Author Archive

-

Morning News: November 30, 2023

Eddy Elfenbein, November 30th, 2023 at 7:07 amUN Declares 2023 Hottest Year Ever as Crucial COP28 Summit Starts

Why No One Wants to Pay for the Green Transition

Global and Business Leaders Face Questions at New York Times Forum

China Investment Bank Bans Displays of Wealth

Turkey Seeks Gulf Cash for $20 Billion Bet on Transit Trade

Eurozone Inflation Falls Faster Than Expected

Robinhood Opens in Britain with Low-Cost US Trading to Woo Clients

Biggest Blowout in Bonds Since the 1980s Sparks Everything Rally

Goldilocks Meets Santa as Global Stocks Power to Best Month in Three Years

CFOs See Ongoing Pain From Foreign Exchange Oscillations

Banking Escapees Make Billions From Private Credit Boom

Consumers Likely Pulled Back Spending in October

Inside the Battle for OpenAI’s Soul

Big Companies Find a Way to Identify A.I. Data They Can Trust

AbbVie to Buy ImmunoGen for More Than $10 Billion

Cigna-Humana Merger Is Likely to Face Antitrust Challenge

Tata Tech Adds Billions to Market Capitalization in Indian Trading Debut

U.A.W. Announces Drive to Organize Nonunion Plants

Ford Lost $1.7 Billion in Profits from UAW Strike

Pickup or Lunar Lander? Tesla’s Cybertruck Enters a Crowded Market

Red Lobster’s Popular Endless Shrimp Deal Ate Into Its Profits

Be sure to follow me on Twitter.

-

Morning News: November 29, 2023

Eddy Elfenbein, November 29th, 2023 at 8:06 amWelcome to COP28, the U.N. Climate Conference Hosted by an Oil Giant

Saudi Arabia to Host World Expo 2030, in Victory for Crown Prince

House Prepares to Drop China Investment Curbs From Defense Bill

In a Shaky Oil Market, OPEC Has Bitter Decisions to Make

A $30 Billion Rout Shows Toll of Fed Hikes on Biden Energy Goals

The $7 Trillion ETF Boom Gets Blamed Again for Dumb Stock Moves

Bill Ackman Bets Fed Will Cut Interest Rates as Soon as First Quarter

Corporate America Has Dodged the Damage of High Rates. For Now

American Black Friday Sales Signal Tough Holidays for Retailers

The Chicken Tycoons vs. the Antitrust Hawks

KKR to Pay $2.7 Billion for the Rest of Insurer Global Atlantic

OpenAI Director Who Helped Oust Altman Now Key Player in Startup’s Future

U.S. Debates How Much to Sever Electric Car Industry’s Ties to China

G.M. to Cut Spending on Cruise Self-Driving Unit

GM Plans $10 Billion Stock Buyback in Bid to Assuage Investors

Toyota Plans to Reduce Stake in Top Auto-Parts Supplier Denso

Rakuten’s Mobile Misadventure: From Ambitious Plan to Millstone

Disney’s Failing ‘Wish’ Shows Iger Also Has a Princess Problem

Chemours, DuPont, Corteva to Pay $110 Million in Settlement Agreement with State of Ohio

A Master of One-Liners: Munger on Politics, Life and Crypto

Signa Files Insolvency as Cash Crunch Fells Luxury Empire

This 3-Year Cruise Around the World is Called Off, Leaving Passengers in the Lurch

Be sure to follow me on Twitter.

-

CWS Market Review – November 28, 2023

Eddy Elfenbein, November 28th, 2023 at 6:22 pm(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

RIP: Charlie Munger

As I was preparing today’s newsletter, I got the news that Charlie Munger, Warren Buffett’s long-time partner, had died just a few weeks before his 100th birthday.

I don’t have enough time to offer a tribute, but I wanted to share with you some of my favorite Mungerisms:

“Someone will always be getting richer faster than you. This is not a tragedy.”

“People calculate too much and think too little.”

“99% of the troubles that threaten our civilization come from too optimistic accounting.”

“Knowing what you don’t know is more useful than being brilliant.”

