CWS Market Review – March 5, 2024

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

Beware the Reversals of March

In recent years, March has been the time for dramatic market turnarounds. Sometimes, March has welcomed major high points while other times, it’s been lows; but whatever the direction, this has been the time of year for them.

Why March? Beats me. Perhaps the coming of spring gives new hope to those who’ve been on the wrong end of the market for so long.

I’ll give you a few examples. Probably the biggest was the Great Tech Bubble which peaked in March 2000. The Nasdaq Composite closed at 5,048 on March 10, 2000.

This was the top of a blistering rally. In the previous 18 months, the index had soared 250%. The good times didn’t last. One year later, the Nasdaq was down 60%. Within two-and-a-half years, the Nasdaq was off by more than 75%. Anyone heard from Pets-dot-com lately?

The bear market low of 2002-03 is up for some debate. That’s because the market low officially came in October 2002. However, the stock market put on a nice 19% rally over the next four weeks…before it collapsed again.

Some analysts will claim that a rally of that size qualifies as a new bull market. Frankly, I’m agnostic on these points, but the S&P 500 reached another major low on March 11, 2003, right at the start of the Iraq War. The market low came exactly three years and one day after the Tech Bubble popped.

The Financial Crisis of 2007-08 is an interesting case because it took some time before the size of the damage was fully realized. The stock market peaked in October 2007 before it gradually eroded, and that erosion soon turned into an avalanche.

The closing low for the S&P 500 came on March 10, 2009 at 676.53. In terms of pure valuation, that may stand out as a multi-decade low. Adjusted for inflation, the Dow Jones Industrial Average was where it was 43 years before. Everyone, it seemed, hated Wall Street. If you recall, this was the time Jim Cramer went on Jon Stewart’s show. Like the others, this was also a great time to buy.

Then there’s the Covid bear market. That was an extremely dramatic market and again, March was the turning point. I’ve never seen a market so panicked. In March 2020, the S&P 500 had two of its six worst days in history, and it had two of its ten best days in history. In 13 trading days, the S&P 500 lost close to 30%. The S&P 500 finally reached its closing low of 2,237.40 on March 23, 2020.

Of course, that was also a great time to buy (thanks to extraordinary efforts from the Federal Reserve). In less than 17 months, the S&P 500 doubled, and it’s up another 14% from there.

It’s interesting to see how the market emerges from whatever chaos we face. On Wall Street, we refer to market drops as being “corrections” but from a long-term perspective, those drops are really the errors.

There’s an old saying on Wall Street that “bull markets go up the staircase while bear markets jump out the window.” That’s very true and you can really see the impact by looking at the long term.

Permit me a brief thought experiment. Think of investing as a roulette wheel with very unusual rules. You spin the wheel once a year, and you face two possible payoffs. You have either an 85% chance of making 15% on your investment next year, or you have a 15% chance of losing 20%.

I made up those numbers, but it’s close to what investors actually see. The long-term payoff is close to 10% but the key is that you have to keep playing through those 20% drawdown years. In fact, the odds are high that in an investing lifetime, you’ll almost certainly see two bad years within a five-year span.

The other part of this thought experiment is that bull markets can seem, to a rational observer, unusually hot. After all, the market is performing at a 50% faster rate than its long-term average, and that can happen for several years. This causes too many investors to jump ship too soon, and that’s a big mistake.

One of my favorite quotes from Peter Lynch is, “Far more money has been lost by investors’ preparing for corrections, or trying to anticipate corrections, than has been lost in the corrections themselves.”

Target to Start Membership Program

Shares of Target (TGT) got a nice 12% boost today after the retailer said it’s going to start a paid membership program next month. Of course, this is exactly what other retailers like Amazon and Walmart do. I’m curious what took Target so long. Amazon Prime is a smash hit, and Walmart said that Walmart+ has been doing very well.

The new service will be called Target Circle 360. The service “will include unlimited free same-day delivery for orders over $35 in as little as one hour with no delivery fees and free two-day shipping, along with other perks.”

