-

Fans Flock to Mourn California, 1849-2009

Posted by Eddy Elfenbein on July 10th, 2009 at 1:47 pmIowahawk is on the scene:

From a humble beginning as a water-poor remote Spanish mission outpost, California proved to be a precocious and talented child performer. It struck gold with ‘Sutter’s Mill’ in 1849, earning accolades and attracting millions of crusty bearded prospectors. Black gold soon followed with ‘Arizona.’ Unlike many child acts, California made a smooth transition to adolescence, scoring a major hit with ‘Agriculture’ in 1891.

Even a frightening bout with tremors did not stop the flow of hits. The 1915 megasmash ‘Hollywood’ broke all records, as did the wartime favorite ‘Aerospace.’ More recently, California topped the charts with ‘Tourism,’ ‘High Tech,’ and ‘Coastal Pretension.’

For a time it seemed as if the superstar could do no wrong, but behind the glittering facade of Disneyland Manor troubling signs of mental instability began to emerge. The state developed a well-publicized drug problem during filming of 1967’s ‘Summer of Love,’ and briefly dabbled in strange religious cults. Under the influence of spiritual guru Jerry Brown, it began wholesale experimentation in exotic spending programs, eventual resulting in a traumatic 1979 stay at the Prop 13 Rehab Center.

During the 80’s and 90’s California enjoyed a brief career renaissance with hits like ‘Olympics,’ ‘Real Estate’ and ‘Dot Com Boom,’ but personal problems plagued the reclusive star once again. During the recording of the ‘OJ’ and ‘Rodney King’ albums, friends and visitors expressed concern over its recurring tremors and penchant for self-mutilation.

“California used to be so happy and beautiful,” said a horrified Ohio. “I hardly recognize it any more.”

During that period, camp insiders say the increasingly psychotic state began driving away its long time professional management team and support crew. In its place, it assembled an entourage of con men and embezzlers, some of who stoked California’s increasingly bizarre environmental paranoia. It was seldom seen in public without a breathing mask to ward off imagined pollutants.

Worse, the hits began drying up; the huge 2001 flop ‘Dot Com Bust’ put a huge crimp into California’s once unlimited cash flow. Despite the setback, insiders say the superstar was unwilling to change its lavish lifestyle, and retreated once again into spending abuse. Personal expenses skyrocketed, propelled in part by California’s eight million adopted foster children. During the 90’s sensationalistic accounts of child abuse began surfacing. Eyewitnesses reported California cruising local neighborhoods in school buses, luring unsuspecting kid for sessions of ‘public education.’ By some estimates hundreds of thousands were left traumatized and severely brain damaged.Read the whole thing.

-

The Big Business of Overdraft Fees

Posted by Eddy Elfenbein on July 10th, 2009 at 11:05 amContrary to what you might think, banks love overdrafts. They’re happy to cover you then charge a hefty fee. This year banks will rake in close to $40 billion through overdraft fees. To put that in context, it’s about double what they’ll make off credit card penalties. If it weren’t for overdraft fees, nearly half of all banks and credit unions wouldn’t have made any money last year.

USA Today reports:Large banks also reserve the right to process large transactions first, triggering more overdraft fees by emptying the account more quickly. Some even charge consumers before they overdraw by deducting a purchase when it’s made, rather than when it clears, pushing the account into the red sooner.

There is a simple way for consumers to avoid all this—balance your freakin checkbook!

-

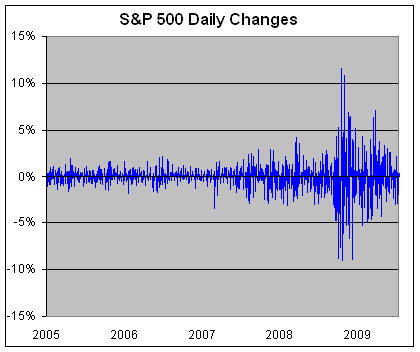

The Volatility Storm Has Passed

Posted by Eddy Elfenbein on July 10th, 2009 at 10:38 amWhat happened to all the volatility? Here are the closing S&P 500 levels for Tuesday, Wednesday and Thursday—881.03, 879.56 and 882.68. Snore!

