CWS Market Review – December 19, 2023

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

Before I begin, a quick reminder: I’m going to unveil the 2024 Buy List next week.

I’ll send you the next free issue of CWS Market Review on Monday, which is Christmas Day. The stock market will be closed that day. This will be our 19th annual Buy List.

Normally, our Buy List has 25 stocks and each year: five new stocks go in, and five old ones come out. This year, we got an extra stock when Danaher spun off Veralto. That means six stocks will go out and five new ones will come in.

I’ll have all the details for you soon, but it appears that our Buy List has returned over 500% in its entire history. Here’s to the next 19 years!

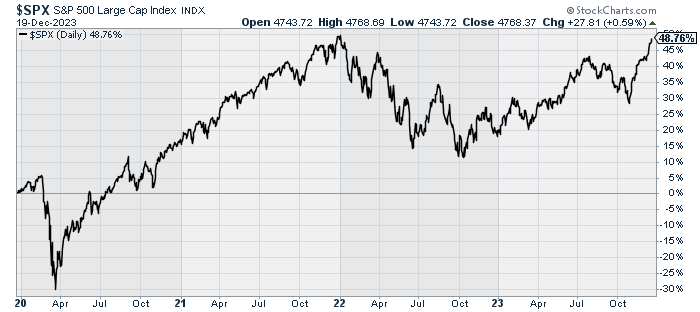

The S&P 500 Hits a 23-Month High

Now let’s look at the stock market which has certainly been in the holiday spirit lately. On Tuesday, the S&P 500 closed at its highest level in nearly two years. The index is getting very close to its all-time high (less than 0.6% away).

Historically, there really has been a Santa Claus Rally. I broke down the entire history of the Dow back to its beginning in 1896. I found that from December 21 to January 8, the Dow has gained an average of 2.83%. That means that more than one-third of the Dow’s historic gain has come over a period of less than three weeks.

Roughly one-third of the stock market’s gain over the last four years has come in the last seven weeks. The stock market tends to act like a rabbit: it can sit still for long stretches before it suddenly hops away. That’s one of the reasons why I avoid trying to time the market.

The Federal Reserve meets again in six weeks, and I doubt they’ll make any changes to interest rates. But the meeting after that, the one on March 20, could be a very important meeting.

Wall Street has completely changed its mind on what could happen. One month ago, traders thought there was a 28% chance of the Fed cutting rates at the March meeting. Today, those odds are up to 75%.

What’s the cause for the change in outlook? Two things. The jobs reports have gotten noticeably weaker. Nothing alarming, but noticeable. The other is that the inflation reports have been relatively benign. We’re not out of the inflation woods just yet, but we have to note that there has been improvement.