The initial price will be $49 per year, but it will bump up to $99 per year after the initial promotion ends on May 18.

I’ve been following Target recently and the retailer appears to be at a turning point. There are still a lot of problems at Target, but for the first time in a long time, the company may be a worthwhile investment.

The shares had not been performing very well versus the overall market until late last year.

Then in November, Target released an encouraging, but not great, earnings report. I don’t want to overstate the case because Target still has problems. For Q3, same-store sales fell by 4.9%. Retail is a tough game, and it’s especially hard if your sales are falling. Retail is all about managing your inventory efficiently and getting the lowest price to your customer.

Still, the company said in November that it had improved its efficiency and was managing its inventory better. For its fiscal Q3, Target made $2.10 per share which was well ahead of the consensus for $1.48 per share. After the November report came out, the stock jumped 17% in one day.

Today, Target reported its fiscal-Q4 earnings, which covers the important holiday shopping season. Once again, Target didn’t have great news to report but it was a lot better than was feared. Same-store sales fell 4.4%. That was the third drop in a row. For the first time since 2016, Target’s annual sales fell.

For earnings, Target made $2.98 per share for its Q4. That was much better than Wall Street’s consensus for $2.42 per share. Target’s own range for earnings was $1.90 to $2.60 per share. Quarterly revenue hit $31.92 billion which was $90 million better than consensus.

For Q1, the current quarter, Target sees same-store sales falling by 3% to 5%, and earnings ranging between $1.70 and $2.10 per share. For the full-year, Target expects same-store sales to be flat to -2%, and full-year earnings coming in between $8.60 and $9.60 per share. That’s not great, but it could have been much worse.

Turnaround plays are tough. I generally avoid them. The issue is that investors need to figure out which is a fixable problem and which is not, because once a company loses its competitive edge, it’s very difficult to get it back. I’m pleased to see the progress at Target but the company still has to do more.

JetBlue and Spirit Call Off Merger Plans

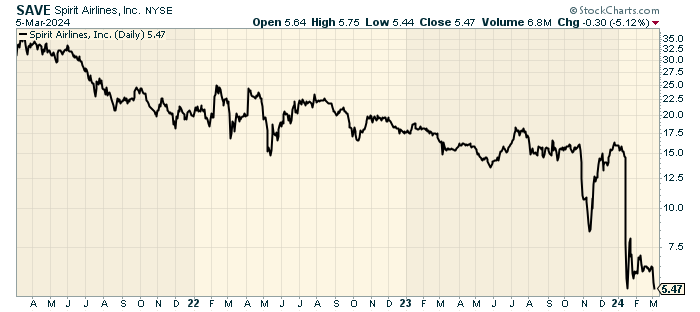

JetBlue (JBLU) and Spirit Airlines (SAVE) finally ditched their plans for a $3.8 billion merger. The Biden administration fought to stop the deal, claiming it would harm consumers. In January, a federal judge sided with the administration and blocked the deal.

The two airlines had been looking to appeal the decision but have now agreed to part ways. JetBlue now owes Spirit a breakup fee of $69 million and $400 million to Spirit’s shareholders. I’ll be honest—Jet Blue shareholders dodged a big bullet with this one.

Despite the payment, Spirit is in very rough shape. They weren’t pursuing this deal because they wanted to but because they had to. In the chart above, notice how badly shares of SAVE got punished after the judge’s decision in January.

Spirit is a mess. The airline has a massive debt load, and they haven’t turned a quarterly profit since Covid. The airline is projected to lose money this year and next year as well. Perhaps someone else will buy them. Frontier (ULCC) had been kicking the tires, but they were eventually outbid by JetBlue.

I bet Frontier or someone else could get a good deal, but taking on Spirit won’t be easy. The DOJ will almost certainly challenge any deal.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want more info on our ETF, you can check out the ETF’s website.

Posted by Eddy Elfenbein on March 5th, 2024 at 6:40 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His