“Investing is where you find a few great companies and then sit on your ass.”

“A lot of people with high IQs are terrible investors because they’ve got terrible temperaments.”

“It’s waiting that helps you as an investor, and a lot of people just can’t stand to wait.”

“Necessity never made a good bargain.”

“It is remarkable how much long-term advantage people like us have gotten by trying to be consistently not stupid, instead of trying to be very intelligent.”

Rest in peace, Charlie.

A Great Month for Stocks

This has been a very good month for stocks. Unless something major happens later this week, November will go down as one of the best months for the S&P 500 in years.

I’m also pleased to see that our Buy List has outpaced the market on the way up. So far this month, the S&P 500 has gained 8.6% while the Buy List is up 10.6%.

The reason for the rally is quite simple. Investors have been convinced that the Fed is done, or just about done, with its rate hikes. One of the oddities we’re seeing is that there’s a pronounced gap between the Fed’s tough-sounding rhetoric and the market’s expectations. Even today, Fed Governor Michelle Bowman said that more rate hikes are needed. I’m not so sure she’ll get her way.

The market loves lower interest rates and that appears to be what it will get. The Fed meets again in two weeks and it’s highly unlikely that the FOMC will hike rates. Futures traders see about a one-in-three chance of a rate cut by March.

I’ll give you an example of how much the market loves low interest rates. I ran a test. I took all the data for the S&P 500 and the three-month Treasury yield over the last 18 months.

I then separated the data into three buckets: days when the three-month Treasury yield fell, days when it increased and days when it stayed flat. Then I looked at how the S&P 500 performed on those days.

On days when the three-month yield increased, the S&P 500 fell at an annualized rate of 7.63%. When the yield was unchanged, so were stocks. The S&P 500 rose at an annualized rate of 0.06%. But when the three-month yield fell, the S&P 500 rose at an annualized rate of 41.4%. Falling rates are the fuel of a stock rally.

The good news is that inflation has abated in recent months, but the Fed wants to be clear that it won’t stop hiking until inflation gets back to its target of 2%. This could be a mistake.

I think it’s more important that the trend of inflation heads lower rather than hitting some arbitrary target. Bear in mind that the price for gasoline has fallen for 60 days in a row. At some point, the Fed will have to give in and admit victory.

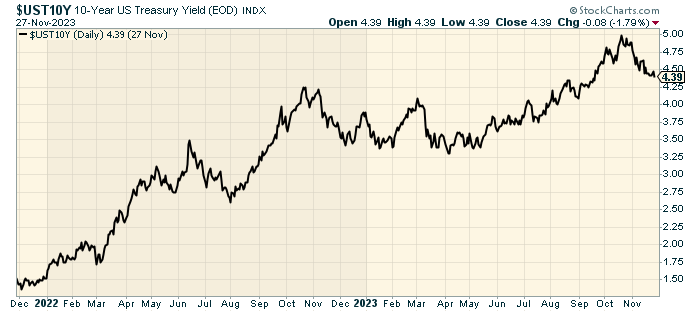

Lately, we’ve also seen a rally in long-term bonds. I’m somewhat hesitant to highlight a drop in long-term yields because it comes after a dramatic rise in yields. The yield on the 10-year Treasury rose from 3.3% in April to 5% in September. It’s back down to about 4.3%.

There are emerging signs that the economy is on shaky ground. The consumer was spending money feverishly this summer, but that’s faded away.

Worst Year for Home Sales in 30 Years

The housing market, in particular, is quite weak. Existing-home sales in the U.S. are on pace for their worst year in three decades. This is the impact of higher mortgage rates. On Monday, the government said that new-home sales fell 5.6% in October.

That was below expectations. Wall Street had been expecting an annualized rate of 723,000 new homes sold. Instead, it was just 679,000.

What’s happening is that so many people locked into mortgages at very low rates. That means that now they’re reluctant to take on new higher-yielding mortgages.

The Fed has thrown a deadly right hook at inflation, and it hit the housing market square in the face. Mortgage rates peaked in October and have started to come down along with Treasury yields.

