-

“It beats the heck out of any certificate of deposit”

Posted by Eddy Elfenbein on August 19th, 2009 at 10:14 amWhere are some investors placing their money?

Tax liens.Private investors step in and buy tax liens, paying governments upfront all or part of the value of the taxes. The investors then get the right to foreclose on the properties, taking priority over mortgage lenders, and to charge interest rates as high as 18 percent on the unpaid taxes.

“It beats the heck out of any certificate of deposit,” said Howard Liggett, executive director of the National Tax Lien Association.

Because the sales occur in a patchwork of cities and counties across more than two dozen states, there are no figures tracking the number of tax-lien sales nationwide. The liens that are sold come from cases in which homeowners pay taxes to the local government, not through their lenders. But Mr. Liggett, whose group represents tax-lien investors, said they generated about $10 billion every year.

In 2006, Lucas County began selling off its overdue tax certificates to a New Jersey company named Plymouth Park Tax Services, a subsidiary of JPMorgan Chase. It also operates under the name Xspand.

The company, once run by the former governor of New Jersey, James J. Florio, was sold to Bear Stearns and then absorbed into JPMorgan after Bear’s collapse last year. Today, Plymouth Park is one of the largest players in the tax-lien business.

Plymouth Park has filed more than 1,000 foreclosure actions against delinquent taxpayers, more than any single mortgage lender in the county. But it says that it has only foreclosed on 56 of those filings. -

Eaton Vance’s Earnings Fall But Top Expectations

Posted by Eddy Elfenbein on August 19th, 2009 at 9:57 amIt’s still been a good year for the asset management stocks. Eaton Vance (EV) is up over 40% for us. Reuters reports:

Asset manager Eaton Vance Corp said fiscal third-quarter net income fell 37 percent compared with a year ago as fees decreased.

For the three months that ended July 31, Boston-based Eaton Vance reported net income of $31.2 million, or 26 cents per share, down from $49.6 million, or 40 cents a share in the same period a year ago. Revenue fell 19 percent to $228 million.

Analysts surveyed by Thomson Reuters on average had expected the company to earn 28 cents per share, and revenue of $224.5 million for the quarter.

Revenue and net income rose compared with the quarter that ended April 30, 2009, however, as did assets under management. Eaton Vance managed $143.7 billion in assets as of July 31, up from $127.2 billion in the previous quarter. The increases were similar to those at other asset managers that have benefited from rising stock markets. -

Investor Quiz

Posted by Eddy Elfenbein on August 18th, 2009 at 2:46 pmGuess what company went from concept to $1 billion in sales in three years?

-

How Bad Is Inflation in Zimbabwe?

Posted by Eddy Elfenbein on August 18th, 2009 at 2:39 pmAt one point last year, prices were doubling.

Every day. -

RIP: Rose Friedman

Posted by Eddy Elfenbein on August 18th, 2009 at 1:19 pmRose Friedman passed away yesterday at the age of 98.

“The only person known to have ever won an argument with Milton.” – President George W. Bush

-

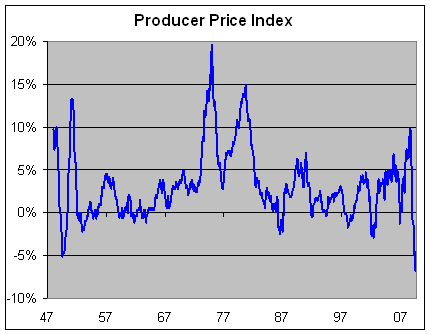

PPI Is Lowest on Record

Posted by Eddy Elfenbein on August 18th, 2009 at 10:35 amToday’s PPI report shows that wholesale prices have dropped by 6.8% over the last year. That’s the lowest on record.

So is deflation a threat? Matthew Lynn says that fears of deflation are vastly overblown.In other words, there were plenty of deflationary years. Yet over that period, the U.K. became the greatest economic power in the world: Its relative decline only started once inflation took hold. Deflation didn’t stop the Industrial Revolution, one of the most sustained times of economic creativity ever seen.

Likewise, a 2004 study by the Federal Reserve Bank of Minneapolis looked at the data on deflation across 17 countries over 100 years. It found that although the Great Depression of the 1930s was linked with falling prices, that wasn’t true of any other historical period. There was, it said, “virtually no evidence” that deflation caused a depression.

