CWS Market Review – May 6, 2025

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

Over the weekend, Warren Buffett announced that he’s stepping down as CEO of Berkshire Hathaway. On January 1, Greg Abel will take over. Berkshire’s board unanimously approved Buffett’s suggestion. Buffett is 93 years old.

Yesterday, the A shares of Berkshire fell $40,000. I guess that’s a good sign of Wall Street’s respect for Buffett.

Buffett’s track record is simply amazing. Since 1965, Berkshire has gained 5.5 million percent while the S&P 500 has gained a measly 39,000%. That means that if Berkshire fell by 99% tomorrow, it would still be outperforming the market.

Until the big sector rotation earlier this year, CWS had (barely) outperformed Berkshire over a seven-year run. As for the other 60 years, ol’ Warren’s got a big edge.

To be fair, most of Berkshire’s really big years came decades ago. Even Buffett has conceded that his portfolio won’t do as well as it did. Before Monday’s big drop, one share of Berkshire was worth more than $800,000.

I wish Mr. Buffett a happy retirement.

Yesterday, the stock market snapped its nine-day winning streak. The decline wasn’t that bad (-0.64) but it was the first daily drop since April 21.

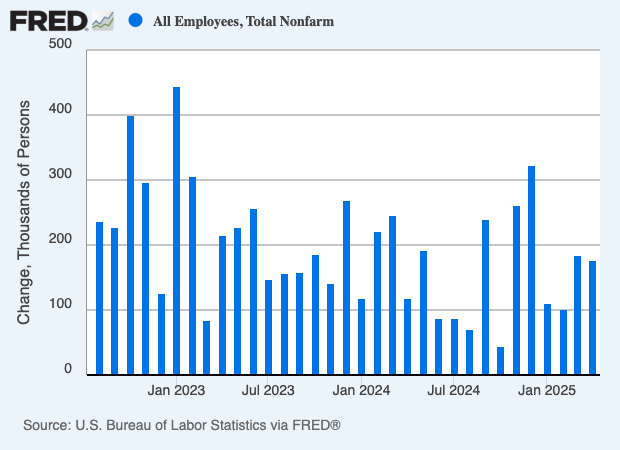

On Friday, the Labor Department said that the U.S. economy added 177,000 nonfarm payrolls last month. That news surprised Wall Street. Economists had been expecting an increase of just 133,000.

The figure for March was revised lower by 43,000 to 185,000. The February number was lowered by 15,000.

The unemployment rate held steady at 4.2%, which is low by historic standards. In fact, the unemployment rate last month was lower than every single month from 1971 to 1998.

The key stat I like to watch is average hourly earnings. After all, worker pay eventually translates to revenue for a company. Last month, average hourly earnings rose by 0.3% which was 0.1% below expectations. Over the last year, average hourly earnings increased by 3.8% which isn’t much higher than inflation.

The labor force participation rate increased to 62.6% and the broader U-6 rate dropped to 7.8%. Wall Street has been looking hard for signs of the impact of tariffs but so far, it hasn’t found anything.

Here are some details:

Health care continued to be a leader in job creation, adding 51,000 jobs. Other sectors posting gains included transportation and warehousing (29,000), financial activities (14,000), and social assistance.

The federal government reported a loss of 9,000 jobs on the month amid Trump’s efforts, led by Elon Musk and the Department of Government Efficiency, to trim payrolls in the public sector. Federal government jobs have declined by just 26,000 since January, as employees furloughed but still receiving severance are not counted as unemployed, according to the BLS.

Manufacturing saw a slight loss of 1,000 jobs as well.

President Trump took to Truth Social, “Consumers have been waiting for years to see pricing come down. NO INFLATION, THE FED SHOULD LOWER ITS RATE!!!”

He may get his rate cut soon. The Federal Reserve began its two-day meeting today. The Fed will release its policy statement tomorrow afternoon. I don’t expect to see a rate cut this time, but one may be coming at the Fed’s June meeting, in six weeks.

Traders currently place the odds of a rate cut next month at 68%. All told, traders see the Fed lowering rates by a total of 0.75% by the end of the year. At the June meeting, the Fed will also update its economic projections for the next few years.

Does Job Growth Tell Us When Recessions Are?

I was curious to see how changes in nonfarm payrolls have historically aligned with recessions and expansions.

I reviewed the last 1,000 months’ worth of data. Of those 1,000 months, job growth was negative 219 times. Of those 219 months, the U.S. economy was in a recession for 113 months which is about half the time.

Even when the economy is shedding jobs, that only indicates a roughly 50% chance that the economy is officially in a recession.

For April, job growth was 0.11% which comes in 616th out of the last 1,000 months. The important takeaway is that recessions almost never line up with that type of job growth. To get a real recession, you need more than job losses – the economy needs to be shedding jobs.

Looking at the data, it seems that job growth of -0.13% is the turning point. In today’s terms, that’s a loss of 207,00 jobs. Of the last 1,000 months, there have been 125 months with that level of job losses, and 71% of those months have come during a recession.

Just going by the jobs report, the economy very likely isn’t in a recession. The next big test for the market comes a week from today when the government releases its CPI report for April. The last report showed a tiny bit of deflation.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on May 6th, 2025 at 5:51 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His