Tomorrow, the government will revise its report on Q3 GDP growth. The initial report said that the U.S. economy grew in real annualized terms of 4.9% during the third quarter. That was the best quarter for economic growth since Q4 of 2021. Consumer spending greatly helped the economy during Q3.

Wall Street is starting to turn its attention to Q4. The Atlanta Fed’s GDPNow model says that the economy will grow at a 2.1% rate in Q4.

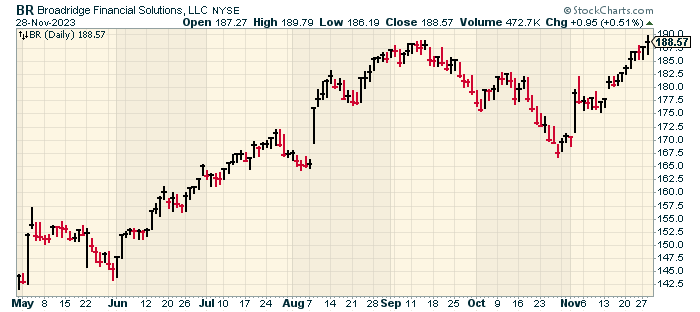

Broadridge Financial Hits New High

As I mentioned before, our Buy List has been acting well lately. I wanted to share with you one of our better-performing stocks which has been Broadridge Financial Solutions (BR).

This is actually a follow-up because I mentioned Broadridge in August 2022 in our free newsletter. At the time, the company had just reported very good results and it had been highlighted in Barron’s. This is part of what the magazine had to say:

Broadridge has been a steady stock for rocky times. That is thanks to a model heavy on recurring-revenue businesses and exposure to long-term trends that should remain in place no matter the near-term path of the economy or interest rates. Broadridge stock’s recent rally could cap gains in the near term, but the company’s long-term positive trajectory remains intact.

The company has a near monopoly in the business of managing and distributing investor communications for practically every public company in the U.S., plus mutual funds, exchange-traded funds, and more. That includes proxies, regulatory disclosures, and other reports and filings required of all U.S. securities issuers. Those are non-discretionary communications that companies and funds need to distribute no matter what the world is doing. That segment tends to grow at the pace of overall stockholdings in the U.S., with Broadridge able to eke out higher profit margins thanks to a continuing shift from printed documents delivered by mail to digital investor communications.

Broadridge also has a smaller but faster-growing segment focused on back-office functions for asset managers, investment banks and broker-dealers. Those include trade processing and settlement, record-keeping, and a variety of other compliance or regulatory functions. That is a software-as-a-service business that has expanded through a combination of organic growth and Broadridge buying companies with adjacent or complementary software and services.

The only thing better than a monopoly is a near-monopoly. It gets less attention from the authorities. The important point that Barron’s covers is Broadridge’s recurring revenue. That’s a great quality for a business to have.

I like looking at BR’s stock chart because you can tell when its earnings report comes out:

Earlier this month, Broadridge reported another strong quarter. For its fiscal Q1, BR earned $1.09 per share. That’s up 30% from a year ago, and it was 12 cents higher than expectations. Total revenues increased 12% to $1.431 billion, and recurring-revenue growth was up by 8%. Last quarter, BR bought back $150 million of its shares.

I’m glad to see that Broadridge is standing by its previous guidance. That calls for recurring-revenue growth of 6% to 9%, and EPS growth of 8% to 12%. The latter works out to a range of $7.57 to $7.85 per share. BR should have little trouble reaching that.

In August, Broadridge raised its annual dividend by 10% to $3.20 per share. The company has now raised its dividend in all 12 years since it went public, and 11 of those increases were by double digits.

The stock hit another 52-week high on Tuesday. We now have a 40.6% gain in Broadridge this year. Broadridge is a good example of a business that’s not well-known but has a strong, durable moat.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want more info on our ETF, you can check out the ETF’s website.

