CWS Market Review – November 14, 2023

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

Stocks Soar on Soft Inflation Report

Finally, some good inflation news!

This morning, the government said that inflation was unchanged last month. That was 0.1% below expectations. Not surprisingly, the report was helped by falling energy prices. Over the last year, inflation is running at 3.2%.

This is a very good report. Bear in mind that inflation was running very hot in September (+0.4%), so this report is a nice change of pace.

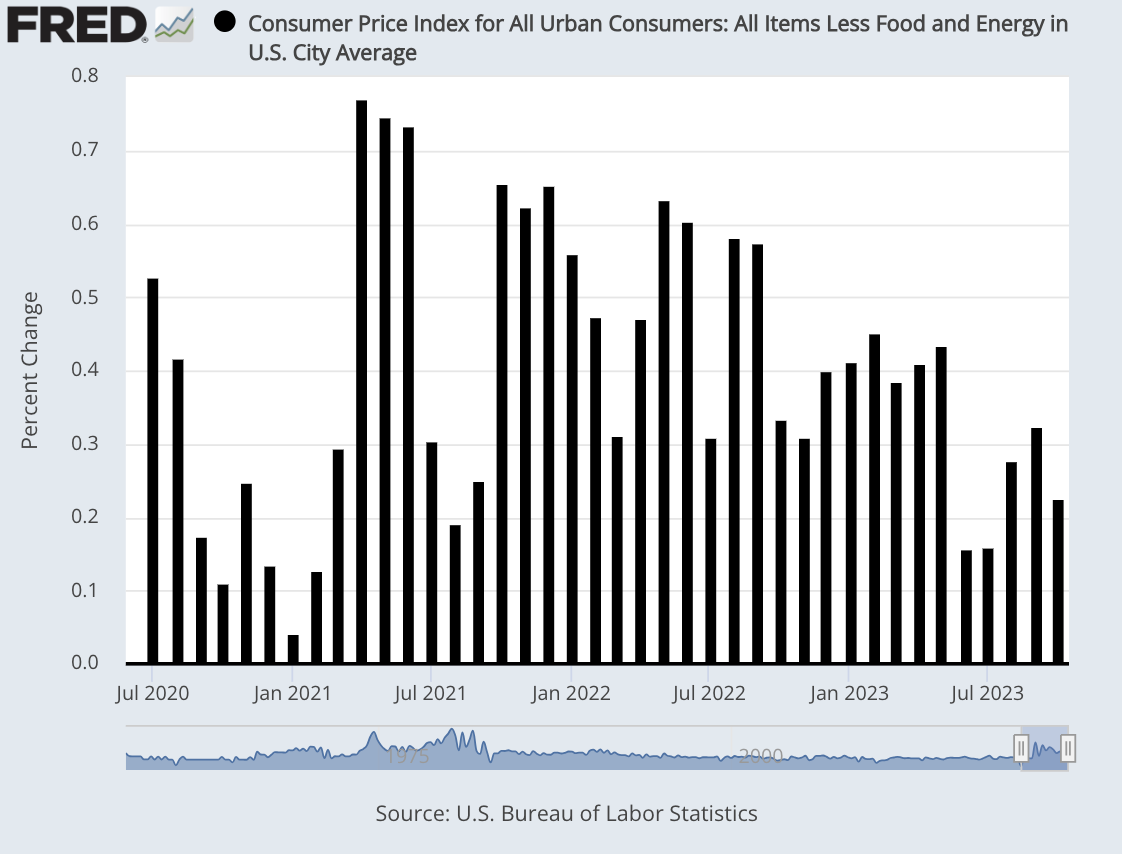

The inflation story isn’t just about energy prices. The core rate, which excludes food and energy, rose by only 0.2% last month. That was also 0.1% below expectations. Over the last year, core inflation is up by 4%. That’s the slowest 12-month rate in over two years.

Here’s a look at the monthly seasonally-adjusted core rate. My apologies for the econ jargon, but this way, you can really see how the threat of inflation has faded over the last year:

Here are some details:

The flat reading on headline CPI came as energy prices declined 2.5% for the month, offsetting a 0.3% increase in the food index. It was the slowest monthly pace since July 2022.

Shelter costs, a key component in the index, rose 0.3% in October, half the gain in September as the year-over-year increase eased to 6.7%. Within the category, owners equivalent rent, which gauges what property owners could command for rent, increased 0.4%. A subcategory that includes hotel and motel pricing dropped 2.9%. 0.4% for September.

