Author Archive

-

It’s Actually Happening

Eddy Elfenbein, February 17th, 2015 at 1:44 pmThe Nasdaq Composite is over 4,900, and it’s within sight of its all-time high reached 15 years ago. The index peaked at 5,048.62 on March 10, 2000. That’s 15 long years without making a new high.

That sounds bad but it’s been worse. The Dow didn’t break its September 3, 1929 high until November 23, 1954.

-

The Market Closed at Another High

Eddy Elfenbein, February 17th, 2015 at 9:37 amI hope everyone had a nice three-day weekend. The stock market closed Friday at a new all-time high. The S&P 500 finished the week at 2,096.99 and the Dow is back over 18,000. This was almost certainly a new inflation-adjusted high. Our Buy List continues to outpace the climbing market as well. I try not to get worked up about short-term moves, but this is nice to see. This month, our Buy List is up 7.88% to the S&P 500’s 5.11%.

Things may get jittery this week as investors turn their attention to the soap opera between Greece and the rest of Europe. The debt talks have broken down but still, investors seem optimistic that some sort of deal will be reached. I think both sides are working hard to position themselves as not “caving in” in the eyes of their respective voters. Once this is achieved, they can hammer out a deal. Consider that consumer prices in Greece have fallen for 23 months in a row. This is a problem that the important people in suits cannot allow to go on much further.

The bond market has quietly retreated over the past few days, bearing in mind that this comes after a spectacular run. The yield on the 10-year Treasury fell as low as 1.65% on January 30 and February 2. Since then, the yield has drifted higher as it’s up to 2.06 this morning. That’s still very low, but it’s interesting to see the bond market finally move downward.

-

Morning News: February 17, 2015

Eddy Elfenbein, February 17th, 2015 at 7:06 amGreek Euro Exit Risk Increases as EU Delivers Ultimatum

EU Hangs Tough, Waiting for Greece to Bend as Euro Wilts

German Investor Confidence Rises to One-Year High Before QE

U.K. Inflation Slows More Than Forecast to Record-Low

Putin’s Paradise Becomes Economic No-Go Zone

U.S. Companies Can Avoid Slow Torture of Venezuela Devaluations by Taking One Big Hit

U.S. Embedded Spyware Overseas, Report Claims

The Price of Getting Apple’s Attention: $12 Billion

Spain’s Caixabank Offers 1 Billion Euros for Whole of Portugal’s BPI

Canada’s Fairfax Snaps Up Lloyd’s Insurer Brit for $1.88 Billion

Liberty Global, Becoming a Big Fish, Risks Attracting the Eye of a Shark

Ford Guns for China’s App Addicts, Seeks WeChat Tie-Up

Dutch Startup WeTransfer Just Raised $25 Million to Expand into the US

Jeff Carter: Are You The Right Investor?

Credit Writedowns: Tax Anticipation Notes: A Timely Alternative Financing Instrument for Greece

Be sure to follow me on Twitter.

-

Jesse Livermore: The Greatest Trader Who Ever Lived

Eddy Elfenbein, February 16th, 2015 at 2:03 pmWhen Jesse Livermore made his first stock trade at the tender age of 15, he didn’t hedge his bets. He consulted the charts he’d compiled working as a chalkboard runner in a Boston brokerage firm, and when the figures for the company in question, Burlington, checked out, he went all in, investing everything he had—all $5—in the railroad. Two days later, he cashed in his shares, for a profit of $3.12.

It was 1892.

Exhilarating, that first taste. The pendulum had begun to swing.

Livermore began to roam the streets of Beantown, frequenting its bucket shops, gambling counters that took bets on stocks without executing actual trades. His ability to recognize patterns in the ticker tape stood him in good stead. In six months, he’d accumulated $1,000. Five years later, it was $10,000—enough to make him persona non grata to every pseudo-broker in the city.

So he moved to New York and graduated to trading with real Wall Street firms. Something, however, was wrong. His system wasn’t delivering as expected. He watched his stake drop, first to $2,500, then to zero. At an age when most contemporary youth were still preoccupied with fraternity smokers and petting, the “Boy Plunger” (turn-of-the-century slang for “reckless gambler”) had already gone through a full cycle of boom and bust.

