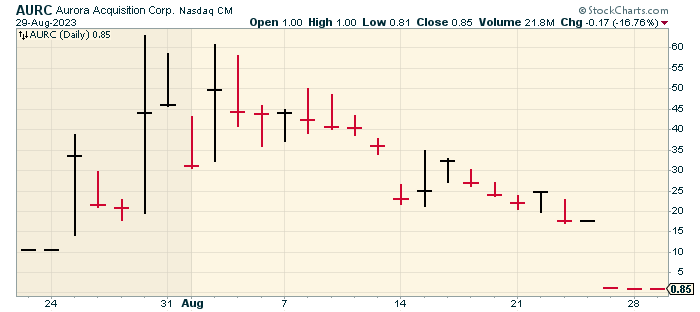

Speaking of silly behavior, Better.com (BETR) has seen better days. The online mortgage lender went public this week, but not by the traditional route.

Instead, Better.com’s parent company, Better Home & Finance, merged with Aurora Acquisition Corp. (AURC)

Never heard of them? Well, you’re not alone. Aurora is a Special Purpose Acquisition Company, better known as a SPAC.

SPACs are basically shell companies that are already listed on the exchanges. Instead of going public through an IPO, a SPAC will buy an unlisted company thereby making it publicly traded. That way, it skips a lot of bureaucratic steps.

If you think SPACs are sketchy, I agree. The day before the Better deal, shares of Aurora were trading at $17.44. After the deal, the stock fell to $1.15. Now it’s at 85 cents per share. The SPAC is now a speck.

SPACs were all the rage a few years ago. It’s amazing how low interest rates can make smart people do a lot of silly things. In Q1 of 2021, 278 SPACs hit the market. In Q2 of this year, only four went public. In Q1 of 2021, 98 SPAC deals were announced, but only 100 in the first half of this year.

Bloomberg notes that there have been 11 SPAC deals this month. Nine of them are in the red. The median loss is 41%. Roughly 40% of the 400 SPACs now trade below $2 per share. Most SPACS started at $10 per share so we’re talking about an 80% loss.

Better is fighting two headwinds at the same time. It’s a terrible market for SPACs and it’s a lousy market for mortgages. Better is already considered somewhat shady. This is the company that made the news two years ago when it fired 900 employees over Zoom. These aren’t exactly PR geniuses we’re dealing with.

If that’s not enough, the SEC delayed Better’s SPAC deal until it concluded an investigation to see if it had violated securities law. The SEC ultimately decided against any enforcement action.

Better is only the latest in a series of SPACs than have gone splat. Shares of WeWork (WE) and Virgin Galactic (SPCE) have both been crushed. Virgin Orbit and Pear Therapeutics both filed for bankruptcy. WeWork may not be far behind.

It really is all driven by interest rates. When rates are high, the future is expensive, but when rates are low, the future is cheap — and sometimes it gets too cheap.

That’s all for now. The stock market will be closed on Monday for Labor Day. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want more info on our ETF, you can check out the ETF’s website.

Posted by Eddy Elfenbein on August 29th, 2023 at 6:53 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His