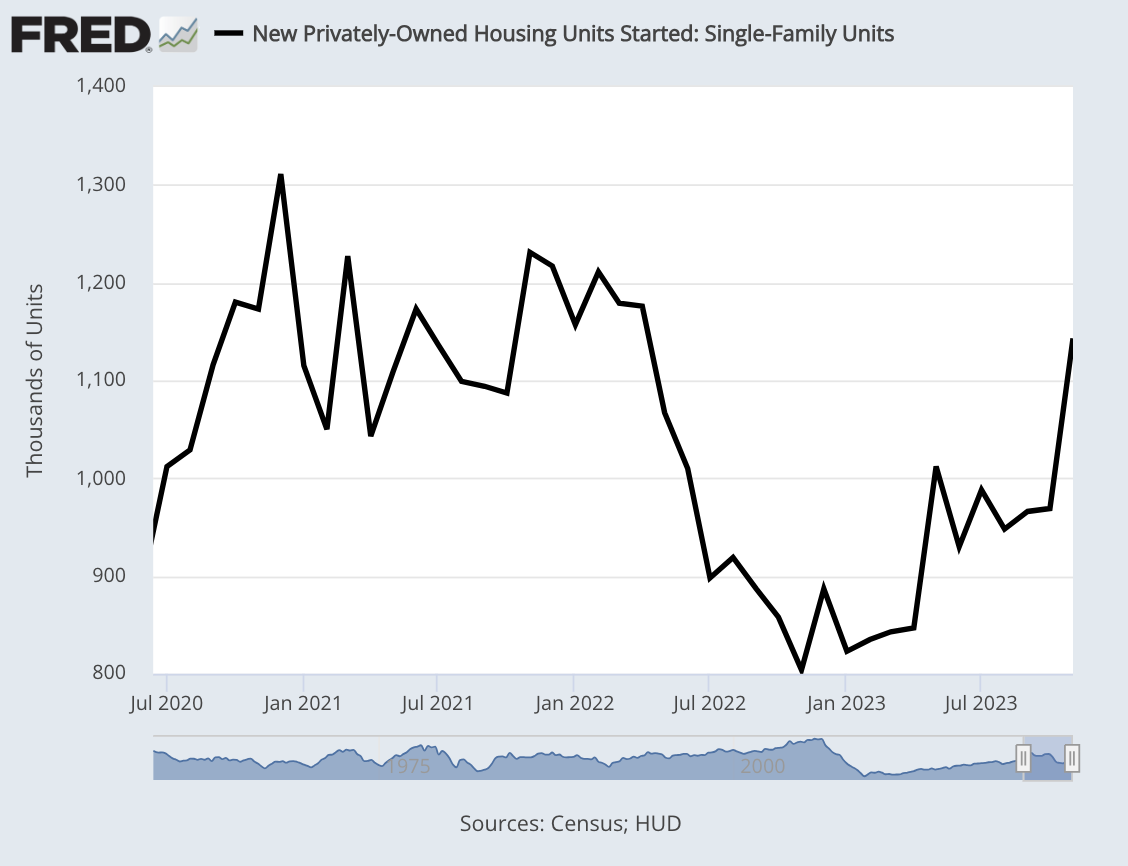

Lower interest rates, or even the prospect of lower rates, can have a big impact on the economy. Notice, of course, the markets’ nice bounce since late October. Not only that, but interest rates also have a major impact on the housing market.

Housing Is On the Rebound

During the middle of each month, several of the important reports on housing are released. Many stock investors tend to overlook these reports, but that’s a mistake. The housing sector is vital to the economy. In fact, several years ago, Edward Leamer, a well-respected economist, went as far as to say that “Housing IS the Business Cycle.” I think he’s right.

On Monday, the National Association for Home Builders said that homebuilder confidence rebounded slightly in December. The confidence number rose from 34 to 37 while Wall Street had been expecting 36. That’s not a terribly large jump, but it’s good to see something positive as mortgage rates have started to move lower recently.

I don’t want to declare victory too soon, but it looks like interest rates have peaked for this cycle. Even the Fed sees rates being significantly lower by this time next year.

On Tuesday, we got a nice surprise from the housing starts report. Last month, single-family housing starts rose to a 19-month high. The report also said that the figure for permits for new construction rose to its highest level since May 2022. This was much better than Wall Street had been expecting.

The problem right now for housing is that there aren’t enough homes, and that’s caused prices to spike. Builders need to catch up to demand.

Activity was also likely supported by mild temperatures and dry conditions. Data for October was revised slightly lower to show single-family starts rising to a rate of 969,000 units instead of the previously reported 970,000 units.

Starts vaulted 42.2% on a year-on-year basis in November.

Single-family homebuilding soared in the Northeast, Midwest and the densely populated South. It declined in the West.The rate on the popular 30-year fixed mortgage averaged 6.95% last week, the lowest level since August, from 7.03% in the prior week, according to data from mortgage finance agency Freddie Mac. It has tumbled from a 23-year high of 7.79% in late October, tracking the decline in U.S. Treasury yields.

The stock market turned right as mortgage rates peaked. I can’t say I’m surprised.

There are currently about one million homes on the market. Just before Covid hit, there were two million homes on the market. The housing reports helped Goldman Sachs raised its estimate for Q4 economic growth by 0.2% to 1.7%. The Atlanta Fed sees Q4 growth coming in at 2.7%.

I’m going to watch housing closely. The report on existing home sales is out tomorrow, and on Friday we’ll get the report for new home sales.

Q4 Earnings Season Will Start Soon

We’re getting close to Q4 earnings season, and I’ll caution that it probably won’t be a very strong one for the market as a whole. That’s more a reflection of how things have been rather than how they will be.

For Q3, the S&P 500 had earnings growth of 4.9%, and analysts expect growth to slow down to 2.4% for Q4. Analysts expect quarterly revenue growth of 3.1%. For the year, the S&P 500 is expected to post earnings growth of just 0.6% and revenue growth of 2.3%.

FactSet (which is not only a Buy List stock, but a great resource for stats on the market) said that the broadline retail industry is expected to report earnings of $30 billion this year. That’s up from a loss of -$1.2 billion last year.

The earnings figure for the consumer discretionary sector is expected to rise by 43.9%, but there’s a major caveat. If we exclude Amazon, then earnings growth for consumer discretionary would fall to just 16.2%.

Overall, businesses are healthy even though this has been a subdued period for growth. For 2023, the estimated net profit margin is expected to be 11.6%. That’s down slightly from 11.8% for 2022, but it’s still above average for the last ten years.

If interest rates come down in 2024, that will spur a housing rebound and that will be good for consumers and businesses. This is why stocks have been in such a good mood.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want more info on our ETF, you can check out the ETF’s website.

Posted by Eddy Elfenbein on December 19th, 2023 at 7:22 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His