Livermore decided the problem lay in the lag time between the stock order and the execution of the purchase itself. So he borrowed $500 against future gains. The pendulum began to swing wider. Quickly making back what he’d lost, he increased his stash further, to $50,000. Then, on May 9, 1901, he lost it all, every penny, largely due to the frenzied pace of the day’s trading.

Again he hit the bucket shops, again accumulating a stake that allowed him to get back into the game. He returned to New York with what he termed a “fair-sized roll.” Then, on April 16, 1906, he was hit by a premonition. With no warning, he yielded to a strange urge to sell short a thousand shares of Union Pacific railroad—an urge even he admitted he didn’t understand. Two days later, the San Francisco Earthquake hit. Union Pacific was decimated; he’d made $250,000 literally overnight. Inexplicable, the sudden intuition, but just as inexplicable was what happened next: again trading in shares of Union Pacific, he violated two of his most cherished principles—never heed insider information, and always keep your own counsel—and sold short when a friend tipped him off that the stock was about to tank. It didn’t. His net loss: more than $40,000.

The arcs described by the pendulum continued to widen, the swings to grow ever more vertiginous. During the Panic of 1907, Livermore again shorted the market, earning $1 million in the course of a few days. He then proceeded to lose everything in an attempt to corner the cotton sector, declaring bankruptcy and running up debts of over $1 million by 1916. Once again, he amassed sufficient capital to recover, making first $3 million (in assorted commodities), then $10 million (in wheat). Then came his greatest moment: sensing the impending 1929 crash, he again shorted the market, emerging from the rubble of October 29 with a net profit of $100 million—well over a billion dollars in today’s money.

Five years later, he was bankrupt, his vast fortune completely wiped out, for reasons that remain mysterious even today.

Livermore rallied from his subsequent depression in the late 30s, pooling sufficient energy to write a book detailing his trading principles. But on November 20, 1940, the pendulum swung finally, irrevocably against him. In the cloakroom of the Sherry Netherland Hotel in Midtown Manhattan, he shot himself in the head with a .32 Colt automatic. A suicide note was found scribbled in his notebook: “I am a failure,” it said.

Who was Jesse Livermore? How could the world’s greatest trader, the author of one of the most staggering fortunes America had ever seen, end up hitting the wall in just five years? What drove him to take ever more manic risks with his trades, to the point where the harmonic oscillator of his own speculations ended by ripping him apart?

Livermore himself gives us a clue to his own mystery in Reminiscences of a Stock Operator, the book of interviews he wrote with the journalist Edwin Lefèvre:

The speculator’s chief enemies are always boring from within. It is inseparable from human nature to hope and to fear….The successful trader has to fight these two deep-seated instincts. He has to reverse what you might call his natural impulses. Instead of hoping he must fear; instead of fearing he must hope….It is absolutely wrong to gamble in stocks the way the average man does.

The great trader liked to style himself as a dispassionate analyst. Repeatedly in Reminiscences, we find him stepping back from the welter of the trading floor to admonish himself with conclusions drawn from his market smash-ups—conclusions that read like oracular utterances brought down from the sacred mount of traders: “I learned you must give up trying to catch the last eighth, or the first: these two are the most expensive eighths in the world,” and the like. But the excerpt above intimates that perhaps cold-blooded calculation wasn’t the whole story. That beneath the rational exterior lay something that was not rational, that had to do instead with dreams and forebodings and hidden compulsions. That this aloof, seemingly imperturbable man was in fact deeply attuned to the obscure rumblings of chaos.

For chaotic his life was, in spades. His broker, reflecting on his penchant for cruising the Manhattan streets at night in his canary-yellow Rolls Royce in search of young girls, quipped, “When Livermore is speculating, he is thinking of screwing, and when he is screwing he is thinking of speculating.” His first wife, Nettie Jordan, separated from him one year after their wedding, following a tearful scene in which he begged her to pawn her jewels to finance one of his bankruptcies. His second wife, Dorothy Wendt, was an 18-year-old Ziegfield Follies showgirl who responded to Livermore’s philandering by taking up with a Prohibition agent; after separating from both men, she went on to shoot her 16-year-old son, Jesse, Jr., through the chest with a .22-caliber rifle. Both Livermore’s son and his grandson were manic-depressive and suffered from alcoholism. Both committed suicide.

