CWS Market Review – March 19, 2024

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

Why You’re Not Diversified When You Think You Are

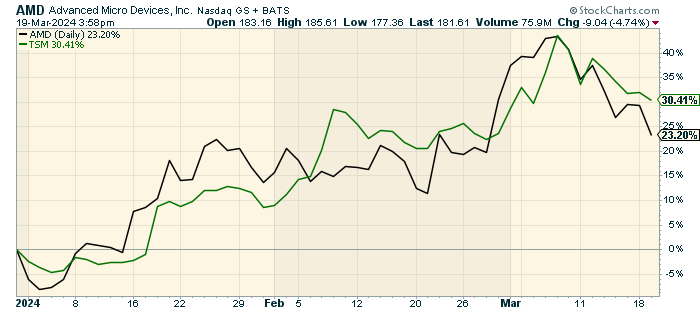

One of the themes I stress to investors, especially newer investors, is the importance of owning a diversified portfolio. So often, I’ll hear investors say, “sure I’m diversified! I own AMD and TSM.” Well, that’s not exactly proper diversification. Owning two stocks that closely mimic each other does little to lower your risk.

Diversification is an important topic and it’s more difficult than it may appear. By not being properly diversified, investors can leave themselves exposed to risks they’re unaware of.

For example, an investor may load up on several stocks that are highly sensitive to the U.S. dollar. When adding those stocks, they may have had no idea that that was the case. Then, after a few days of trading, they see how their portfolio can be impacted by, say, the decisions of a foreign central bank. They had no idea that’s what they were getting themselves into.

I’ve also seen many investors become overly exposed to technology stocks. This leaves them open to the twists and turns of the capital investment cycle of some large companies they don’t own.

I even fell prey to this effect last year when I had both Danaher and Thermo Fisher Scientific on our Buy List. I like both stocks, and it’s no wonder because the companies are similar. Not surprisingly, both stocks tend to behave very similarly, especially in the short term. I should have realized this beforehand.

An investor can own Lowe’s and Home Depot. There’s certainly no law against it, but understand the position and risks you’re taking. To quote Winston Churchill, “Money is like manure, it’s only good if you spread it around.”

Oftentimes, you’ll see an investor who had a particularly strong year but on closer inspection, they were merely overly exposed to a particular risk that paid off. Was the investor brilliant or did some category like small-cap growth have a banner year? Humphrey B. Neill said, “Don’t confuse brains with a bull market.”

Our Buy List is a good example of the portfolio that’s well diversified. You don’t need to own every stock, but a healthy sample can start you on your way to owning a high-quality portfolio that’s properly diversified.

The Worst Environment for Defensive Stocks in Decades

I highlight this point because right now, we’re seeing this effect play out. In particular, I’m referring to the lagging performance of many defensive stocks. Sectors like Consumer Staples and Utilities are at their worst relative performance levels in decades.

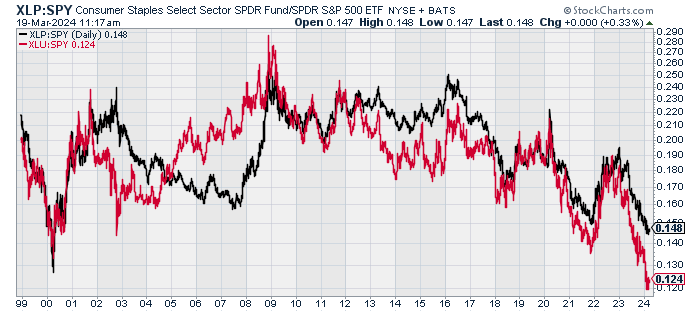

Check out this chart below:

The chart shows the S&P 500 Consumer Staples divided by the S&P 500 (in black) and the S&P 500 Utilities divided by the S&P 500 (in red). If those lines are rising, then they’re beating the market, but if they’re falling then they’re lagging the market.

Right now, the lines are as low as they’ve been in at least 25 years. These lines are important to watch because it reflects how popular defensive stocks are, and right now, they’re very unpopular.

What’s going on? Defensive stocks, as the name implies, generally move opposite to the overall economy. When the economy gets weak, investors want to own safe and secure defensive stocks. But when the economy is strong, or is perceived to be strong, then investors shy away from defensive stocks in search of cyclical stocks.

It’s not that one group is in any sense better than another. Rather, time and chance happens to them all. You’ll notice that both lines got a little bump four years ago at the start of Covid. Again, I need to stress that this is relative performance. Both sectors were falling severely, just not as severely as everyone else was.

Defensive stocks tend to do well when interest rates are falling, which also tends to align with a weak economy. Defensive stocks did indeed trail the market as the Federal Reserve hiked interest rates.