-

Morning News: November 28, 2023

Eddy Elfenbein, November 28th, 2023 at 7:05 amChina’s Property Lifeline Exposes Banks to Big Losses, Job Cuts

The Hong Kong Judge Who Puts Fear Into China’s Deadbeat Builders

Gold Bars and Tokyo Apartments: How Money Is Flowing Out of China

European Fund Giant Amundi Dips Toe Back into Turkey’s Lira

Biggest Climate Talks Ever Confront Global Chaos and Record Heat

BlackRock Sees Bank Reforms Freeing $4 Trillion in Climate Funding

Vietnam Relied on Environmentalists to Secure Billions. Then It Jailed Them

A Psychedelics Boom Is Minting Environmentalists

UBS Chair Kelleher Warns Bubble Is Forming in Private Credit

Ex-Hedge Fund Boss Fights SEC at Supreme Court With Big Backers

Goldman CEO Says Proposed Bank Rules Could Impact Airfares, Pensions

In the Age of Public Salary-Range Listings, Some Jobseekers Feel Duped

Inside U.S. Efforts to Untangle an A.I. Giant’s Ties to China

Chinese Sales Swamp Competition in Soaring Mexican Car Market

Musk’s Cybertruck Is Already a Production Nightmare for Tesla

Tesla Sues Swedish Transport Agency in Dispute Over License Plates

New Bidder Aims to Save Bankrupt Trucking Firm, if Treasury Goes Along

Fashion Retailer Shein Files Confidentially for US IPO

Shein Still Needs to Prove It’s a Bargain

Advertising Is Dead. Long Live Advertising

U.S. Whiskey Is ‘Collateral Damage’ in Trans-Atlantic Trade Fight

Be sure to follow me on Twitter.

-

Morning News: November 27, 2023

Eddy Elfenbein, November 27th, 2023 at 7:02 amBehind Tesla’s Challenges in Making the Cybertruck: Ultrahard Stainless Steel

Global Automakers Turn to China for EV Lessons

China’s Remote Deserts Are Hiding an Energy Revolution

Origin Energy Bidder Doesn’t Know How Much Largest Shareholder Wants

President Biden Plans to Skip COP28 Climate Summit in Dubai

Now for Some Good News About Climate

Javier Milei Needn’t ‘Dollarize’: Market Forces Have Done It for Him

Russian Central Bank to Resume Domestic FX Market Interventions from January

China Scrambles to Contain a Looming Shadow-Bank Meltdown

Goldman’s Jan Hatzius Believes the Hard Part Is Over

Billions Wiped Out as Stock-Safety Trade on Wall Street Misfires

Americans Ditched Big Cities During the Pandemic. Now Many Are Regretting It

Just How Bad Is the US Cost-of-Living Squeeze? We Did the Math

Retailers Have Cleaned Up Their Inventories for the Holidays

There’s a Lot Riding on Black Friday and Cyber Monday

The Biggest Delivery Business in the U.S. Is No Longer UPS or FedEx

Blackstone’s Schwarzman Sees Opportunities in Europe Real Estate

Choice Hotels Prepares to Challenge Wyndham’s Board

Hot Healthcare Hiring Bolsters Cooling U.S. Labor Market

Amazon Once Inspired Fear in the Health-Care Industry. No Longer

How To Make a Weight-Loss Drug Go Viral

Be sure to follow me on Twitter.

-

Morning News: November 24, 2023

Eddy Elfenbein, November 24th, 2023 at 7:04 amA More Moderate Milei Embraces Trading Partners He Had Shunned

Dirty Venezuelan Fuel Imports Threaten Colombian Leader’s Green Credentials

Germany Announces Special Budget to Avert Crisis

Turkey Nears First Bond Sale to Abu Dhabi Fund in Landmark Deal

Mideast Wealth Funds Draw Greater US Scrutiny Over China Ties

Ukraine’s Struggle for Arms and Attention Gives Putin an Opening

Canada’s Real-Estate Market Stumbles as Rate Hikes Bite

Nissan Invests $1.4 Billion to Build Two New EV Models in Britain

Tennessee Zinc Smelter Is at the Center of U.S.-China Trade Fight

Why Americans Can’t Buy Cheap Chinese Electric Vehicles

Auto Dealers Find Savings by Buying Cars Off the Street

Asset Managers Quietly Add ‘ESG’ to Portfolios of Defense Stocks

Muddy Waters’s Latest Target Follows String of Notable Wins

College Dropouts Who Weathered Crypto’s Crash See Promise Ahead

Nvidia Shares Fall as It Reportedly Delays China AI Chip Designed to Comply with U.S. Export Rules