Nor was chaos a mere by-product of Livermore’s personal eccentricities—it was his stock in trade. The Great Bear of Wall Street made his greatest profits when he sold short, that is to say, when he capitalized on other traders’ helplessness in the face of their own hopes and fears. In an age when Wall Street optimism was almost an American religion, he learned to read, and profit by, the dark anxieties that flowed just beneath the surface of the zeitgeist and that were liable to break out at any moment. He was an expert at sensing the nature and scope of mass hysteria, the thresholds at which men begin to panic. It’s no accident, then, that his favorite book was Extraordinary Popular Delusions and the Madness of Crowds, the Scottish philosopher Charles Mackay’s dark treatise on the power of the irrational in history. Nor is it an accident that, in seeking to harness the forces of unreason that he knew so intimately, he ended up betrayed by them—betrayed and, ultimately, destroyed.

The man who all his life sought to codify the workings of the market into a foolproof set of rules was the same man who consistently violated those rules, helpless to resist his own compulsions. The man who proclaimed clear-sighted analysis as the key to the charts was also a man haunted by irrational dreams and forebodings, who depended upon an uncanny sixth sense to tell him which way the market was moving, and who ultimately succumbed to the same delusions he fought so hard to keep at bay.

Traders are not the same as investors. Investors, however aggressive, are devotees of the long term. Personality-wise they tend to be more sober, more thoughtful and restrained, a la Warren Buffett or Peter Lynch. Volatility is, if not their enemy, then at best an unpredictable confederate, to be regarded with suspicion. Traders, by contrast, live in the moment. They operate by learning to feel the market, sensing when to cut their losses, when to double down, when to follow the trend and when to go against everyone. Far from being adverse to volatility, they secretly hope to get inside it, to understand it and so ride it to victory.

Like all traders, Livermore dreamed of beating the market, pinning his hopes to the forces of order: reason, logic, calculation, monetary self-discipline. Yet like all traders, he ultimately came face to face with that which cannot be rationalized, not just in the great hurly-burly of Wall Street but inside himself, in the shadowy realm where desire becomes compulsion and ambition self-destructive obsession. So that in the end, his battle with the market was a stand-in for his larger battle with himself.

Livermore was well aware of the chaos inside him. That’s why, early in his career, he invested in $800,000 worth of annuities for his wife and children that he himself would be unable to touch: “I knew a trading man will spend anything he can lay his hands on. By doing what I did my wife and child are safe from me.”

In the end, Livermore’s dream was the great, illusory dream of gamblers everywhere: to impose form and coherence on chance itself. But he failed to treat chance with the proper respect: he got too close. His story reads like a dark pendant to that other great 1920s story of lives lost to the pursuit of wealth, The Great Gatsby. Like Fitzgerald’s hero, Livermore sought to define himself against the huge forces that were shaping an America on the verge of empire. His failure, no less than Gatsby’s, is a grim parable of the fate of the individual in the age of money.

(You can sign up for my free investing newsletter here.)

-

Morning News: February 16, 2015

Eddy Elfenbein, February 16th, 2015 at 7:16 amGreek Markets Hold Steady as Crucial Debt Talks Approach

Euro Zone December Trade Surplus Higher Than Expected

Japan’s Out of Recession – But Not With Any Great Conviction

Oil Steadies Around $61, Kuwait Sees Prices Supported

Hackers Steal Up to $1 Billion From Banks, Security Co. Says

HSBC Says Sorry Over Past Standards at Swiss Bank

Currency Battle is Tethered to Obama Trade Agenda

With Port Talks Gridlocked, White House Move Ramps Up Pressure For a Deal

AIG Profit Drops 67% And Misses Street Estimates

Amazon Drone Plans Shot Down By Authorities

Infosys Buys Automation Tech Company Panaya Valued at $200 Million

Putin Lets Consumers Feel Pain as Russian Slump Deepens

Pinterest is Reportedly Trying to Launch a “Buy” Button This Year

Jeff Miller: Weighing the Week Ahead: Will Energy Stocks Support the Market Breakout?

Epicurean Dealmaker: Goldman Sachs Doesn’t Care What You Think

Be sure to follow me on Twitter.

-

Dividend Champions

Eddy Elfenbein, February 13th, 2015 at 11:43 amDividend Growth Investor tells me that the S&P 500 Dividend Aristocrats is an incomplete list. For example, the steel company Nucor paid a special dividend on top of its regular dividend. When they ended their special dividend, S&P considered that to be a dividend cut even though they continued to raise their regular dividend. That doesn’t seem fair.