(…)

Vehicle costs, which had been a key inflation component during the spike in 2021-22, fell on the month. New vehicle prices declined 0.1%, while used vehicle prices were off 0.8% and were down 7.1% from a year ago.

Airfares, another closely watched component, declined 0.9% and are off 13.2% annually. Motor vehicle insurance, however, saw a 1.9% increase and was up 19.2% from a year ago.

Wall Street celebrated as it now looks like the Federal Reserve won’t be raising rates anymore this cycle.

In Wall Street’s mind, there’s nothing better than lower interest rates. On Tuesday, the S&P 500 rallied for the tenth time in the last 12 sessions. For the day, the index gained 1.9%. The S&P 500 is already up 7.2% in November and the month isn’t quite halfway over.

Futures traders think there’s only a 0.2% chance the Fed will hike next month. One month ago, the odds for a December rate hike were at 30%. Traders think there’s a 0.2% chance it will hike in January. By May, the market says there’s a 65% chance that the Fed will start cutting rates.

On our Buy List, Trex (TREX) was up more than 7.5% today. The deck-maker recently beat earnings and raised guidance. Celanese (CE) rallied 6.7% on Tuesday, and Polaris (PII) was up close to 6%.

Tuesday’s market was heavily concentrated on higher-risk areas of the market. On days like today, I like to look at the spread between the S&P 500 Low Volatility Index and the S&P 500 High Beta Index. On Tuesday, High Beta gained 4.45% while Low Vol gained 1.24%.

What’s going on? I think a lot of investors mistakenly believe that the promise of lower rates will lead us back to the glory days of 2020-2021. That’s when rates were at 0% and the government was spending money to boost the economy. The Fed effectively took risk out of the investing equation and high-risk areas soared.