The Pension: That Rare Retirement Benefit Gets a Fresh Look

YOLO Consumers to Decide Winners and Losers This Holiday Season

Black Friday Isn’t What It Used to Be

These Retail Workers Make Your Holiday Shopping Spree Possible

Next Year’s Holiday Gift May Be AI in Your Pocket

Be sure to follow me on Twitter.

-

Morning News: November 23, 2023

Eddy Elfenbein, November 23rd, 2023 at 7:08 amRussia’s Sanctioned Sovcombank Requests US Licence to Make UN Climate Payments

Why Carbon Capture Is Big Oil’s Solution for Climate Change

In Biden’s Climate Law, a Boon for Green Energy, and Wall Street

Turkey Central Bank Hikes Rate by Double the Forecast to 40%

Germany Financial Sector Facing Dark Clouds, Bundesbank Warns

German Budget Mess Could Inflict Big Growth Hit in 2024, BE Says

Dutch Giant ASML Warns Against Labor Curbs After Far-Right Win

Mexico’s Inflation Ticks Up as Banxico Holds Key Rate Steady

Chinese Financial Conglomerate Zhongzhi Has a $31 Billion Problem

China Races to End Property Panic, Fill $446 Billion Gap

Washington Quietly Scrapped a Plan to Save Homeowners Thousands of Dollars

Virgin Money’s Profit Misses Forecasts as Cost Pressures Bite

A $200,000 Pet-Rock NFT Shows How Crypto Is Relapsing Into FOMO

Altman Is Back at OpenAI, But Questions Remain as to Why He Was Fired in First Place

OpenAI Engineers Earning $800,000 a Year Turn Rare Skillset Into Leverage

A.I. Belongs to the Capitalists Now

Judge Says Evidence Shows Tesla and Elon Musk Knew About Flawed Autopilot System

How the Memphis Sanitation Workers’ Strike Changed the Labor Movement

Toy Shoppers Come Down With a Case of the Holiday Blahs

Colt Makes $1.74 Billion Offer for Vista Outdoor, Gate-crashing Rival Deal

Be sure to follow me on Twitter.

-

Morning News: November 22, 2023

Eddy Elfenbein, November 22nd, 2023 at 7:05 amOPEC+ Talks Hit Turbulence as Saudis Agitate Over Output Levels

Andurand Says OPEC+ May Need Deeper Cuts as US Supply Surges

Argentina Is a Textbook Case of ‘Fiscal Dominance’

African Bank Plans Pre-IPO for Shareholders, Eyes 2025 Listing

ECB’s Centeno Says Inflation Expectations Remain Anchored

US Mortgage Rates Slide Sharply, Reinvigorating Housing Demand

Some of America’s Costliest Cities Offer Best Middle-Class Life

It’s the Most Wonderful Time of the Year (for the Economy)

The Rules for Holiday Spending This Year (No. 1: Wait ‘Til December)

American Shoppers Have Plenty of Dry Powder

McKinsey and Its Peers Are Facing the Wildest Headwinds in Years

The Sudden Downfall of Changpeng Zhao, the Crypto Titan Behind Binance

Sam Altman Returns as OpenAI CEO in Chaotic Win for Microsoft

Nvidia Fails to Satisfy Lofty Investor Expectations for AI Boom

The Bill for Offshore Wind Power Is Rising

Ford Resumes Work on E.V. Battery Plant in Michigan, at Reduced Scale

Mary Barra’s $280 Billion Goal Confronts a Litany of GM Hurdles

Why China and Boeing Still Need Each Other

The Old-School Artillery Shell Is Becoming High Tech

Blackstone to Buy U.K. Software Developer Civica

Music Licensing Giant BMI Sells to Private Equity Firm

The Strange $55 Million Saga of a Netflix Series You’ll Never See

How Elon Musk Spent Three Years Falling Down a Red-Pilled Rabbit Hole

Be sure to follow me on Twitter.

