CWS Market Review – April 16, 2024

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

The stock market is finally showing some cracks. Yesterday, the Dow soared more than 400 points during the day only to close lower by 248 points. The S&P 500 slipped another 0.21% today. The index finished the day at its lowest level since February 21.

On Monday, the S&P 500 also closed below its 50-day moving average (the blue line). That snapped a streak of 110 days, which is one of the longest such streaks in the last 30 years. (In the mid-1990s, the S&P 500 was trading above its 50-DMA for more than a year.)

Dropping below the 50-DMA can be an omen for a poor or a sluggish market. Not only is Wall Street still rattled by last week’s inflation report but the escalating tensions in the Middle East are also weighing on investors.

To be frank, the recent stock market hasn’t been that volatile. The VIX, which is the volatility index, rose from less than 15 on Thursday to more than 19.5 during the day on Tuesday. It’s just that the previous five months have been unusually calm, so any change from that pattern seems unusually jarring.

We’ve gotten our first batch of Q1 earnings reports. Bank of America (BAC) said its earnings dropped 18%, and it missed estimates by one penny per share. Johnson & Johnson (JNJ) beat by seven cents per share, but the stock hit a new 52-week low. Goldman Sachs (GS) had a strong quarter as its profits rose 28%. Trump Media (DJT) lost 39% in the last week.

A few weeks ago, I mentioned how defensive stocks had been particularly weak. Today was a good example of defensive stocks doing well. In particular, staples and healthcare stocks were up the most, or in many cases, down the least.

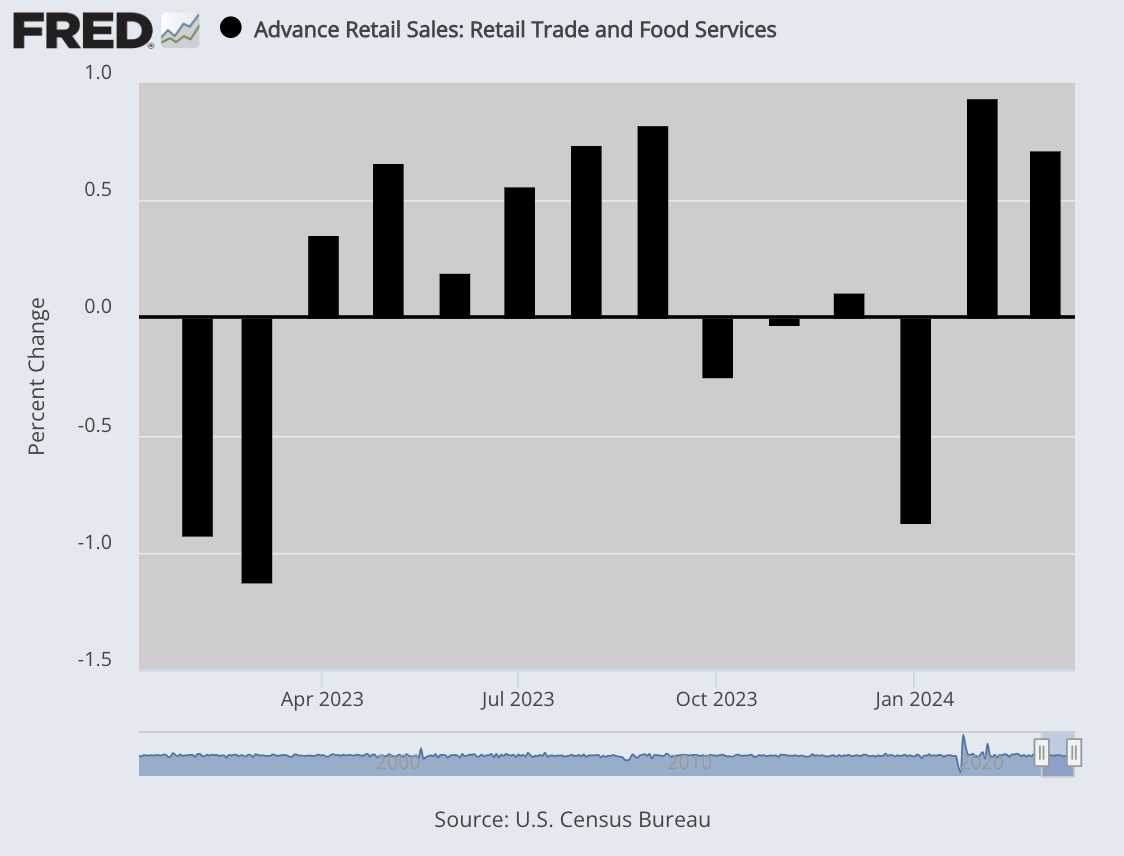

Retail Sales Jump 0.7%

The economic news continues to be favorable. Shoppers are in a buying mood. On Monday, the Commerce Department said that retail sales rose by 0.7% last month.

That was a pleasant surprise. Wall Street had been expecting a gain of only 0.3%. Also, the number for February was revised higher to a gain of 0.9%.

This tells us that despite stubborn inflation, higher prices haven’t kept shoppers from the malls. Over the last year, retail sales increased by 4% while inflation was up by 3.5%.

If we don’t count cars, then retail sales increased by 1.1% last month. That more than doubled Wall Street’s estimates for a gain of 0.5%. It’s true that higher gasoline prices helped drive higher retail sales, but the largest increase came from online sales, which were up by 2.7%. These numbers are important to watch because consumers make up about 70% of the economy.

The Atlanta Fed’s GDP model increased its estimate for Q1 GDP growth from 2.4% to 2.9%. The model now expects real personal consumption expenditures (PCE) to rise by 3.5%. That’s quite good. The government’s initial report on Q1 GDP growth will be out on April 25. The initial report will be updated two more times.

