-

Baxter and Amphenol’s Earnings

Posted by Eddy Elfenbein on July 16th, 2009 at 11:25 amWe had two earnings reports this morning from our Buy List stocks, and so far, the results seem to be canceling each other out. Amphenol’s loss is wiping out Baxter’s gain.

Amphenol (APH) reported earnings of 43 cents a share which beat the Street by a penny a share. In April, APH said to expect earnings between 41 cents and 43 cents a share, so this isn’t much of a surprise. But it’s a big drop from the 61 cents a share they made last year.

The company sees Q3 earnings coming in—same as Q2—between 41 cents and 43 cents a share, which is below the Street’s view of 44 cents. Amphenol is a good stock but not a great buy right now.

Baxter International (BAX) earned 96 cents a share which was two cents more than expectations, and one penny more than the high end of the range they provided in April. For Q3, they said to expect earnings between 95 cents and 97 cents a share (btw, I like companies with that kind of precise guidance). Last year’s Q2 came in at 85 cents a share.

They slightly raised their full-year EPS guidance to a range of $3.76 to $3.80 from the previous range of $3.72 to $3.78. They had also raised guidance in April as well, so this is good to see.

I like this stock but I’d like it more at $45. -

Let’s Try a Small Thought Experiment

Posted by Eddy Elfenbein on July 16th, 2009 at 10:14 amThe stock market is up again and I’m outraged!! The market closed yesterday just 1.5% below our June 12th high, and we’re up about 38% from the March low.

How could so many market gurus lead us astray!

Shiller, Taleb, Schiff, Roubini. They all FAILED to see this horrible bull rally that has crippled MILLIONS AND MILLIONS of shorts.

Congress needs to investigate! I want to see people go to JAIL!

In the spirit of Jon Stewart, don’t they know that investing isn’t a game???

Think of all the children of shorts who now go hungry every night. Think of the shorts who have seen their retirement savings get ransacked by this cruel bull market. Think of all those investors who now can only afford a BMW 328 i? It makes me sick!

Let’s start compiling a list of VILLAINS who are responsible for this rally!

I can’t wait to Matt Taibbi take these frauds down!

I DEMAND that Shiller, Taleb, Schiff and Roubini go on Jon Stewart’s show and GROVEL, and say that they’ll try to do a better job in the future. These people need to be publicly HUMILIATED!

They have NO SHAME.

I DEMAND that left-wing groups start a petition asking CNBC to BAN everyone who missed this cruel and vicious rally. -

Prominent Economists: Leave the Fed Alone

Posted by Eddy Elfenbein on July 15th, 2009 at 2:48 pmHere’s a petition that’s been signed by a slew of well-known economists (you can see the names at the link):

Amidst the debate over systemic regulation, the independence of U.S. monetary policy is at risk. We urge Congress and the Executive Branch to reaffirm their support for and defend the independence of the Federal Reserve System as a foundation of U.S. economic stability. There are three specific risks that must be contained.

First, central bank independence has been shown to be essential for controlling inflation. Sooner or later, the Fed will have to scale back its current unprecedented monetary accommodation. When the Federal Reserve judges it time to begin tightening monetary conditions, it must be allowed to do so without interference. Second, lender of last resort decisions should not be politicized.

Finally, calls to alter the structure or personnel selection of the Federal Reserve System easily could backfire by raising inflation expectations and borrowing costs and dimming prospects for recovery. The democratic legitimacy of the Federal Reserve System is well established by its legal mandate and by the existing appointments process. Frequent communication with the public and testimony before Congress ensure Fed accountability.

If the Federal Reserve is given new responsibilities every effort must be made to avoid compromising its ability to manage monetary policy as it sees fit.Earlier this week, my in-box was crammed full of morons who insisted in perpetuating the lie that the Federal Reserve is a private bank. However, I’ve never fully understood the sacredness of central bank independence. Why is this some great ideal? The Fed is a dependency of Congress and I don’t see what’s wrong with treating it that way.

Can anyone point to an instance of where Fed independence turned out to be helpful? Perhaps the early 1980s but I highly doubt Paul Volcker would have intimated by anyone. The Fed doesn’t need to be independent. It does need to have latitude and flexibility within a framework of Congressional oversight. If the Fed fails to do its job well, that’s a political issue and politicians should be held accountable.

The function of the Fed has changed a lot in the past year and I think it’s reasonable to revisit some core assumptions. Questioning the Fed’s independence is a good start. -

Used Car Prices Up in June

Posted by Eddy Elfenbein on July 15th, 2009 at 1:51 pmToday’s CPI report showed that “used cars and trucks” rose nearly 1.4% last month. That’s not seasonally adjusted. This might be evidence that used cars are doing well which may say something about Nicholas Financial (NICK). It’s a small bit of news, but worth passing on.

By the way, NICK just posted their latest annual report. The stock is still going for less than two-thirds of its book value. -

Carney Defends Capitalism

Posted by Eddy Elfenbein on July 15th, 2009 at 1:32 pmJohn is spot on. CIT really made a mistake in not failing earlier and more massively. Oh well.

