CWS Market Review – February 20, 2024

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

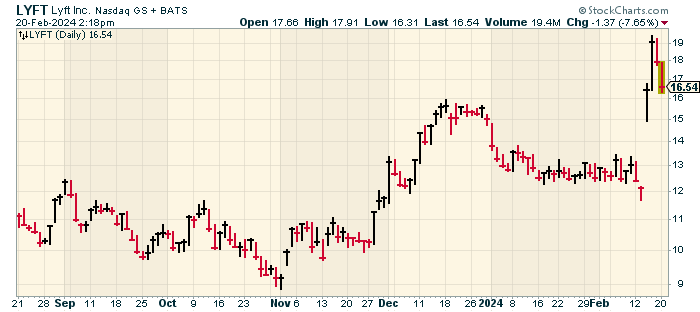

Lyft Soars 67% on Typo

After the close of trading last Tuesday, the ride-sharing company, Lyft (LYFT), released its quarterly earnings report. In it, the company said that it expects its profit margin to improve by 500 basis points.

Wow! In after-hours trading, the stock soared as much as 67%.

There was, however, one teeny-tiny problem: they meant to say 50 basis points, not 500.

A spokesperson for the company attributed the correction to a clerical error.

Oh!

Cue Emily Litella, “nevermind.”

The shares quickly fell back to Earth. This is a good reminder that the market is made up of people, and it’s subject to all the faults and foibles people have.

We have lots of fancy models that try to explain a process that can be highly irrational, or simply misinformed.

This is also a good reason why I’m leery of stop orders, especially for long-term investors. You can easily be stopped out of a good stock for a bad reason.

By the way, Lyft really did have a great quarter, and the stock is up, but much of the good news has been lost due to an embarrassing typo. It’s amazing how one wrong key stroke can duck things up.

Could the Fed Resume Hiking Rates?

In recent issues, I’ve talked about the market’s change of heart regarding what the Fed will do with interest rates. Not that long ago, the market thought the Fed would be cutting interest rates by now. Lately, it looks like the Fed won’t be cutting rates at its meetings in March or May. In fact, the June meeting may soon look doubtful.

What’s going on? Into all this jumps former Treasury Secretary Lawrence Summers who said the Fed may even raise interest rates. Specifically, Summers said, “There’s a meaningful chance—maybe it’s 15%—that the next move is going to be upwards in rates, not downwards.”

I’m not fully in Summers’s court just yet, but it’s an interesting take. Summers said that Wall Street economists had been expecting that plunging housing costs would hold back overall inflation, but that hasn’t happened.

Economists like to look at the “core rate” of inflation which excludes food and energy prices. There’s also the “super core rate” which is the cost of services except energy and housing. The super core rate has been getting a lot of attention lately.

This is important because it makes us focus on the issue of how much inflation is driven by wages, which is another way of asking, how much of inflation does the Fed control?

What happened is that during Covid, employees finally held the upper hand. It was a tight labor market and wages started to improve. Those increases were largely passed along in the form of higher prices for services, and not so much for goods.

I’m borrowing this example from the WSJ but it explains the phenomenon well. Let’s compare haircuts and televisions. The former is a service that’s driven by wages. The latter is a good and less dependent on wages.

The prices for haircuts are rising while TV prices are falling. It’s like two separate economies but it’s really showing us how much prices are influenced by wages. The January CPI report showed that super core prices rose by 0.85%. Summers is making the point that the prices that most concern the Fed are far from under control.

Walmart Beats the Street

Last week’s retail sales report came in below expectations. This morning, we got another retail sales report but this time, it wasn’t from the government, Instead, Walmart (WMT) released its earnings report.

The company is so big that its earnings report is effectively a report on Americans’ spending behavior. Walmart said that its quarterly revenue increased by 6% to $173.39 billion. That works out to about $1.3 million every minute.

Today’s report was for the key holiday spending months of November, December and January. For the quarter, Walmart earned $1.80 per share which was 15 cents higher than Wall Street’s consensus. The shares jumped a little over 3% in today’s trading.

Walmart had held up well during the recent (and perhaps, still ongoing) bout of inflation. As any shopper knows, Walmart is relentless in its quest to keep prices as low as possible. Last quarter, Walmart was helped by soaring e-commerce revenue. Global e-commerce sales rose 23%.

Going forward, Walmart said it expects sales growth of 4% to 5% for its fiscal Q1 (ending April 30), and earnings of $1.48 to $1.56 per share. For the year, Walmart expects earnings of $6.70 to $7.12 per share. That means the stock is going for about 25-26 times earnings. In my opinion, that’s too high.

While other companies have been holding back, Walmart has been expanding and upgrading its locations. The company said that it will raise the average income for store managers to $128,000 per year.

Shares of Walmart will split 3-for-1 after the market closes on Friday. This will be the retailer’s first stock split in 25 years. In the 25 years prior to that, Walmart split its stock nine times, all of them were 2-for-1.

According to the largest retailer on the planet, shoppers are plenty active.

Capital One Buys Discover for $35 Billion

“What’s in your wallet?” Apparently, Discover Financial Services.

A major acquisition was announced today in the credit card space. Capital One Financial (COF) said it’s buying Discover Financial Services (DFS) for $35 billion. The deal is all cash.

Here’s how the deal works. Discover shareholders will get 1.0192 shares of COF for each DFS share they own. That’s a nice 26% premium for Discover based on Friday’s close.

Once the deal is done, Capital One shareholders will own 60% of the company, while Discover shareholders will own the other 40%. The companies expect the deal to close later this year or early in 2025.

There’s still the issue of getting regulatory approval. The government doesn’t look too kindly on mergers of industry leaders, especially in industries that aren’t wildly popular with consumers.

When deals like this are announced, the market likes to poke around at what might be next. This time, I’m skeptical because there doesn’t appear to be an obvious candidate. Also, I suspect that getting the Feds to sign off on this deal may be harder than they think.

The big earnings report for tomorrow will come after the close when Nvidia (NVDA) reports its earnings. Nvidia has become the most prominent AI trade. The company recently surpassed Alphabet (GOOG) and Amazon (AMZN) in total market value.

I guess you can say that expectations are high as the shares have soared 450% over the last 16 months. Also, Nvidia has crushed its last three earnings reports. The company has exceeded expectations by (in order) 18%, 29% and 19%. Nvidia has really become the marquee name of the Magnificent 7 gang.

For tomorrow, Wall Street expects earnings of $4.63 per share. Between you and me, I think that really means at least $5 per share. Wall Street is expecting Nvidia’s sales to rise by 240%. Of course, a large amount of those sales are going to Microsoft, Google and Amazon. Last quarter, Nvidia’s gross margin was 75%.

This is a good case of expectations being so high that almost any number will be a disappointment. Nvidia closed down today by 4.3%.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want more info on our ETF, you can check out the ETF’s website.

Posted by Eddy Elfenbein on February 20th, 2024 at 6:10 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- August 2026

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His