Instead of the Dividend Aristocrats, Dividend Growth Investor recommends the Dividend Champions list complied by David Fish. That list has over 100 names. Fish also includes stocks that have raised their dividends at least 10 years in a row, and at least five years in a row. You can see the Dividend Champions here.

-

CWS Market Review – February 13, 2015

Eddy Elfenbein, February 13th, 2015 at 7:08 am“Reversion to the mean is the iron rule of financial markets.” – Jack Bogle

Jack’s right. Not only do markets revert to the mean, but sometimes that reversion can be quite mean. By now, you’ve probably gathered that I’m not much of a fan of market forecasts. People often ask me where I think the market will be in six or twelve months. My answer: “beats me!”

The past few days are a great example of why it’s so hard to predict the market. Not only is it impossible, but it’s unnecessary as well. Just a few days ago, everyone seemed so down on the S&P 500. On February 2, the S&P 500 reached an intra-day low of 1,980.90; that’s 5.4% below the all-time intra-day high reached five weeks before. But since then, the market has rebounded impressively. On Thursday, the S&P 500 reached its highest close this year. (Maybe the market was rooting for the Patriots?)

In this week’s CWS Market Review, we’ll take a closer look at the market’s recent uptick. Our Buy List stocks continue to do well. Qualcomm ($QCOM) finally reached a deal with the Chinese government. It’s not every day you agree to fork over $1 billion and your stock shoots up. I suppose investors expect the worst when dealing with the PRC. I’ll also preview two more Buy List earnings reports coming next week, Wabtec ($WAB) and Hormel Foods ($HRL). But first, let’s take a look at the market’s recent rally.

The S&P 500 May Be at an All-Time Inflation-Adjusted High

On Thursday, the S&P 500 ended at 2,088.48 for its highest close this year. The index may have closed at an all-time inflation-adjusted high. That hasn’t happened in nearly 15 years. The only problem is, we can’t say for sure until the CPI for February comes out in about five weeks.

Here’s how it works. The S&P 500 made its all-time inflation-adjusted high on March 23, 2000. The index closed that day at 1,527.35. That’s actually one day before the market peaked, but the one-day gain was less than the rate of inflation. Going by the recent CPI data, which is for December, the close from March 23, 2000 works out to 2,099.30 in today’s dollars.

Here’s the catch: The CPI has been falling lately thanks to lower oil. As a result, the all-time inflation-adjusted high has been falling as well. The S&P 500 closed 0.52% below its inflation-adjusted high. So the question is, have prices deflated that much this year? I don’t know. But the lesson for investors is that the market can go a long time without making any real gains. Another lesson is the importance of dividends. Once we include dividends, the S&P 500 is well above its 2000 peak, with or without inflation.

I’m also happy to say that our Buy List has been doing very well lately. Our Buy List beat the S&P 500 for eight days in a row, and it came close to making nine days on Thursday. Thanks to some strong earnings reports, our Buy List is up 6.99% so far this month compared with 4.69% for the S&P 500. That’s a pretty big gap for such a short time period.

I should point out how conservative our Buy List truly is. Last year, the daily changes of our Buy List correlated more than 93% with the daily changes of the S&P 500. It will probably be about the same this year. Many active managers would try very hard to avoid such a high correlation with the overall market. After all, they want to show how they stand apart from everyone else. For me, I don’t mind following the market so closely. I know that over time, the superior characteristics of our strategy will come forward, and that’s happened many times over the last ten years.

Qualcomm Settles With the PRC

Qualcomm ($QCOM) has been our leading candidate for Dud of the Earnings Season. Even in top-notch portfolios, there’s always going to be one. Actually, Qualcomm’s earnings were quite good. The company pulled in $1.34 per share for Q4. That beat estimates by nine cents per share.

The problem was Qualcomm’s guidance. Before, the company said to expect full-year earnings of $5.35 per share. In the earnings report, they said they’ll range between $4.75 and $5.05 per share. As you might imagine, Wall Street was not pleased. The stock dropped 10% in one day.

This week, Qualcomm announced that they’d reached a deal with the Chinese government. The company will pay a fine of $975 million due to their “anti-competitive practices.” If I were the cynical type, I’d mention the irony of this charge coming from a one-party state. Since I’m not, I won’t. The fine works out to about 60 cents per share. The deal also calls for Qualcomm to lower the royalty rate they get on their patents.

