CWS Market Review – June 10, 2025

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

On Friday, the S&P 500 closed above 6,000. To be exact, the index closed at 6,000.36. Not many people expected the market to recover so quickly. The last time the S&P 500 closed above 6,000 was on February 21.

On Monday and Tuesday, it closed even higher. We’re now less than 2% from a fresh all-time high. Looking back at the panic this year, it all seems rather silly. We didn’t know what the tariff policy was going to be, and we were less sure of the potential impact.

In any event, investors got very scared. In just 48 calendar days, the S&P 500 lost 18.9%. Then in 63 calendar days, it gained back 21.2%. (Thanks to the lower base, we’re still not quite at a new high despite the gain being greater than the loss. Don’t blame me. Blame math.)

I wonder if a Rip Van Winkle-type of investor who had slept through the entire period would have noticed any difference. By the way, notice how much smaller the high-low bars have gotten since April. We aren’t seeing any dramatic intra-day reversals like we did this past spring.

The U.S. Economy Added 139,000 Jobs Last Month

On Friday, we got the jobs report for May, and it was pretty good. There had been some trepidation going into this report because the ADP report had been quite weak.

Nevertheless, the Bureau of Labor Statistics reported that the U.S. economy created 139,000 net new jobs last month. That was 14,000 more than expected although that was a very conservative expected number. The jobs number for April was revised lower to a gain of 147,000.

Bear in mind that recessions usually align with job losses, not slower gains. There are no signs that we’re in a recession. Of course, that could change.

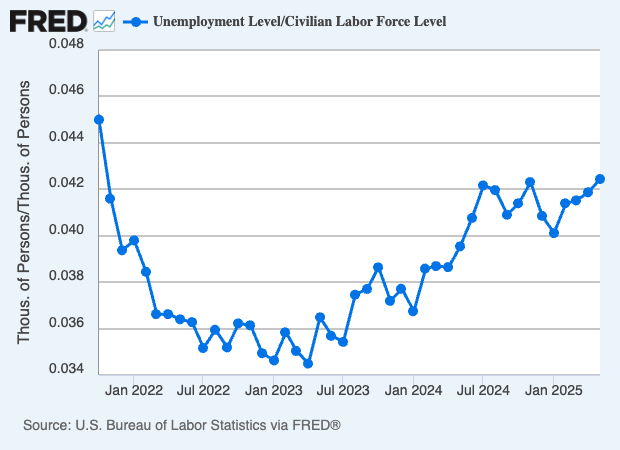

The unemployment rate stayed at 4.2%. I dug into the data and found that if we look at a few more decimal places, then the jobless rate is the highest in 43 months (see below). Although that sounds like a lot, the unemployment rate has really been quite steady. I also like to look at the broader U-6 unemployment rate, and that stayed at 7.8%.

Probably the best news is that average hourly earnings rose 0.4% last month. That was 0.1% better than expected. Over the last year, average hourly earnings are up 3.9%. That’s not bad, but I’d like to see it improve.

Here are some details:

Nearly half the job growth came from health care, which added 62,000, even higher than its average gain of 44,000 over the past year. Leisure and hospitality contributed 48,000 while social assistance added 16,000.

On the downside, government lost 22,000 jobs as efforts to cull the federal workforce by President Donald Trump and the Elon Musk-led Department of Government Efficiency began to show an impact.

The number for April was revised downward by 30,000. The number for March was revised lower by 65,0000. The household survey showed a decline of 696,000 workers. There was a decline of 623,000 full-time folks and an increase of 33,000 parttime workers.

Overall, this was a good report although there are a few signs of weakness. The Federal Reserve meets again next week, and I strongly doubt they’ll make any changes to interest rates. In fact, I don’t see any rate cuts coming in July either.

However, the meeting after that, in mid-September, could be a different story. There’s a decent chance that the Fed will lower rates by 0.25%, but a lot can happen over the next three months. We’ll learn more tomorrow when the government releases the CPI report for May.

Wall Street Goes Nuts for Circle

Wall Street has gone absolutely bonkers recently over the debut of Circle Internet Group (CRCL). The company is a stablecoin issuer which means its coins are tied to the value of the dollar. Hence, the prices are “stable.” This is a major difference from bitcoin which is highly volatile.

What I find interesting about the Circle-mania is that this appears to be another sign of crypto entering the mainstream. Years ago, I think crypto was wrongly seen as a plaything of computer nerds. Now, however, it may be taking on an important role in the financial services sector. If all goes well, then consumers can use stablecoins for fast and secure transactions.

Basically, Circle provides a platform that lets businesses integrate stablecoins seamlessly into their operations.

The stock took off from an offering price of $31 per share to a high of $138 per share. Well, that’s not bad for three days of work (CRCL closed lower for the first time today). The environment has also been helped by a crypto-friendly administration in Washington. The company raised $1.1 billion.

Since the Circle IPO, a few stablecoin ETFs have already rushed in to join the frenzy. I won’t be surprised to see some larger and more established firms issue stablecoins in the coming months.

Circle is the issuer of USDC. In the stablecoin arena, Circle is #2 to Tether. Circle currently has $60 billion in circulation while Tether is up to $150 billion.

Circle makes its money by investing its reserves in U.S. Treasuries. At some point, stablecoins may be thought of as cash, just expressed slightly differently.

Bloomberg says there are now 80 ETFs that track digital assets. One year ago, Bitcoin was trading around $25,000. It recently got as high as $110,000.

Tomorrow, the Senate is scheduled to vote on an important piece of legislation that addresses the stablecoin industry. The bill is backed by the Trump administration and the stablecoin industry.

According to Bloomberg, “The stablecoin bill would set up rules for dollar-pegged tokens used to make payments. The stablecoins would have to be backed one to one with reserves held in short-term investments like federal debt, overseen by federal or state regulators.”

My chief concern about any stablecoin is reserve management. This is why transparency is so important.

The bill has support from both sides of the aisle although some Democrats say the legislation could damage the financial sector. My view is to let 1,000 flowers bloom. If it has a role, the market will quickly adapt.

Casey’s Soars on Earnings Beat

Sixteen months ago, I highlighted Casey’s General Stores (CASY) in the newsletter. I didn’t know the company very well but some friends in the Midwest raved about Casey’s, and it’s very popular there.

It’s basically a gas station masquerading as a pizza shop. Or vice versa. It really doesn’t matter.

The idea is simple. If you drive a car, you’ll need gas. If you’re going to go to a gas station, you might as well choose the place that has pizza as well.

Casey’s is based in Iowa and the stores are mostly in Iowa, Missouri and downstate Illinois. The company also has an impressive presence in the other Midwestern and Plains states. There are now over 2,700 locations in 17 states.

Casey’s prefers to locate in small towns where there’s less competition. There isn’t a Casey’s within several hundred miles of Wall Street.

The stock has been a huge winner over the years. Since 1991, Casey has returned more than 500-fold.

I bring up Casey’s because the stock soared 11.6% higher today after it reported very good earnings. After yesterday’s closing bell, Casey’s said it made $2.63 per share for its fiscal Q4. Wall Street had been expecting $1.95 per share.

Revenues were up 11% to nearly $4 billion which was also better than expected. Casey also increased its quarterly dividend by 14% to 57 cents per share. This is a neat little stock that’s not well-known on Wall Street. The stock is up nearly 60% since I profiled it last year.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on June 10th, 2025 at 6:11 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His