CWS Market Review – August 8, 2023

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

The Age of Decoupling

One of the important changes impacting the U.S. economy is that American companies are altering their businesses so they’re not as dependent on China.

The buzzword is “decoupling,” and it’s been happening quickly. Through May, imports from China are down 24%. Some of it is politics, but a lot of it comes down to simple economics.

Thanks to decoupling, America’s top trading partner is now Mexico. Adjusted for inflation, the value of imports from China are down 12% over the last five years. Meanwhile, imports from Mexico are up about $10 billion compared with the same period last year.

Decoupling shows little sign of slowing down. On Tuesday, China said that exports fell by 14.5% in July from a year ago and imports dropped by 12.4%. That was much worse than expected. Exports to the U.S. fell by 23.1%. Exports from China have fallen for three months while imports are down for five months in a row.

After growing quickly for several years, the Chinese economy is in a bad state. Domestic demand has slowed to a crawl. Even after Covid restrictions were lifting, the economy didn’t see a rebound.

American companies have come to realize that it’s risky to have so much of their supply lines dependent on China. We’re also seeing that retailers like Target and Walmart are ordering fewer Chinese goods. For example, China’s share of personal computers fell from 61% in 2016 to 45% last year. For printers, China’s share fell from 48% to 23%.

For many years, China was incredibly important to global manufacturing, but that position is being challenged. It’s still important but countries like Mexico, Vietnam and Thailand are gaining market share. The interesting part of this change is that it’s happening not from governments but from businesses.

When Donald Trump was president, the U.S. government placed tariffs on several Chinese-made goods. Also, Chinese workers have been getting higher pay, and that cuts into the country’s former strength as being the low-cost producer.

It’s not just the U.S., but it’s been happening in Japan as well. Companies are opening fewer manufacturing facilities in China.

We’re also seeing Chinese firms trying to bypass the tariffs. For example, companies will build nearly everything in China and then send it to Mexico for final assembly. The products are really made in China but are stamped as being made somewhere else.

This is important because in the U.S., the Federal Reserve has been fighting inflation by hitting demand. In response, consumers are shifting their spending from goods to services. That leaves Chinese-made goods on the outs. This change may last a long time. We’re now living in the Age of Decoupling.