On Tuesday, the Federal Reserve said that industrial production increased by 0.4% last month. That’s good to see because this data series hasn’t done much over the past two years. Last month, manufacturing increased by 0.5%. If we don’t count autos, then factory output was up by 0.3%.

Thanks to the positive economic news, that’s altering the markets’ take on the Fed and the course for interest rates. According to the most recent trading in the futures market, there’s a 65% chance that the Fed’s first rate cut will come in September, and there’s a 51% chance that it will be the Fed’s only rate cut this year.

Earlier today, Fed Chair Jerome Powell conceded that there’s been “a lack of further progress” with regard to inflation. Powell indicated that rate cuts may not be coming so soon. This is a noticeable change from the Fed’s stance of only a few weeks ago.

One effect of higher interest rates is that the US dollar has been getting stronger in recent days. The dollar is also being helped by increased international tensions. When investors get nervous, they go to areas of stability. According to Bloomberg, the greenback is having its best run in over a year.

Until now, investors had assumed that most of the world’s major central banks would cut rates similarly, so therefore, the impact would be negligible. Now that doesn’t appear to be the case.

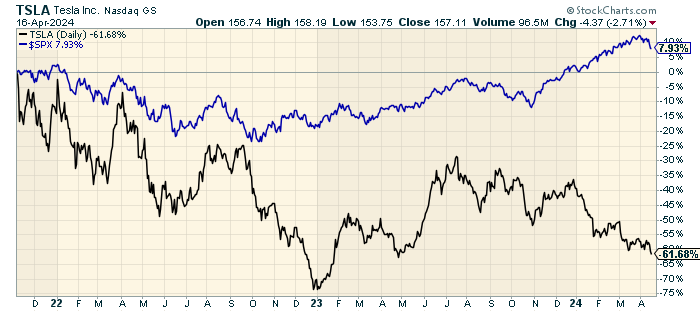

Tesla to Cut 10% of its Workforce

Something on Wall Street that still surprises me is how quickly a stock can go, in Wall Street’s eyes, from doing nothing wrong to doing nothing right.

I say this in the wake of Monday’s news that Tesla (TSLA) will be laying off more than 10% of its global workforce. The electric vehicle leader is facing the reality of slower sales growth. In Q1, Tesla delivered 387,000 vehicles. That’s down 8.5% from last year.

Companies like Tesla are always a challenge for value-oriented investors because embryonic industries are often long on potential but meager with results. How can an investor properly value a stock that’s trading at 100 times trailing earnings but that could be the next Microsoft (MSFT)? It’s a tough question, and I don’t know the answer. I will concede that non-traditional companies should be valued in non-traditional ways.

That’s certainly true for Tesla, but now we’re talking about a company that’s richly valued but may not be growing so quickly. Tesla’s profit margins have consistently eroded. Tesla has also experienced several senior executives leaving the company.

Elon Musk said, “About every 5 years, we need to reorganize and streamline the company for the next phase of growth.” The last time they cut 10% of the workforce was two years ago.

You can see how badly Tesla has lagged the overall market.

Musk is apparently pushing the company hard in the direction of fully-autonomous vehicles. The goal is to unveil a robotaxi sometime this summer. Meanwhile, other car companies are scaling back their EV plans, while hybrid sales are as strong as ever.

These kinds of stocks are often referred to as lottery investments meaning that investors know that 90% of these investments will go nowhere but that a big home run will more than make up for the losses.

Let’s say that forty years ago, you decided that computers were the future. You decided to invest in what most experts believed were the top contenders in the field. That probably would have led you to invest in IBM, Cray and DEC. Lancaster Colony (LANC) would have been a far better investment. They make croutons.

My point is that even if you’re right in your thesis, you can be wrong in your delivery.

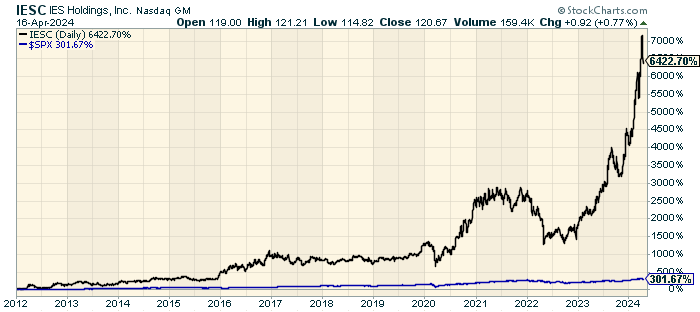

Stock Focus: IES Holdings (IESC)

As long-time readers know, one of my favorite hobbies is to highlight high-quality companies that are practically unfollowed by Wall Street. I’m often asked how to find these stocks, but that’s hard to answer because they’re, by definition, not well known.

Recently, I came across IES Holdings (IESC), which I have to confess I was unfamiliar with. I’m glad I know it now. Twelve years ago, it was going for $1.75 per share. Now it’s at $120. Still, not a single analyst covers it.

IESC has done so well that the S&P 500 looks like a flat line in comparison.

According to Wikipedia, IESC “provides infrastructure services including electrical, communications, low-voltage, network, AV, and security alarm systems to the residential, industrial and commercial markets.”

IESC isn’t some microcap. The company has 8,300 employees and a market value of $2.4 billion. The company was founded in 1997 and it’s based in Houston.

For the most recent fiscal year (ending in September), IESC made $4.71 per share. IESC’s next earnings report will probably be out in early May, but I can’t say what Wall Street’s consensus is since there isn’t one.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want more info on our ETF, you can check out the ETF’s website.

Posted by Eddy Elfenbein on April 16th, 2024 at 6:23 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His