Here’s a look at the S&P 500’s daily changes going back to 2005.

Right now we’re at 881.38. This market is flat! -

CNBC Follows Up Its Special Report on Weed with One on Hookers and Another on Porn. Trend?

Posted by Eddy Elfenbein on July 10th, 2009 at 10:15 amIs it me or does there seem to be a trend with CNBC’s special reports? First David Faber did an excellent job with “Marijuana Inc: Inside America’s Pot Industry.” Tonight is the premiere of “Dirty Money: The Business of High-End Prostitution.” And next Wednesday, they air “Porn: Business of Pleasure.”

And they employ Dennis Kneale.

Don’t get wrong, I’m all for this vice stuff. But some of their sponsors aren’t too thrilled with the idea. Mediaite notes that Charles Schwab pulled it sponsorship of Fast Money—though not from CNBC entirely. -

Same-Stores Sales for June

Posted by Eddy Elfenbein on July 9th, 2009 at 3:18 pmHere are the mostly ugly totals for June:

DISCOUNT

BJ’s Wholesale Club -7.5 pct

Costco -6 pct

Target -6.2 pct

DEPARTMENT STORES

Bon-Ton Stores -8 pct

Dillard’s -14 pct

Fred’s 0.2 pct

J.C. Penney -8.2 pct

Kohl’s -5.6 pct

Neiman Marcus -20.8 pct

Nordstrom -10 pct

Macy’s -8.9 pct

Saks -4.4 pct

Stage Stores -12.6 pct

CLOTHING AND TEEN-ORIENTED

Abercrombie & Fitch -32 pct

Aeropostale 12 pct

American Apparel -13 pct

American Eagle Outfitters -11 pct

The Buckle 9.6 pct

Cato Corp. -3 pct

The Children’s Place Retail Stores -12 pct

Destination Maternity -10.7 pct

Gap Inc. -10 pct

Hot Topic -7.9 pct

Limited Brands -12 pct

Ross Stores 1 pct

Stein Mart -8 pct

TJX Cos. 4 pct

Wet Seal -11.1

Zumiez -19.3 pct

DRUG

Rite Aid Corp. -0.6 pct

Walgreen Co. 3.4 pct -

The Fed Strikes Back

Posted by Eddy Elfenbein on July 9th, 2009 at 1:49 pmDespite have a ton of cosponsors, Ron Paul’s bid to get a full audit of the Fed seems have died in the Senate. Vice Chairman Donald Kohn took on the issue today on Capitol Hill:

The Congress, however, has purposefully–and for good reason–excluded from the scope of potential GAO audits monetary policy deliberations and operations, including open market and discount window operations, and transactions with or for foreign central banks, foreign governments, and public international financing organizations. By excluding these areas, the Congress has carefully balanced the need for public accountability with the strong public policy benefits that flow from maintaining the independence of the central bank’s monetary policy functions and avoiding disruption to the nation’s foreign and international relationships.

The same public policy reasons that supported the creation of these exclusions in 1978 remain valid today. The Federal Reserve strongly believes that removing the statutory limits on GAO audits of monetary policy matters would be contrary to the public interest by tending to undermine the independence and efficacy of monetary policy in several ways. First, the GAO serves as the investigative arm of the Congress and, by law, must conduct an investigation and prepare a report whenever requested by the House or Senate or a committee with jurisdiction of either body. Through its investigations and audits, the GAO typically makes its own judgments about policy actions and the manner in which they are implemented, as well as recommendations to the audited agency and to the Congress for changes or future actions. Accordingly, financial markets likely would see the grant of audit authority with respect to monetary policy to the GAO as undermining monetary independence–with the adverse consequences discussed previously–particularly because GAO audits, or the threat of a GAO audit, could be used to try to influence monetary policy decisions.