-

Lap Dances Apparently Not Hurt By Recession

Posted by Eddy Elfenbein on July 15th, 2009 at 12:06 pmGuess what strip club stock is 200% in the last four months?

Rick’s Cabaret International (RICK)

Special bonus! Hear Erin Burnett make a reference to Mark Haines’ ass. It’s not business, it’s CNBC.

-

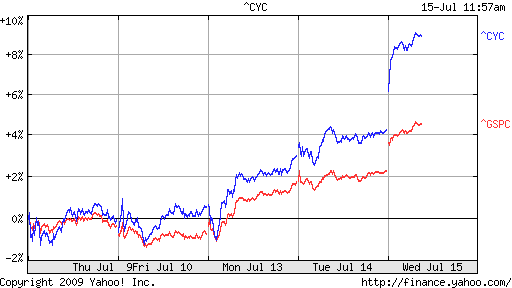

Today’s Rally Is Led by the Cyclicals

Posted by Eddy Elfenbein on July 15th, 2009 at 11:57 amIt’s all about the cyclicals:

-

The Puzzling Equity Premium Puzzle

Posted by Eddy Elfenbein on July 15th, 2009 at 10:28 amDavid Merkel has some interesting thoughts on the Equity Premium Puzzle.

My so-far-ignored-by-the-Noble committee idea is that there is and should be an premium for equities, but it shouldn’t be very much. The idea is simple: If you lend a company money, both you and the company implicitly agree that they can do better with it than you. Therefore, their ROE ought to top the interest rate on the loan.

A bond can’t buy a stock, but a stock can buy a bond. Moreover, a stock can use leverage to buy even more bonds. Therefore the size of the equity premium ought to be related to the size of the yield curve. What exactly the relationship is…well, I haven’t worked that part out yet. -

Stat of the Day

Posted by Eddy Elfenbein on July 14th, 2009 at 3:41 pmGeneral Motors, days in bankruptcy = 39

Jesus, days in wilderness = 40

(Source: Bloomberg, KJV) -

Daniel Gross: The Recession is Over (Sorta)

Posted by Eddy Elfenbein on July 14th, 2009 at 3:13 pmAt the new-and-improved Newsweek, Daniel Gross hops on the Dennis Kneale bandwagon and declares the recession over — though he has a far more intelligent and sardonic analysis:

(T)wo of the best and most objective forecasters, who are not connected to investment banks or to the CNBC noise machine, have recently called the upturn. Macroeconomic Advisers, the St. Louis-based consulting firm that compiles a monthly GDP index, reported to its clients Monday that while second-quarter GDP was tracking at negative 0.1 percent (recession), the third quarter was tracking at 2.4 percent growth.

The folks at the Economic Cycles Research Institute agree enthusiastically. It’s not because they’ve detected green pea shoots in Central Park. Rather, it’s because we’ve seen the three P’s, says Laskhman Achuthan, managing director at ECRI, which has been studying business cycles for decades and was one of the few outfits to call the last two recessions with any degree of accuracy.

The economic data that get the most play in the news—unemployment, retail sales—are coincident or lagging indicators and historically have not revealed much about directional changes in the economy. ECRI’s proprietary methodology breaks down indicators into a long-leading index, a weekly leading index, and a short-leading index. “We watch for turning points in the leading indexes to anticipate turning points in the business cycle and the overall economy,” says Achuthan. It’s tough to recognize transitions objectively “because so often our hopes and fears can get in the way.” To prevent exuberance and despair from clouding vision, ECRI looks for the three P’s: a pronounced rise in the leading indicators; one that persists for at least three months; and one that’s pervasive, meaning a majority of indicators are moving in the same direction.

The long-leading index—which goes back to the 1920s and doesn’t include stock prices but does include measures related to credit, housing, productivity, and profits—hits bottom and starts to climb about six months before a recession ends. The weekly leading index calls directional shifts about three to four months in advance. And the short-leading index, which includes stock prices and jobless claims, is typically the last to turn up.

All three are now flashing green. According to Achuthan, the long-leading index growth rate has been recovering since November 2008, the weekly leading index has been recovering since last December, and the short-leading index growth rate bottomed in February 2009. In sequence, each turned up, “and by April the three Ps had all been satisfied.” Sure, corporate profits continue to disappoint, and the unemployment rate is climbing. But for ECRI, which navigates by relying exclusively on its instruments, that’s only a part of their picture. They’re the Spocks of the economic forecasting crowd—unemotional, uninvested in anything but the logic of what history and their dashboard tell them. “From our vantage point, every week and every month our call is getting stronger, not weaker, including over the last few weeks,” says Achuthan. “The recession is ending somewhere this summer.” In fact, it may already be over.Hmmm…I hope he’s right but hope isn’t a good research tool. The fact is that the economy still faces a number of headwinds, the most crucial is the deleveraging that’s going on. My fear is that we’re in for a prolonged period of sluggish growth.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His