CWS Market Review – November 28, 2023

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

RIP: Charlie Munger

As I was preparing today’s newsletter, I got the news that Charlie Munger, Warren Buffett’s long-time partner, had died just a few weeks before his 100th birthday.

I don’t have enough time to offer a tribute, but I wanted to share with you some of my favorite Mungerisms:

“Someone will always be getting richer faster than you. This is not a tragedy.”

“People calculate too much and think too little.”

“99% of the troubles that threaten our civilization come from too optimistic accounting.”

“Knowing what you don’t know is more useful than being brilliant.”

“Investing is where you find a few great companies and then sit on your ass.”

“A lot of people with high IQs are terrible investors because they’ve got terrible temperaments.”

“It’s waiting that helps you as an investor, and a lot of people just can’t stand to wait.”

“Necessity never made a good bargain.”

“It is remarkable how much long-term advantage people like us have gotten by trying to be consistently not stupid, instead of trying to be very intelligent.”

Rest in peace, Charlie.

A Great Month for Stocks

This has been a very good month for stocks. Unless something major happens later this week, November will go down as one of the best months for the S&P 500 in years.

I’m also pleased to see that our Buy List has outpaced the market on the way up. So far this month, the S&P 500 has gained 8.6% while the Buy List is up 10.6%.

The reason for the rally is quite simple. Investors have been convinced that the Fed is done, or just about done, with its rate hikes. One of the oddities we’re seeing is that there’s a pronounced gap between the Fed’s tough-sounding rhetoric and the market’s expectations. Even today, Fed Governor Michelle Bowman said that more rate hikes are needed. I’m not so sure she’ll get her way.

The market loves lower interest rates and that appears to be what it will get. The Fed meets again in two weeks and it’s highly unlikely that the FOMC will hike rates. Futures traders see about a one-in-three chance of a rate cut by March.

I’ll give you an example of how much the market loves low interest rates. I ran a test. I took all the data for the S&P 500 and the three-month Treasury yield over the last 18 months.

I then separated the data into three buckets: days when the three-month Treasury yield fell, days when it increased and days when it stayed flat. Then I looked at how the S&P 500 performed on those days.

On days when the three-month yield increased, the S&P 500 fell at an annualized rate of 7.63%. When the yield was unchanged, so were stocks. The S&P 500 rose at an annualized rate of 0.06%. But when the three-month yield fell, the S&P 500 rose at an annualized rate of 41.4%. Falling rates are the fuel of a stock rally.

The good news is that inflation has abated in recent months, but the Fed wants to be clear that it won’t stop hiking until inflation gets back to its target of 2%. This could be a mistake.

I think it’s more important that the trend of inflation heads lower rather than hitting some arbitrary target. Bear in mind that the price for gasoline has fallen for 60 days in a row. At some point, the Fed will have to give in and admit victory.

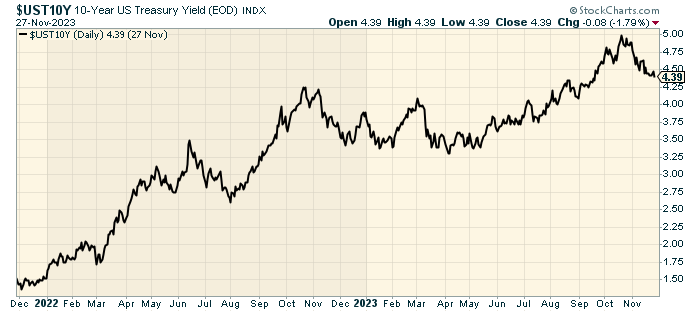

Lately, we’ve also seen a rally in long-term bonds. I’m somewhat hesitant to highlight a drop in long-term yields because it comes after a dramatic rise in yields. The yield on the 10-year Treasury rose from 3.3% in April to 5% in September. It’s back down to about 4.3%.

There are emerging signs that the economy is on shaky ground. The consumer was spending money feverishly this summer, but that’s faded away.

Worst Year for Home Sales in 30 Years

The housing market, in particular, is quite weak. Existing-home sales in the U.S. are on pace for their worst year in three decades. This is the impact of higher mortgage rates. On Monday, the government said that new-home sales fell 5.6% in October.

That was below expectations. Wall Street had been expecting an annualized rate of 723,000 new homes sold. Instead, it was just 679,000.

