-

Econ Nobel Goes to Two Americans

Posted by Eddy Elfenbein on October 12th, 2009 at 11:05 amCongratulations to Elinor Ostrom and Oliver E. Williamson.

The prize committee cited Elinor Ostrom of Indiana University “for her analysis of economic governance, especially the commons,” and Oliver E. Williamson of the University of California, Berkeley, “for his analysis of economic governance, especially the boundaries of the firm.”

Ms. Ostrom becomes the first woman to win the prize for economics. Her background is in political science, not economics.

“It is part of the merging of the social sciences,” Robert Shiller, an economist at Yale, said of Monday’s awards. “Economics has been too isolated and these awards today are a sign of the greater enlightenment going around. We were too stuck on efficient markets and it was derailing our thinking.”

The prize committee, in making the awards, seemed to be influenced by the credit crisis and the severe recession that in the minds of many mainstream economists has highlighted the shortcomings of a unregulated marketplace, in which “economic actors,” left to their own devices, will act in their own self-interests and in doing so, will enhance everyone’s well-being.

The committee, in effect, said that theory was too simplistic and ignored the unstated relationships and behaviors that develop among companies that are competitors but find ways to resolve common problems. “Both scholars have greatly enhanced our understanding of non-market institutions” other than government, the committee said.

“Basically there is a common understanding that develops even among competitors when they are dealing with each other,” Mr. Shiller said, adding “when people make business contact, even competitors, they can’t anticipate everything, so an element of trust comes in.”

That is what the Nobel committee recognized, he said, in citing Mr. Williamson and Ms. Ostrom. -

The Market Is Not Overvalued

Posted by Eddy Elfenbein on October 9th, 2009 at 10:45 amJoe Weisenthal notes David Rosenberg’s comments that the stock market is overvalued. I’m sorry, I just don’t see how you can argue against this market on a valuation basis. Could there be a double-dip? Sure, that’s a risk and I can’t say how large. But the idea that the market is not only high, but dangerously high, makes no sense to me.

Rosenberg writes:While we will not belabour the point, when all the write-downs are included, the trailing P/E on “reported” earnings just widened to its highest levels in recorded history of nearly 140x (see chart below), which is three times the levels prevailing during the height of the tech bubble.

Yes, but that’s extremely depressed trailing earnings. When the economy tanks like that, these metrics lose some of their usefulness. Also, whenever the stock market initially spikes, it’s common for the P/E Ratio to rise since stocks are going up while earnings are still going down.

Rosenberg notes this criticism and compares today’s valuations to previous depressed earnings environments. Still, outside the great depression, the historic comparisons aren’t in the ballpark. Once we get Q4 2008 off our backs, then things will start to look like normal and we can again use traditional metrics again.

Another fact that the valuation argument must address is the low interest rates. As interest rates go down, valuations tend to rise in order to be competitive so I would expect higher multiples.

Rosenberg rightly notes that relying on future earnings is tricky since these are rarely correct. That’s true, but this is a crucial point and it goes back to my disagreements with Nassim Taleb. The forecasts and models don’t need to be perfect. They simply need to be reasonable.

In making a valuation judgment we need to make reasonable assumptions. For example, I recently said that corporate profits are likely to grow faster than the economy for the next few quarters (say three year).

Here’s a look at corporate profits’ share of GDP.

As you can see, it looks to be below trend. Note that I’m not predicting exactly where it will go, but based on past info, I’m making an assumption that profits will take up a larger share of the economy in near future.

This is why I believe the Street estimates of $92 earnings for the S&P 500 in 2011 are reasonable, which makes the market well priced, if not a little on the cheap side. -

Mortgage Rates in U.S. Fall to 4.87%

Posted by Eddy Elfenbein on October 9th, 2009 at 10:19 amMortgage rates for 30-year fixed U.S. home loans fell for the second consecutive week, pushing borrowing costs to near record lows.

The average U.S. 30-year rate dropped to 4.87 percent from 4.94 percent last week. The 15-year rate was 4.33 percent, mortgage buyer Freddie Mac of McLean, Virginia, said today in a statement.