The July Jobs Report: OK But Not Great

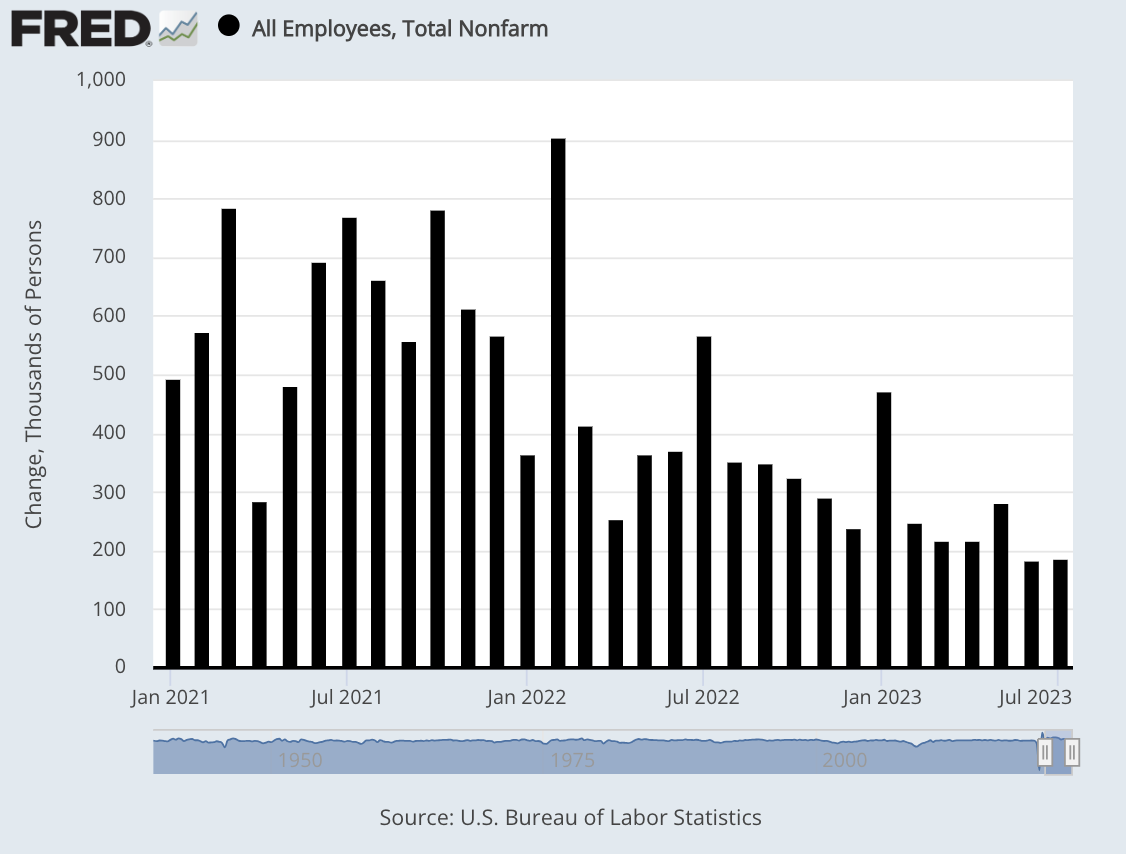

Despite many predictions of its imminent demise, the U.S. labor market continues to churn out more jobs, albeit at a slower rate. On Friday, the government released the jobs report for July. According to the Bureau of Labor Statistics, the U.S. economy created 187,000 net new jobs last month.

To be frank, that’s an okay number but not a great one. Wall Street had been expecting a gain of 200,000. July was the slowest month for job gains since December 2020 when the economy shed 268,000 jobs.

In this chart, you can really see the drop in job gains:

The year-over-year percentage of jobs gained has declined 16 times in the last 17 months. In other words, the economy is still creating new jobs but at a progressively slower rate.

Some of the details are encouraging. Private payrolls increased by 172,000. We’re also seeing better numbers for wages. Last month, average hourly earnings rose by 0.4%. That was 0.1% better than expected. Over the past year, average hourly earnings are up 4.4%. The problem is that inflation has taken a big bite out of workers’ paychecks.

Here are some more details:

Health care led job creation by industry, adding 63,000 jobs for the month. Other sectors contributing included social assistance (24,000), financial activities (19,000) and wholesale trade (18,000). The other services category contributed 20,000 to the total, which included 11,000 from personal and laundry services.

Leisure and hospitality, which has been a leading sector for most of the recovery in the Covid pandemic era, added just 17,000 jobs, consistent with a slowing trend after averaging gains of 67,000 a month in the first three months of 2023.

Previous months’ totals were revised lower — the June count dropped to185,000, a downward revision of 24,000, while May was cut to 281,000, down 25,000 from the previous estimate.

Economists like to look at the broader U-6 rate which is often referred to as the underemployment rate. For July, that was 6.7%. That’s not far from the cyclical low of 6.5%.

The unemployment rate ticked down to 3.5%. On Twitter (or X), I noted that “The unemployment rate is lower today than *at any point* in the 1970s, 80s, 90s, 00s and 10s.”

This prompted several responses telling me to look at the labor force participation rate. Here’s a sample:

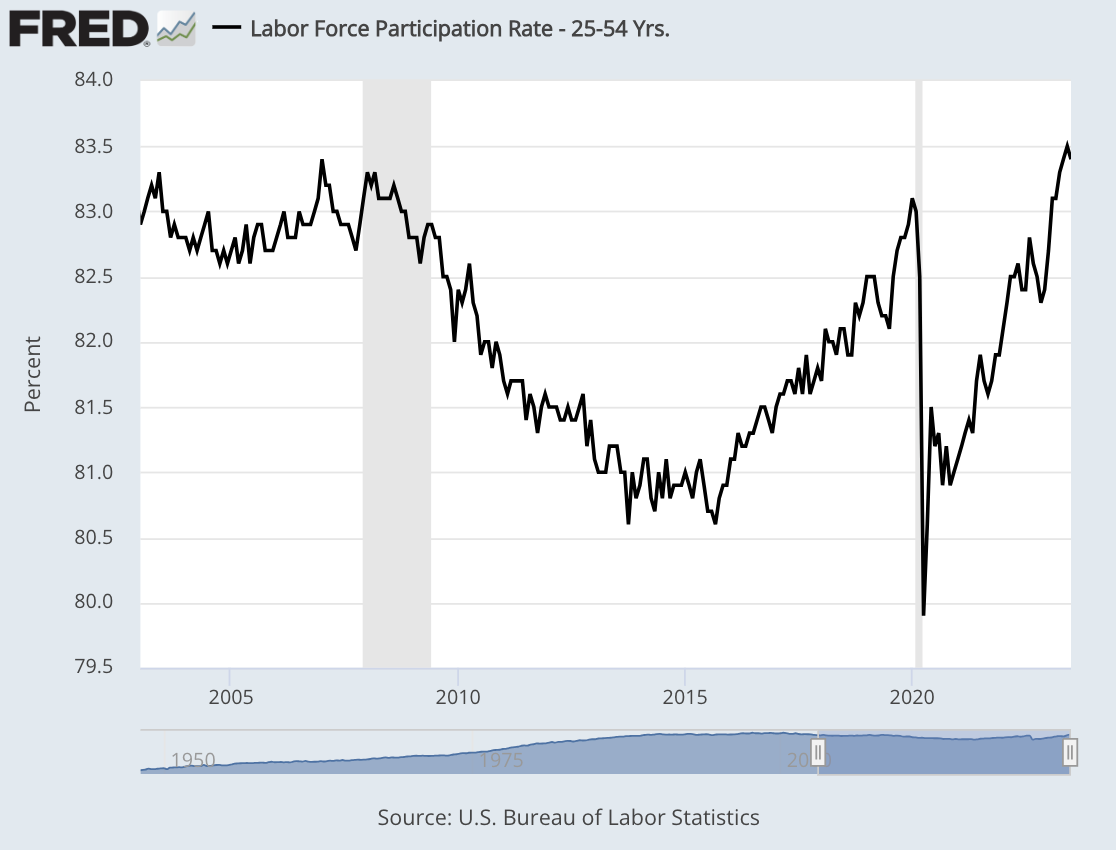

Well, let’s go for it. The labor force participation rate (LFPR) measures the percentage of people who are employed or are actively looking for work.

There seems to be a widespread belief that the only reason that the unemployment rate is low is because the government doesn’t count the people who have stopped looking for work.

This is simply incorrect. For July, the LFPR rate held at 62.6% for the fourth month in a row. That’s the highest it’s been this cycle.

In an interview with the New York Times, John C. Williams, the president of the New York Fed, said “we’ve seen the labor force participation, labor force growth improve quite significantly.”

It’s true that during Covid, many folks left the work force, but they’ve come back. At its low, the labor force participation rate got to 60.1 in April 2020. The current LFPR is below its pre-Covid high, but it’s not that far from it. The fact is that the workforce has largely returned to normal.

Here’s the catch. That LFPR can be influenced by demographic factors such as the growing number of retirees. It’s not that bummed out young people have stopped looking for work. Instead, it’s that grandma and grandpa have retired and moved to Florida.

That’s why I prefer to watch the labor force participation rate for people from ages 25 to 54. That helps us skirt the age issue. For July, that was 83.4% which is close to its highest level of the last 20 years. June’s rate was 83.5% which is the highest since May 2002.

There are plenty of criticisms for the economy. The pace of jobs growth is rapidly slowing, and wages lagged inflation for several months, but we absolutely have not seen a mass exodus from the jobs market.

The next big econ report will be this Thursday when the CPI report for July is out. The inflation numbers have improved over the past year, but tackling the last bit may prove difficult.

For the 12 months through June, consumer prices increased by 3%. The core rate, which excludes food and energy, increased by 4.8%. For Thursday, Wall Street expects the 12-month headline rate to rise to 3.3% and the core rate to drop to 4.7%.

Currently, the futures market expects the Fed to pause again at its meeting on September 19-20. In fact, the futures don’t see the Fed making any changes until March 2024, and that first move is expected to be a rate cut. Until then, don’t let scary headlines make you flee the market.

The FTC Finally Gives In

One of our favorite Buy List stocks is Intercontinental Exchange (ICE). The company owns the New York Stock Exchange, plus a few other financial exchanges. Last week, the company released another solid earnings report ($1.43 vs $1.37 est.). What I like about the business is that ICE’s operating margin often runs around 60%. ICE has grown by using a series of aggressive but shrewd acquisitions.

More recently, ICE started moving into mortgage technology. In 2020, ICE bought Ellie Mae, a mortgage technology business, for $11 billion. This strategy took a very big leap last year when ICE said it was buying Black Knight (BKI), a mortgage data vendor, for $11.7 billion.

That got the attention of the U.S. Federal Trade Commission. They didn’t like the deal at all. The government felt that an ICE/Black Knight deal would put too much power in too few hands. The key to understanding the deal is that it’s all about data.

The FTC contends that such a deal would stifle innovation and raise prices for consumers. Lina Khan, the head of the FTC, has gotten a lot of attention for her aggressive policies against corporate mergers. The problem for the FTC is that it hasn’t been doing well when its battles go to court. The FTC failed in its attempt to block Microsoft’s $70 billion acquisition of Activision. Leaving that aside, the FTC has been doing everything it can to scuttle the Black Knight deal.

ICE and Black Knight struck back by selling off different units to appease the FTC. For example, Black Knight said it would sell its Optimal Blue business for $700 million. The company also said it would sell its Empower loan origination system business.

The strategy finally worked, and the government threw in the towel. Yesterday, the FTC told a federal court that it will drop its lawsuit trying to stop the deal from going through. The trial had been set to start on Monday, August 14.

Not that long ago, the merger deal was viewed as hopeless. The deal price was for $75 per each share of BKI. Less than a month ago, shares of BKI were trading for around $58. That’s changed. Yesterday, BKI rallied 4% to close at $74.36 per share. This is a big victory for Intercontinental Exchange.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want more info on our ETF, you can check out the ETF’s website.

Posted by Eddy Elfenbein on August 8th, 2023 at 7:06 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His