CWS Market Review – May 27, 2025

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

The stock market got a nice bounce today after President Trump said he’s going to delay the 50% tariffs on the EU.

It’s interesting how any news of a tariff pause sends the bulls charging but any warning of tariffs to come brings out the bears. It’s clear that Wall Street doesn’t like tariffs.

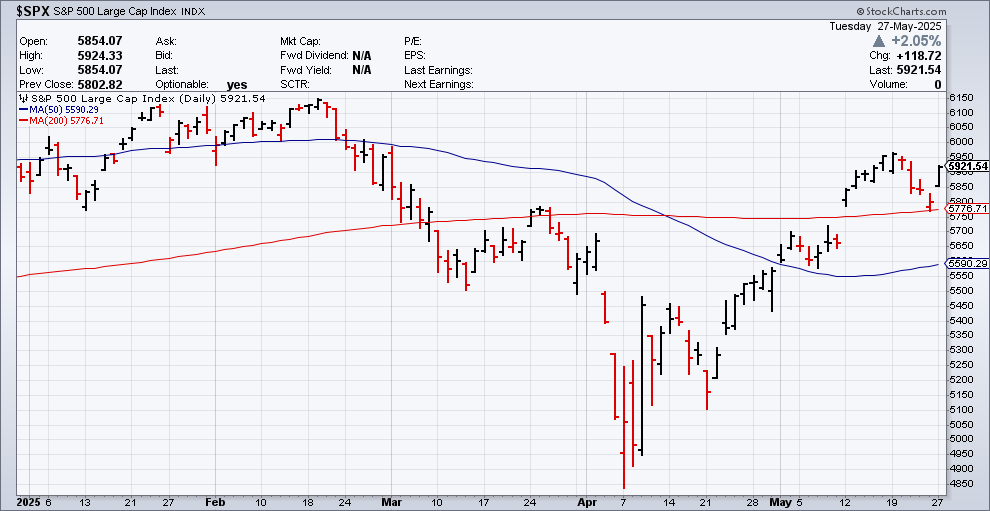

At one point, the Dow was up more than 740 points today. The S&P 500 was up by 2.0% while the Nasdaq was up by 2.5%. I talk a lot about the 200-day moving average. This is a good example of why. The S&P 500 bounced almost perfectly off its 200-DMA. The Russell 2000 was particularly strong today.

President Trump said he’ll push the EU tariffs back to July 9. He’s making the move as part of a request from Ursula von der Leyen who is the president of the European Commission. The original date for the tariffs was for June 1.

President Trump took to Truth Social: “This is a positive event, and I hope that they will, FINALLY, like my same demand to China, open up the European Nations for Trade with the United States of America.” The EU said it will fast-track trade talks with the U.S.

Through May 19, the S&P 500 had put together a very nice run of 17 up days in 20 sessions. That came to an end last week as the index fell on Tuesday, Wednesday, Thursday and Friday. Today’s rally is walking back most of last week’s damage.

The 30-year Treasury yield fell back below 5%. There were some concerns last week when a Treasury auction showed unusually light interest. This was particularly worrying to some because it shortly followed the credit downgrade from Moody’s.

Interestingly, shares of Tesla (TSLA) got a nice boost today after Elon Musk said he’s going to pull back on his political endeavors. Tesla sold only 7,261 cars in Europe in April. That’s down 49% from last year. The overall EV market saw an increase of 34.1%. Shares of Tesla have lagged the market for more than three years.

When a stock goes up, shareholders will forgive most anything. But when a stock starts to slide, their patience wears thin. All things being equal, I prefer to invest in a company whose CEO keeps a low profile.

We’re not quite done with earnings season, but we’re getting very close. So far, 95% of the companies in the S&P 500 have reported results. Of those, 78% have topped estimates. This week, we’re getting Nvidia’s (NVDA) earnings report which will be very closely watched. The report is due out after tomorrow’s closing bell. Wall Street expects earnings of 75 cents per share. That’s up from 61 cents per share for last year’s fiscal Q1.

The other earnings report to look out for will come from Costco (COST). I highlighted the company last week and explained why I’ve been such a big fan over the years. Last time, Costco had a rare earnings miss ($4.02 versus $4.10 per share). This time, Wall Street expects earnings of $4.23 per share. Costco’s earnings report is due out after the closing bell on Thursday.

We also had good economic news this morning. It seems that consumers are in a much better mood. This morning, the Conference Board’s Consumer Confidence Index came in much stronger than expected. For May, Consumer Confidence was 98.0. That’s an increase of 12.3 points over April. For May, Wall Street had been expecting 86.0.

This snaps a streak of five straight monthly declines. What caused the surge? It seems that President Trump’s decision on May 12 to hold back on the most severe tariffs certainly played a role.

The present situation index increased to 135.9, up 4.8 points, and the expectations index posted a major surge to 72.8, a 17.4-point gain. Investors also showed more optimism, with 44% now expecting stocks to be higher over the next 12 months, up 6.4 percentage points from April.

Views on the labor market also improved, with 19.2% of respondents expecting more jobs to be available in the next six months, compared with 13.9% in April. At the same time, 26.6% expect fewer jobs, down from 32.4%. However, the level of respondents saying jobs were “plentiful” edged higher to just 31.8%, while those saying employment was “hard to get” increased to 18.6%, up 1.1 percentage points.

Consumer confidence was higher for every income bracket. Consumer confidence is an interesting metric to watch because it’s not visible and it’s hard to measure, but if you don’t have it, it can be terrible.

Last week, we had a great earnings report from one our Buy List stocks. Intuit (INTU), the TurboTax people, reported earnings of $11.65 per share. That was up 18% over last year, and it beat Wall Street’s consensus of $10.91 per share.

The CEO said Intuit is “becoming a one-stop shop of AI-agents and AI-enabled human experts to fuel the success of consumers and small and mid-market businesses.”

But the best news is that Intuit raised its full-year guidance. Intuit now see its profits ranging between $20.07 and $20.12 per share. That’s a growth rate of 18% to 19%. The previous guidance had been for 13% to 14%.

Shares of Intuit jumped 8.1% on Friday, and another 3.4% today. The shares hit a new 52-week high today. I won’t give you the “hard sell,” but you can sign up for our premium newsletter here. This is where we discuss our Buy List in greater detail.

The Federal Reserve doesn’t meet for another three weeks, but tomorrow the Fed will release the minutes of its last FOMC meeting. At that meeting, the Fed decided against raising interest rates, which was widely expected, but I’ll be curious to see what the reasoning was inside the Fed.

Over the last few weeks, the market has gradually changed its outlook for the Fed. Wall Street no longer sees the Fed as being willing to lower rates so aggressively.

Futures traders currently see the Fed lowering interest rates in September, but even that’s not an overwhelming proposition. The current probability of a September rate cut is 62%. The market only expects two rate cuts for the rest of this year.

Also today, the Atlanta Fed’s GDPNow model sees Q2 growth of 2.2%. That’s down a little from the prior forecast of 2.4%. The estimate for real gross private domestic investment growth fell from +0.7% to -0.2%. Today’s Case-Shiller Index on home prices showed the first monthly decline in home prices since 2023. The data is seasonally adjusted.

On Thursday, the government will update its report on Q1 GDP growth. The initial report said that the economy grew by only 0.3% for the first three months of this year. I don’t expect to see much of a change.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on May 27th, 2025 at 5:51 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His