-

CWS Market Review – November 21, 2023

Eddy Elfenbein, November 21st, 2023 at 6:13 pm(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

Milei Wins

Earlier this year, I wrote about the stunning presidential primary victory of libertarian economist Javier Milei. This was a major shock, not only to the political establishment, but also to world currency markets. The Argentine Fed responded by raising interest rates 21% to 118%.

Now Milei has been elected president and he has an opportunity to implement his agenda.

The point I want to make wasn’t about the particulars of Argentinian politics but about the interplay of financial markets and government policy. This is an important aspect that’s often overlooked by investors and policy makers.

Investors tend to see the economy as a chessboard and the politicians as those who move the pieces around. In many ways, the truth is the precise opposite. The economy calls the tune, and the politicians adjust their policies.

James Carville famously said, “I used to think that if there was reincarnation, I wanted to come back as the president or the pope or as a .400 baseball hitter. But now I would like to come back as the bond market. You can intimidate everybody.” Boy, is that right.

Indeed, there many times when investors can serve as the veto of last resort. In the end, currency markets get a vote.

Here’s part of what I wrote:

I should explain that Milei isn’t exactly your typical presidential candidate. Milei isn’t merely a small-government conservative; he’s a full-throated anarcho-capitalist. Two of his dogs are named Milton and Murray, in honor of Friedman and Rothbard.

I don’t want to give you the impression that Milei is somehow odd or unusual. For example, he wants to legalize the selling of organs and children. He also refuses to comb his hair. Additionally, he’s a tantric sex instructor. After that, things frankly start to get a little odd.

Now he’s president. Yes, Milei is zany but that’s part of his charm. The real story is that the economy is Argentina is a disaster. Inflation is running at 138%, and the country is on the brink of its sixth recession in the last decade.

People are frustrated and they want something done, even if it’s dramatic. In the U.S., we were alarmed about 9% inflation. Here’s a look at the inflation rate in Argentina.

This means prices double in less than a year.

One of Milei’s bolder plans is “dollarization.” He wants to ditch the Argentine peso and use the U.S. dollar. Other countries like Panama and Ecuador have tried this, but no one as big as Argentina has given it a shot.

The Argentine peso is governed by strict capital controls. There’s the official rate which is around 350 pesos to the dollar; then there’s the real rate. It never seems to occur to policymakers that their currency can be, and is, traded outside their country. The unofficial price for the peso is about one-third the official price.

For a land of such beauty and promise, Argentina seems to go from one self-induced crisis to the next. Forty percent of the people live in poverty. Yet it’s that frustration that’s driving Milei’s popularity. Milei said he wants to cut taxes and implement large spending cuts.

Did I mention that he cloned his dog? Yep, he did that too.

I’m not sure that the people of Argentina have embraced Milei’s strong views. Perhaps they have, but the truth is that things are so bad that voters are willing to give politicians outside the mainstream a hearing. Of course, we’ve had similar outcomes in our elections.

The problem with replacing the peso with the dollar is that Argentina simply doesn’t have enough dollars. They need outside investors and lots of them. Argentina could go to the IMF, but they’re already the IMF’s largest borrower.

Bond markets have been notoriously troublesome for some politicians. In 1981, Francois Mitterrand won a stunning Socialist victory. A lot of French money quickly found a new home in New York. Eventually, Mitterrand reversed course on his more radical policies.

Liz Truss faced a similar crisis last year, leading her to resign after just seven weeks as U.K. Prime Minister.

A Milei presidency could have a major impact on global commodity markets. Argentina is famous for its beef, but it’s also the world’s fastest-growing lithium producer. Milei has promised to take the axe to farm taxes. That could make Argentina’s agricultural sector more competitive. The country also has major deposits of copper and shale oil.