The good news from this deal is that it doesn’t alter Qualcomm’s business model. A lot of people were expecting much worse. The company gets about half of its revenue from China. Qualcomm actually raised the lower end of its guidance by ten cents per share. Excluding the fine, Qualcomm now expects earnings to range between $4.85 and $5.05 per share.

This is very good news for Qualcomm. They really dodged a bullet. I think some other countries may try to pile on like South Korea, but China is the biggie. From the low on February 2 to the high on February 11, Qualcomm rallied 14%. After the earnings report, I cut my Buy Below to $66 per share. As is often the case with investing, doing nothing probably would have been a better move. In any event, I’m going to raise our Buy Below on Qualcomm to $72 per share.

I faced a similar situation with Ford Motor ($F). Since October, I’ve had my Buy Below for Ford at $17 per share, and I resisted lowering it for as long as I could. The stock reacted poorly in January to what I thought was a fine earnings report so I relented and lowered my Buy Below to $16 per share.

Sure enough, a strong sales report sparked a rally. I don’t know if that’s reversion to the mean, or if it was simply people realizing that this stock recently raised its dividend by 20% and now yields 3.7%. Ford is also sticking by its forecast of $8.5 billion to $9.5 billion in pretax profit this year. This week, I’m raising my Buy Below on Ford to $17 per share.

By the way, if you’re looking to add new money to the market, some of our tech stocks are looking very attractive right now. Our four worst-performing stocks so far this year are all tech stocks; Microsoft, eBay, Oracle and Qualcomm. The weakness in overseas economies is taking a toll on these stocks. I’ve already discussed Qualcomm, but I think the other three are going for very good prices at the moment.

For example, Microsoft ($MSFT) is trading at 14.7 times next fiscal year’s earnings. Let’s remember that this is one of very few AAA-rated stocks. A lot of companies can’t say that. Actually, a lot of countries can’t say that. Microsoft just floated a huge bond deal this week, which included 40-year paper. That coupon is just 4%. Microsoft is also sitting on $90 billion in cash, and over 90% of that is outside the United States. It looks like Congress is getting serious about a deal that would allow companies to bring that money home at a reduced rate. The stock has recently dropped which broke a long uptrend (see below). Microsoft is a good buy up to $45 per share.

The situation at Oracle ($ORCL) isn’t quite as rosy. The company had missed earnings for four straight quarters. They finally delivered an earnings beat in December, and the stock shot up, but it’s been pretty lackluster ever since. The good news for Oracle is that they’ve been catching up with their cloud business. The company reports earnings again next month, and I want to see more confirmation of their progress before I say it’s a very attractive buy. For now, Oracle remains a decent buy up to $48 per share.

Upcoming Buy List Earnings Reports

We still have a few more earnings reports to go for Q4 earnings season. I have to explain that companies sometimes take a little longer to report their Q4 earnings. The SEC grants a little extra time for companies to report their fiscal Q4 than with the other three quarters. As a result, some of the later Q4 earnings reports tend to overlap with the earnings reports of companies who end their quarters in January. Next week, two of our new Buy List stocks report earnings, Hormel Foods and Wabtec. But Wabtec’s quarter ended in December, while Hormel’s ended in January. The same thing will happen the week after when Express Scripts (December) and Ross Stores (January) are due to report.

Wabtec ($WAB) is due to report on Wednesday, February 18. This is a very strong company. Wabtec is the only stock on any U.S. exchange that’s risen in each of the last 13 years. If you’re not familiar with WAB, they make locomotives, brakes and other parts for the freight- and passenger-rail industries. In October, Wabtec raised its Q4 guidance to 91 to 95 cents per share. Look for good more good results. I rate Wabtec a buy up to $90 per share.

Hormel Foods ($HRL), the Spam company, is due to report earnings on Thursday, February 19. It was just reported that Hormel is close to a deal to buy Applegate Farms, a privately held firm that makes organic products. The deal could be between $600 million and $1 billion.

For Q4 earnings, Wall Street expects earnings of 64 cents per share. In December, Hormel said to expect full-year earnings to range between $2.45 and $2.55 per share (their fiscal year ends in October). Also in December, Hormel raised their dividend by 25%. It was their 49th consecutive annual dividend increase. Not bad for lunch meat. Hormel is a buy up to $56 per share.