Falling rates helped boost home-loan applications last week to the highest level since May. The Mortgage Bankers Association’s index of applications to purchase a home or refinance rose 16 percent. Rates around 5 percent, slumping home prices and a government tax credit for first-time homebuyers are bolstering demand for housing. -

Obama Wins Nobel Peace

Posted by Eddy Elfenbein on October 9th, 2009 at 9:25 amCongratulations to President Obama on winning the Nobel Peace Prize. Strangely, this comes on the same day that we bombed the Moon.

My guess is that he won’t win the prize in economics. (By the way, here are the odds for that.) -

Economics Fail: Forbes Edition

Posted by Eddy Elfenbein on October 8th, 2009 at 7:37 amCongratulations Forbes, you’re today’s winner of our economic illiteracy prize! Boy, this one is a doozy. They ran a remarkably silly article titled Countries Billionaires Could Buy. Here’s a typical brain-hurting passage:

Castles in France. Islands in the Caribbean. Private jets. With a collective $1.27 trillion at their disposal, the members of The Forbes 400 could buy almost anything.

How about a country? A quick glance at the CIA Fact Book suggests the individual fortunes of many Forbes 400 members are as big as some of the world’s economies.

Bill Gates, America’s richest man with a net worth of $50 billion, has a personal balance sheet larger than the gross domestic product (GDP) of 140 countries, including Costa Rica, El Salvador, Bolivia and Uruguay. The Microsoft visionary’s nest egg is just short of the GDP of Tanzania and Burma.Yes, they’re confusing net worth with GDP.

Ok class, turn to page 208 of N. Gregory Mankiw’s Principle of Macroeconomics for a definition of gross domestic product:Gross domestic product (GDP) is the market value of all final goods and services produced within a country in a given period of time.

In other words, net worth = stuff you have; GDP = stuff you make. It’s like confusing the price of the stock with its earnings.

The net worth of a country is far larger than what it produces in a single year. Not only is Costa Rica wealthier than Bill Gates, it’s a lot wealthier. Furthermore, the comparison between a western billionaire to a developing country is heavily skewed due to the Penn Effect. -

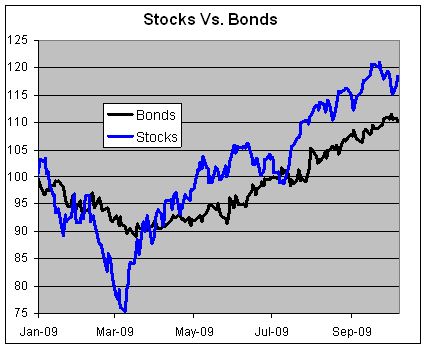

Stocks Vs. Bonds—Another Look

Posted by Eddy Elfenbein on October 7th, 2009 at 1:58 pmOne very simple way of looking at the stock market’s valuation is to compare it with how well long-term bonds have been doing. Over the long haul, stocks have outperformed bonds by a bit but that fact has been thrown into disarray this decade. Since the market peaked in March 2000, bonds have pummeled stocks. In fact, bonds have beaten stocks so badly that they’ve erased the entire lead accumulated over the past 40 years.

Here’s the fact that surprised me. While stocks have rallied since March, the rally when compared with bonds was dramatic but short. Stocks only beat bonds from March 5 to May 8 (I’m using VFINX for my stock proxy and VWESX for my long-term corporate bond proxy). Since May 8, bonds have slightly beaten stocks plus they’re far less volatile.

-

Ken Lewis Resigns

Posted by Eddy Elfenbein on October 7th, 2009 at 11:45 amThe Onion takes a closer look:

Once heralded as a shrewd innovator, embattled CEO Ken Lewis is now leaving Bank Of America. Here are some key missteps from the past 18 months that have cast a pall over his tenure:

* Thought bank had so much more money than it actually did

* Accidentally set the Canton, OH branch on fire during a visit

* Mailed out millions of checks that incorrectly read “Bank of Armenia”

* Problems involving banks, America

* Caught placing cameras in Bank of America’s women’s locker room

* Bank of America cash registers consistently $10 short on his shift

* Idea to have ATMs beep incessantly has driven away tens of thousands of irritated customers

* Worldwide economic collapse -

Moron Attacks Peter Schiff

Posted by Eddy Elfenbein on October 6th, 2009 at 11:27 pmI’ve had my disagreements with Peter Schiff but this attack on him is just plain silly.