For now, the markets love Milei. In yesterday’s trading, shares of Argentina-based stocks soared on U.S. markets. There are 15 Argentine stocks that trade in the U.S. Most of the companies are financial or energy stocks, with a few utilities. Shares of Telecom Argentina (TEO) were up 22% yesterday, and they gained another 10% today. YPF Sociedad Anónima (YPF), a large energy company, jumped 40% yesterday. Check out the recent performance of the Argentina ETF (ARGT):

I’m skeptical Milei will get much of his program passed. Bureaucracies are hard to change. Still, it’s another indication that voters aren’t happy with high inflation and corruption. In the end, Milei will be able to go as far as the bond and currency markets let him.

The Fed Says It’s Not Looking to Cut Rates

This afternoon, the Federal Reserve released the minutes from its most-recent FOMC meeting (October 31 to November 1). Today’s minutes show that the Fed is in no hurry to cut rates. While inflation has been much better behaved, it’s still above the Fed’s target rate of 2%.

The Fed is not fully convinced that the battle against inflation has been won. That’s probably correct. During the 1970s, inflation came back again and again, worse each time. The Fed wants to avoid that.

The Fed is saying that policy should remain “restrictive” until it’s clear that inflation is headed back to 2%.

From today’s minutes:

In discussing the policy outlook, participants continued to judge that it was critical that the stance of monetary policy be kept sufficiently restrictive to return inflation to the Committee’s 2 percent objective over time.

All participants agreed that the Committee was in a position to proceed carefully and that policy decisions at every meeting would continue to be based on the totality of incoming information and its implications for the economic outlook as well as the balance of risks.

Participants noted that further tightening of monetary policy would be appropriate if incoming information indicated that progress toward the Committee’s inflation objective was insufficient.

Translated from Fedspeak, this is simply the Fed trying to sound tough. That’s quite different from making an actual tough-minded policy decision.

The markets continue to believe strongly that the Fed is done hiking rates. Odds of a rate hike at the December FOMC meeting are currently at 5%. For March, traders see a 28% chance of a Fed cut.

That’s interesting because at his last news conference, Jerome Powell said the Fed isn’t even talking about rate cuts. For May, the rate-cut odds rise to 59%, and by Election Day, traders expect to see three rate cuts.

We’re now witnessing a growing gap between what the Fed is saying, and what the public believes. When in doubt, I have greater confidence in the market’s opinion.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want more info on our ETF, you can check out the ETF’s website.

-

Morning News: November 21, 2023

Eddy Elfenbein, November 21st, 2023 at 7:05 amFor Argentina, Dollarization May Work Better on YouTube Than in Reality

South African Inflation Breakevens Tumble as Rates Seen on Hold

Russian Agricultural Bank Files Lawsuit Against JP Morgan

Bond Managers of $2.5 Trillion Make Case for Leaving Cash Behind

Is the US Headed for a Recession? Look at What Richer Americans Do on Black Friday

New ETF Tracks Developers of Obesity Drugs Amid Ozempic Hype

The Great Disconnect: Why Voters Feel One Way About the Economy but Act Differently

Higher Interest Rates Are Shattering Housing Dreams Around the World

October Home Sales Likely Fell to New 13-Year Low

Houses Too Expensive to Buy Underpin Lofty Rents

China Property Stocks Surge After Beijing Picks 50 Firms to Fund

US Is Seeking More than $4 Billion From Binance to End Case

A New Front Is Opening Up in the US-China Conflict Over Chips

How Microsoft’s Satya Nadella Kept the ‘Best Bromance in Tech’ Alive

OpenAI in ‘Intense Discussions’ to Quell Potential Staff Mutiny

The Long Shadow of Steve Jobs Looms Over the Turmoil at OpenAI

India Closer to Agreement With Tesla to Import EVs, Set Up Plant

GM’s Driverless Taxis Need to Slow Down

Wyndham Rebuffs Latest Takeover Attempt From Choice Hotels

How a Billionaire Banker Is Helping Elite US Colleges Recruit New Talent

A Descendant of Freed Slaves, Financier Pursues Family’s $900 Million Oil Claim

Soon You May Know Exactly Where Your Diamond Was Mined

Be sure to follow me on Twitter.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His