Why should it? We are constantly told that deflation is bad because it makes consumers hold off from buying things, thinking they will be cheaper tomorrow. But that is just silly. -

The Biggest Thing Since E-mail

Posted by Eddy Elfenbein on August 18th, 2009 at 10:17 amJim Cramer pounds the table for Smart Phones:

As big and as game-changing as the personal computer and the Internet were, I believe the mobile Internet—the integration of voice, data, video, and storage in one handheld device—will be more lucrative than both. Maybe both put together. That may sound far-fetched now, but these devices, chock-full of applications and hardware that have begun to rival those of personal computers, have finally realized the elusive holy grail. As any twentysomething, or even middle-schooler, knows, once you procure a smartphone, you can throw away pretty much every publication, every guide, every television, every camera, every music device, heck, every gizmo you have, save your toaster oven. You just don’t need ’em anymore.

It’s not just the dazzling technology that’s driving things. It’s the size of the market and the speed at which companies and consumers are getting onboard. It took a half-dozen years and a host of competitors like Dell, Gateway, and Compaq to produce personal computers cheap enough to entice the masses. Thanks to the substantial subsidies offered by Verizon, Sprint, AT&T, and T-Mobile in their endless battles for market share, Americans are buying up smartphones and calling plans much faster than they bought PCs.

And the U.S. market is tiny versus the overseas arena. Beijing alone just committed $40 billion to build a smartphone network that will cover the whole nation, and the big telephone companies in China plan on subsidizing the phones with the same zeal as the American firms—obviously with millions more customers. Currently, there are as many as 4 billion cell-phone users worldwide, but only 12 percent use smartphones. Given the superiority of the product and the aggressive pricing, I expect we will see a total replacement of dumb phones with smart ones rather quickly. You’re talking about a market that could grow eightfold in just a few years. -

The 10 stupidest tech company blunders

Posted by Eddy Elfenbein on August 18th, 2009 at 9:52 amInfoWorld runs down the 10 stupidest blunders from tech companies. Here’s a sample and it’s one I never knew about:

2. Real Networks Punts on the iPod

People think Steve Jobs invented the iPod. He didn’t, of course. Jobs merely said yes to engineer Tony Fadell after the folks at Real Networks rejected Fadell’s idea for a new kind of music player in the fall of 2000. (Fadell’s former employer Philips also turned him down.)

By then MP3 players had been around for years, but Fadell’s concept was slightly different: smaller, sleeker, and focused on a content-delivery system that would give music lovers an easy way to fill up their “pods.” (Jobs is famous for driving the design of the iPod.)

Today that content-delivery system is known as iTunes, and Apple controls some 80 percent of the digital music market. Fadell worked at, and eventually ran, Apple’s iPod division until November 2008. Real Networks is still a player in the streaming-media world, but its revenues are a fraction of what Apple makes from iTunes alone.Um…sorry.

-

S&P 500 Stocks Above Pre-Lehman Levels

Posted by Eddy Elfenbein on August 18th, 2009 at 9:41 amBespoke finds the very small list of stocks that are above their level prior to Lehman Brothers going kablooey. Only 55 stocks are up and just 27 are up by more than 10%.

-

Insiders Are Dumping Stock

Posted by Eddy Elfenbein on August 18th, 2009 at 8:51 amFrom Reuters:

A massive rally in U.S. stocks since March has reawakened bullish spirits, but insiders are jumping out of the market in a sign the run up is getting stretched.

Company executives are selling stock at a rate not seen in two years after a near 50 percent rise in the S&P 500 from a March 9 low. That suggests directors and managers may think stock prices are nearing the top end of their range in the current economic climate.

There has been a decline in short interest — borrowed shares sold but not yet repurchased — which some analysts see as a warning. Some investors sell short to profit from price declines, and some say the recent rally has been supported by the reversing of short positions.After a 50% rally, I think a sharp pullback is necessary. When it will happen and by how much is still a question. However, I don’t think the market really experienced a rally as much as we saw an unwinding of a vicious bear market.

The rally has been led by junk stocks which is really due to investors fleeing all investments which held any type of risk. The low-quality rally is mirrored by what’s been happening in the bond market with the closing of the gigantic spreads between corporates and Treasuries.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His