-

Carney Vs. Taibbi

Posted by Eddy Elfenbein on October 6th, 2009 at 10:43 amThere’s a nice little blog war going on between Matt Taibbi and John Carney over naked short selling, and Carney is mopping the floor with him.

Taibbi posted a video which he claimed show a trader placing a naked short sale. Well, not a short sale exactly but a locate. And this proves that naked shorting is fraudulent because, well, I don’t get that part.

The only point that I see is that the software the trader uses isn’t worth a damn. It claims to have instantly found a bazillion shares of Citi. Taibbi claims it’s Penson though that’s not the case.

Carney writes:Importantly, this trade would have to be put through some broker who would have the responsibility to check whether the shares could reasonably be located in the amount requested. The speed with which this transaction takes place implies that it is a fully automated system that processes trades that would then have to be passed on to an actual back-office at a brokerage where much a much slower review would take place. And at the brokerage, putting aside an egregious human error (which is always possible), the trade would have been rejected.

As I see it, this is like posting a video of guys wearing ski masks standing outside a bank and claiming it’s a video of a hold-up. No, I mean it could be a video of a hold-up. Impressed? Me neither.

More from Kid Dynamite:Daily, traders and brokers will obtain a list of easy to borrow stocks, which get loaded into their trading system. If you go to short GE, it’s on the “easy to borrow list,” and as long as you don’t try to short 10,000,000,000 shares, you won’t have to call your stock loan department to “borrow” shares to short – everyone knows the stock is readily available. Other stocks, however, like Citi (which is almost certainly the stock in Taibbi’s video) can at times be difficult to borrow – like during the summer when they were doing an exchange of preferred stock for common stock, and everyone wanted to be short the common (and long the preferred) to arbitrage the spread between the two share classes.

So, if you try to short Citibank (a few months ago), any good execution system will check its easy to borrow list, see that Citi is not on the list, and ask you where your “locate” is from – in other words, which broker agreed to lend you the stock. There are also many electronic systems where you can request a stock locate electronically – but this is not what’s in Taibbi’s video! What the video clearly shows is that the stock in question (let’s call it C) is on the hard to borrow list. The trader gets a warning message saying that the stock needs to be borrowed, and asking for the trader to either submit the borrow information or elect not to submit the trade.

The trader in the video is NOT submitting a request for the stock to be borrowed – he’s entering information into an audit trail point asking WHO the stock was borrowed from, HOW MUCH was borrowed, and WHEN it was borrowed – exactly to prevent problems related to naked short selling! This way, if the seller fails to deliver shares, the broker can easily pull the exact reference that was used for the short sale. Of course, just because I say that I was able to obtain a locate for a gajillion shares of C doesn’t mean that I actually was able to – and that’s why especially hard to borrow stocks should have another level of compliance checking embedded in them. If this trading system in the video allowed a trader to claim a locate that was clearly impossible, then that’s a condemnation of the inadequacy of this trading system – not of the borrow market and the legitimacy of short selling. Fortunately, there was no naked short sale of tens of billions of shares of C on this trade, and Taibbi’s post is a gigantic misunderstanding of what was actually going on. -

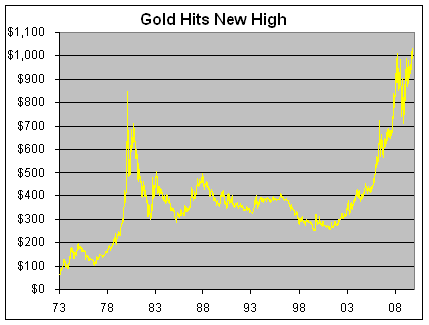

Gold Makes New All-Time High

Posted by Eddy Elfenbein on October 6th, 2009 at 10:16 amThe price of gold is up strongly today to nearly $1,040. Gold and the S&P 500 had been tracking each other, but the S&P took a big lead over the summer. Now it’s close again. The S&P 500 is only about 14-15 points above gold.

In March 2008, gold reached a peak over $1,000 an ounce but it pulled back to nearly $700 by November. Since then, the price of gold has gradually climbed higher.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His