Lately, there appears to be a disconnect between defensive stocks and the state of the economy. The economy certainly has its strong points, but I’m still surprised by how poorly defensive stocks have been behaving. I always pay attention when good stocks have underperformed for some time. I wouldn’t be surprised to see the cyclical/defensive cycle soon turn.

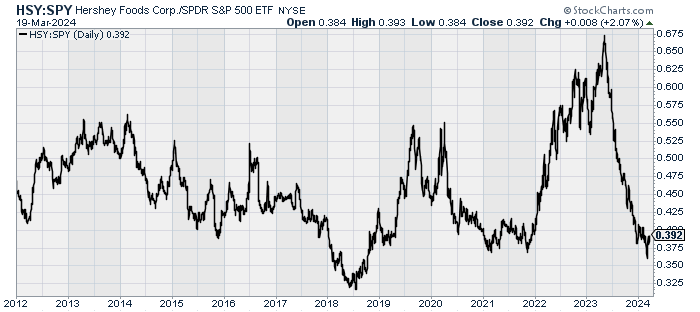

On our Buy List, Hershey (HSY) is a good example of a defensive stock that’s been hurting. See the chart below which shows the relative performance of Hershey, meaning HSY divided by the S&P 500.

That’s quite a run-up followed by a rundown. During an economic downturn, folks don’t cut back on their purchases of Hershey Kisses. Over the last ten months, shares of Hershey are down by more than 20% while the S&P 500 is up by more than 20%. Yet, Hershey’s earnings reports have been quite good.

Certainly, some of the damage has been caused by the soaring price for cocoa. Thanks to heavy rains in west Africa, the price for cocoa has jumped 150% in the past year. In response, Hershey has been able to pass on some of those price increases.

Right now, Wall Street expects that Hershey will have flat earnings growth this year. That may be right, but I highly doubt that flat earnings growth will last long. At some point, cocoa production will return to normal, and Hershey will prosper.

I certainly understand the danger in being too defensive, but I think all Street is currently overdoing its aversion to defensive stocks. The cycle will turn.

Tennant: The Floor Cleaner that Beats the Market

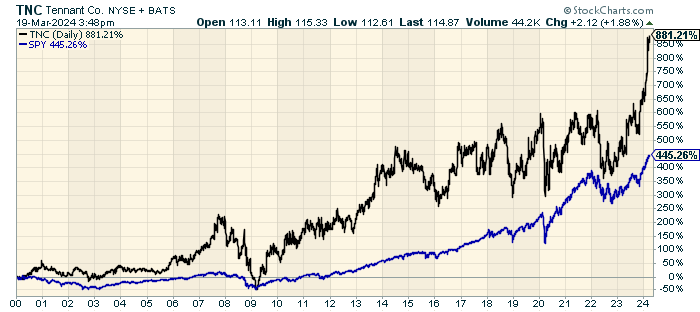

I enjoy highlighting superior stocks that may not be well-known. This week, I wanted to bring Tennant Company (TNC) to your attention. The company “designs, manufactures, and markets floor cleaning equipment.”

Tennant has a market cap of just over $2 billion, and only three Wall Street analysts follow the stock.

A few weeks ago, Tennant reported Q4 earnings of $1.92 per share. That easily beat Wall Street’s consensus (such as it is) of $1.25 per share. In three sessions, the stock gained almost 13%.

Tennant has an enviable track record. Since 2000, TNC has outpaced the S&P 500 by a margin of 881% to 445%.

Tennant has increased its dividend for the last 52 years in a row. I’ll never understand why stocks like this are so overlooked.

What to Expect from This Week’s Fed Meeting

The Federal Reserve is meeting today and tomorrow. The FOMC will release its policy statement tomorrow at 2 pm ET. Don’t expect any change to interest rates. The futures market currently places odds of 99% that the Fed will leave rates unchanged. That sounds about right, maybe a little low.

Along with tomorrow’s policy statement, the Fed will also update its economic projections. I’ll caution you that the Fed has a very poor track record of trying to forecast what the economy will do. Still, it’s important to see what they’re thinking.

There won’t be any Fed meeting in April, but the central bank will get together again in early May. Once again, don’t expect much action. Futures traders say there’s a 93% chance that the Fed won’t make any changes to interest rates.

The earliest traders see the Fed cutting rates is at the June meeting. According to the latest prices, traders place a 60% chance of a rate cut then. That’s still far from certain. We’ll learn more in tomorrow’s Fed statement.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want more info on our ETF, you can check out the ETF’s website.

Posted by Eddy Elfenbein on March 19th, 2024 at 8:57 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His