That’s all for now. The stock market will be closed on Monday for George Washington’s Birthday. The NYSE makes it very clear that officially, the holiday is not President’s Day but Washington’s Birthday. Next Wednesday will be an important day. We’ll get key reports on industrial production and capacity utilization. The Federal Reserve will also release the minutes of their last meeting. It will be interesting to hear more details on the Fed’s thinking. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

-

Morning News: February 13, 2015

Eddy Elfenbein, February 13th, 2015 at 7:03 amPutin’s High Tolerance for Pain and Europe’s Reluctance to Inflict It

Time For Germany To Leave The Euro; German GDP Growth Unexpectedly Strong

Greece, Germany Said to Offer Compromises on Aid Terms

Banks’ Ability to Delay Currency Trades May Not Be Fair

Orbitz Meets Estimates, Shares Up on Expedia Merger News

AmEx-Costco Divorce Shakes Up Card Industry

Groupon Beats on Revenue But Misses Expectations on 1Q Forecast

Kellogg Posts Loss, Cautions on Outlook

Lyft Said to Talk With Investors on $250 Million in Funds

Rolls-Royce Warns on Impact of Oil Price Fall

ArcelorMittal Reports Fourth Quarter 2014 and Full Year 2014 Results

The Big Lesson From a Bet With Warren Buffett

Joshua Brown: This Is The Big One

Be sure to follow me on Twitter.

-

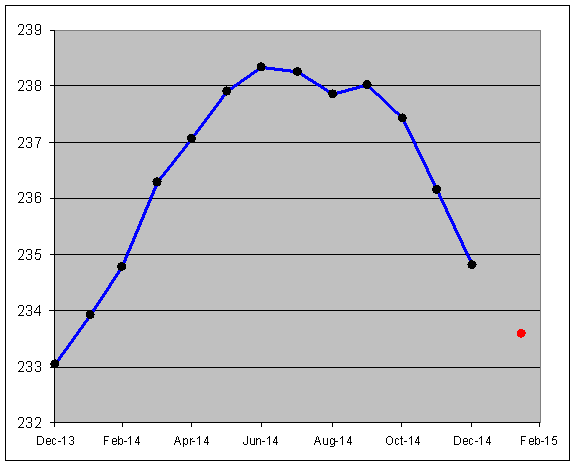

A New Inflation-Adjusted High?

Eddy Elfenbein, February 12th, 2015 at 4:14 pmThe S&P 500 may have closed at an all-time inflation-adjusted high today. The problem is we can’t say for sure until the CPI data for February comes out in about five weeks.

Here’s how it works. The S&P 500 made its all-time inflation-adjusted high on March 23, 2000 at 2,099.30 (1,527.35 nominal). That’s actually one day before the nominal high. That figure is as of the last CPI data point which is for December 31, 2014.

The CPI for December was 234.812. Here’s the catch: The CPI has been falling lately thanks to lower oil. As a result, the all-time inflation-adjusted high has been falling as well.

Today’s close was 2,088.48. That’s 0.52% below the inflation-adjusted high. So the question is, have prices deflated that much so far this year? I don’t know. The January CPI comes out in two weeks.

The blue line is the CPI (not seasonally adjusted). I added the red dot as the tipping point. If the blue line has trended down BELOW the red dot, then today’s close is an all-time inflation-adjusted high. If the blue line has trended above the red dot, then we’re still short of it.

-

Updated S&P 500 Dividend Aristocrats

Eddy Elfenbein, February 12th, 2015 at 2:42 pmHere’s an updated list of the S&P 500 Dividend Aristocrats. These are companies that have raised their dividend for 25 years in a row. This list is a great place to find high-quality stocks and you’ll notice a few current Buy List stocks along with some former members. I’ve included each stock, the ticker symbol, when the dividend streak started and the current yield.

That’s quite impressive that a company can increase its dividend every year for a quarter of a century. There’s an ETF which follows this: ProShares S&P 500 Dividend Aristocrats ($NOBL).

The S&P 500 Dividend Aristocrats had a big change this year as Diebold ($DBD) is no longer a member. After 60 straight dividend increases, they weren’t able to do it again. Energen ($EGN) also got booted when they ended their streak last year. Bemis ($BMS) and Family Dollar ($FDO) left due to acquisitions. Sigma-Aldrich ($SIAL) is in the process of being bought out as well, but they’re still on the list for now.

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His