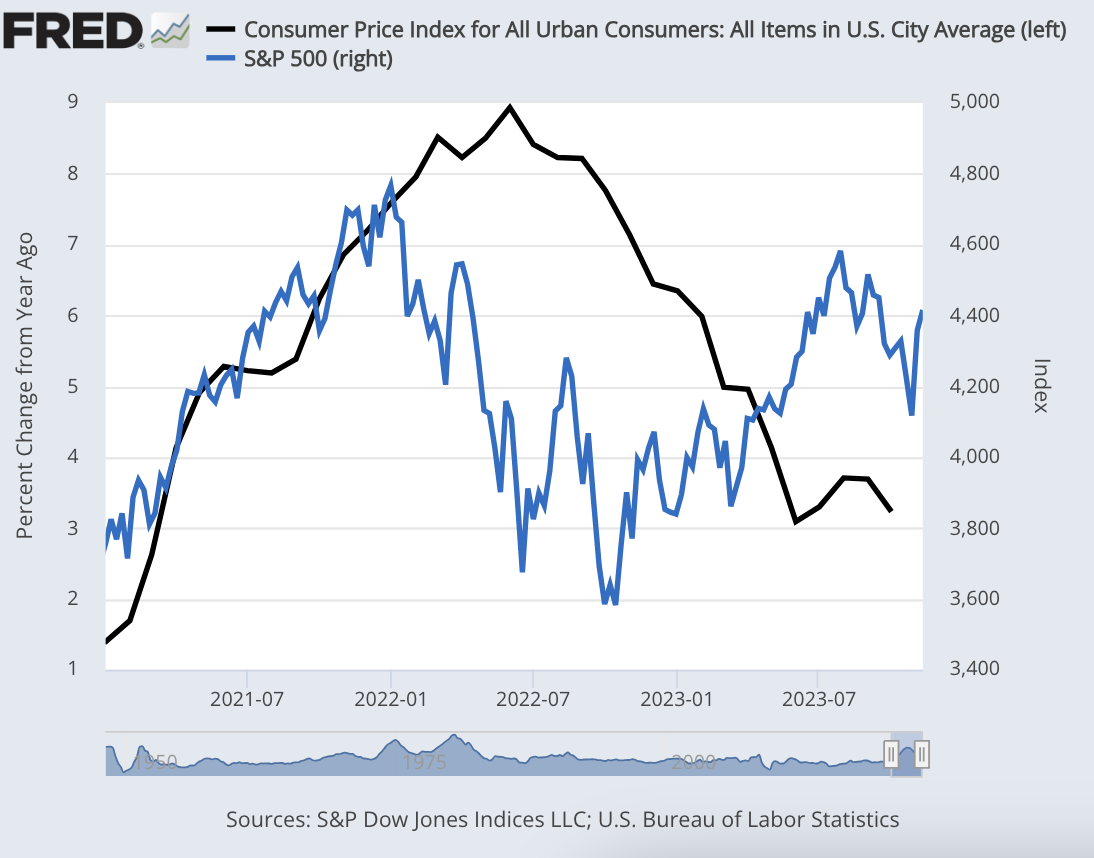

As I look at the stock market and inflation numbers, I can’t help wondering how overly complicated the game appears. Perhaps it’s as easy as leaving the market when inflation hits 7% and then coming back in when it drops below 7%. That’s an easy rule that’s pretty much worked perfectly. You can see it in this chart. The black line is the rate of inflation and it follows the left scale. The S&P 500 is the blue line and it follows the right scale.

The earnings numbers for Q3 are almost all in. It looks like the S&P 500 will report earnings growth of 4.1%. What about for Q4, which is already halfway done? Analysts are expecting Q4 earnings growth of just 3.2%.

But after that, things are expected to improve. Analysts expect earnings growth to improve to 6.7% for Q1, and 10.5% for Q2. FactSet notes that while these projects are down since September, they’re still above the results for Q3. In other words, not only is Corporate America still profitable, but earnings growth is accelerating.

The fastest-growing sectors are projected to be Communication Services (19.9%), Consumer Discretionary (16.5%) and Information Technology (15.2%). The stocks that are expected to contribute the most to earnings growth for Q1 are Nvidia, Amazon, Meta Platforms and Alphabet. Without these four, the S&P 500 would have earnings growth of 3.2%. With them, it’s 6.7%.

Stock Focus: Simulations Plus (SLP)

I’ve been a fan of Simulations Plus (SLP) for some time now. It’s a neat company that’s not well known. SLP’s market cap is just over $725 million and only three analysts follow it. The stock rallied 5.2% today. Incidentally, today was also SLP’s Investor Day.

Simulations Plus makes software that lets drug companies simulate tests of their products in the virtual world before using any human or animal test subjects. That’s a major cost-saver for drug companies.

Simulations Plus helps streamline the R&D process by making it faster and more efficient. Not only is this cost effective, but it also helps drug companies in dealing with time-consuming regulatory hurdles.

In fact, there are times when the results from SLP’s products have allowed companies to waive clinical studies. The cost savings are substantial. This means drug companies don’t have to deal with the time and expense of recruiting test subjects and analyzing test results.

By using SLP’s software, drug companies can experiment with many variables like fine-tuning dosage amounts. Companies can also see potential harmful side effects. Another important factor is that companies can identify treatments that have no benefits.

In healthcare, cost control is a major issue. That’s why SLP’s products are in heavy demand. A great business to buy is one that helps other companies control their costs.

In many ways, I think what Simulations Plus does for pharmaceutical researchers is closely akin to what Ansys (ANSS) does for engineers. By sitting at a computer, an employee can efficiently iron out a lot of kinks before experimenting in the real world. Simulations Plus is also branching out from their core customer base of drug companies. They work with consumer products companies to see the side effects of things like pesticides.

Unfortunately, the shares have not performed well over the past few years. That could make it a compelling buy.

Simulations Plus recently reported its fiscal-Q4 earnings. For the quarter, SLP’s revenues increased 33% to $15.6 million. The company’s gross profit grew 35% to $12.3 million.

For the quarter, the company earned 18 cents per share. That matched Wall Street’s consensus although I don’t know if three analysts count as a consensus. The stock dropped 15% after the report.

For all of last year, SLP’s revenue grew 11% to $59.6 million, and earnings increased from 60 cents to 67 cents per share.

For the new fiscal year, SLP sees revenues ranging between $66 million and $69 million. That works out to a growth rate of 10% to 15%. For earnings, SLP sees profits ranging between 66 cents and 68 cents per share. I’m particularly impressed that SLP can maintain gross margins that are nearly 80%. Simulations Plus pays out a small quarterly dividend of six cents per share.

As much as I like this business, valuation is still a concern. Going by SLP’s latest guidance, the shares are going for 50 times forward earnings. That a lot for any stock.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want more info on our ETF, you can check out the ETF’s website.

Posted by Eddy Elfenbein on November 14th, 2023 at 6:38 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His