Permitting GAO audits of monetary policy also could cast a chill on monetary policy deliberations through another channel. Although Federal Reserve officials regularly explain the rationale for their policy decisions in public venues, the process of vetting ideas and proposals, many of which are never incorporated into policy decisions, could suffer from the threat of public disclosure. If policymakers believed that GAO audits would result in published analyses of their policy discussions, they might be less willing to engage in the unfettered and wide-ranging internal debates that are essential to identifying the best possible policy options. Moreover, the publication of the results of GAO audits related to monetary policy actions and deliberations could complicate and interfere with the communication of the FOMC’s intentions regarding monetary policy to financial markets and the public more broadly. Households, firms, and financial market participants might be uncertain about the implications of the GAO’s findings for future decisions of the FOMC, thereby increasing market volatility and weakening the ability of monetary policy actions to achieve their desired effects.

These concerns extend to the policy decisions to implement the discount window and broadly available credit facilities. These facilities are extensions of our responsibility for promoting financial stability, maximum employment and price stability. Indeed, unlike the institution-specific loans that the Federal Reserve has made that now are subject to GAO audit, these broader market facilities are designed to unfreeze financial markets and lower interest rate spreads in concert with our other monetary policy actions. It is important that, like other monetary policy decisions, the Federal Reserve remain independent in making policy decisions regarding these facilities.

An additional concern is that permitting GAO audits of the broad liquidity facilities the Federal Reserve uses to affect credit conditions could reduce the effectiveness of these facilities in helping promote financial stability, maximum employment, and price stability. For example, even if strong confidentiality restrictions were established, individual banks might be more reluctant to borrow from the discount window if they knew that their identity and other sensitive information about their borrowings could be disclosed to the GAO. Rumors that a bank may have used the discount window can cause a damaging loss of confidence even to a fundamentally sound institution. Experience, including experience in the current financial crisis, shows that banks’ unwillingness to use the discount window can result in high and volatile short-term interest rates and limit the effectiveness of the discount window as a tool to enhance financial stability.

Overall, the Federal Reserve believes that removing the remaining statutory limits on GAO audits of monetary policy and discount window functions would tend to undermine public and investor confidence in monetary policy by raising concerns that monetary policy judgments in pursuit of our legislated objectives would become subject to political considerations. As a result, such an action would increase inflation fears and market interest rates and, ultimately, damage economic stability and job creation. -

Earnings Calendar

Posted by Eddy Elfenbein on July 9th, 2009 at 12:06 pmEarnings season is approaching and 13 of the 20 stocks on the Buy List have a quarter ending in June. Here’s a calendar of report dates. A few haven’t said when they’ll report so I’m estimating by what they’ve done in previous years:

Amphenol (APH) July 16

Baxter (BAX) July 16

Stryker (SYK) July 21

Eli Lilly (LLY) July 22

SEI Investments (SEIC) July 22 est

Danaher (DHR) July 23

Aflac (AFL) July 29

Fiserv (FISV) July 29

Becton, Dickinson (BDX) July 30

Nicholas Financial (NICK) July 30 est.

Moog (MOG-A) July 31 est.

Cognizant Technology Solutions (CTSH) August 5 est.

Sysco (SYY) August 6 est. -

Altria Is Still Cheap

Posted by Eddy Elfenbein on July 9th, 2009 at 11:03 amJust another quick note on Altria (MO). The stock is still very attractive at this price. MO is going for less than 10 times this year’s estimate. The dividend currently yields 7.8% and it could be raised soon. Earnings are due two weeks from yesterday.

-

Meep! Meep! Meep! Meep! Meep!

Posted by Eddy Elfenbein on July 8th, 2009 at 2:52 pmApparently, someone hurt Beaker’s feelings.

-

One From the Time Machine

Posted by Eddy Elfenbein on July 8th, 2009 at 1:17 pmLess than nine years ago:

President Clinton: The United States on Track to Pay Off the Debt by End of the Decade

Today, President Clinton will announce that The United States is on course to eliminate its public debt within the next decade. The Administration also announced that we are projected to pay down $237 billion in debt in 2001. Due in part to a strong economy and the President’s commitment to fiscal discipline, the federal fiscal condition has improved for an unprecedented nine consecutive years.Clinton wasn’t talking about balancing the budget or even reducing the debt, he meant paying off the debt. The only time the government has been debt free was in 1835 and 1836.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His