What’s happening is that so many people locked into mortgages at very low rates. That means that now they’re reluctant to take on new higher-yielding mortgages.

The Fed has thrown a deadly right hook at inflation, and it hit the housing market square in the face. Mortgage rates peaked in October and have started to come down along with Treasury yields.

Tomorrow, the government will revise its report on Q3 GDP growth. The initial report said that the U.S. economy grew in real annualized terms of 4.9% during the third quarter. That was the best quarter for economic growth since Q4 of 2021. Consumer spending greatly helped the economy during Q3.

Wall Street is starting to turn its attention to Q4. The Atlanta Fed’s GDPNow model says that the economy will grow at a 2.1% rate in Q4.

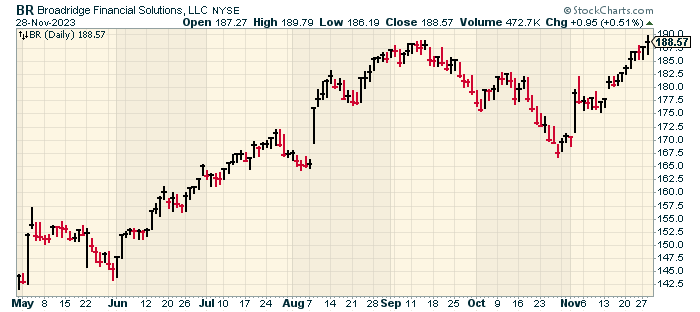

Broadridge Financial Hits New High

As I mentioned before, our Buy List has been acting well lately. I wanted to share with you one of our better-performing stocks which has been Broadridge Financial Solutions (BR).

This is actually a follow-up because I mentioned Broadridge in August 2022 in our free newsletter. At the time, the company had just reported very good results and it had been highlighted in Barron’s. This is part of what the magazine had to say:

Broadridge has been a steady stock for rocky times. That is thanks to a model heavy on recurring-revenue businesses and exposure to long-term trends that should remain in place no matter the near-term path of the economy or interest rates. Broadridge stock’s recent rally could cap gains in the near term, but the company’s long-term positive trajectory remains intact.

The company has a near monopoly in the business of managing and distributing investor communications for practically every public company in the U.S., plus mutual funds, exchange-traded funds, and more. That includes proxies, regulatory disclosures, and other reports and filings required of all U.S. securities issuers. Those are non-discretionary communications that companies and funds need to distribute no matter what the world is doing. That segment tends to grow at the pace of overall stockholdings in the U.S., with Broadridge able to eke out higher profit margins thanks to a continuing shift from printed documents delivered by mail to digital investor communications.

Broadridge also has a smaller but faster-growing segment focused on back-office functions for asset managers, investment banks and broker-dealers. Those include trade processing and settlement, record-keeping, and a variety of other compliance or regulatory functions. That is a software-as-a-service business that has expanded through a combination of organic growth and Broadridge buying companies with adjacent or complementary software and services.

The only thing better than a monopoly is a near-monopoly. It gets less attention from the authorities. The important point that Barron’s covers is Broadridge’s recurring revenue. That’s a great quality for a business to have.

I like looking at BR’s stock chart because you can tell when its earnings report comes out:

Earlier this month, Broadridge reported another strong quarter. For its fiscal Q1, BR earned $1.09 per share. That’s up 30% from a year ago, and it was 12 cents higher than expectations. Total revenues increased 12% to $1.431 billion, and recurring-revenue growth was up by 8%. Last quarter, BR bought back $150 million of its shares.

I’m glad to see that Broadridge is standing by its previous guidance. That calls for recurring-revenue growth of 6% to 9%, and EPS growth of 8% to 12%. The latter works out to a range of $7.57 to $7.85 per share. BR should have little trouble reaching that.

In August, Broadridge raised its annual dividend by 10% to $3.20 per share. The company has now raised its dividend in all 12 years since it went public, and 11 of those increases were by double digits.

The stock hit another 52-week high on Tuesday. We now have a 40.6% gain in Broadridge this year. Broadridge is a good example of a business that’s not well-known but has a strong, durable moat.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want more info on our ETF, you can check out the ETF’s website.

Posted by Eddy Elfenbein on November 28th, 2023 at 6:22 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His