-

Good Story on DirectEdge

Posted by Eddy Elfenbein on June 3rd, 2009 at 4:43 pm -

Rep. Alan Grayson at Ritholtz-Palooza

Posted by Eddy Elfenbein on June 3rd, 2009 at 4:17 pmCongressman Alan Grayson had some interesting comments at Barry Ritholtz’s conference today:

Grayson appeared on a panel with Nassim Taleb, best known as the author of The Black Swan. Their exchange about the proper role of government regulation of the financial system was entertaining, if a bit meandering. Grayson, who grew up in the Bronx and holds three Harvard degrees, has a rare ability to say relatively radical things without coming off as a rabid populist. Moderator Barry Ritholtz, author of the just-published Bailout Nation, asked a straightforward question: The U.S. government does a reasonably good job of regulating things like the safety of airplanes and foods. Why, then, does it do such a lousy job of regulating the financial system?

Grayson’s answer was immediate and succinct: “Capture.” For those not up on regulatory theory, this refers to the notion that regulators become captive of the industries they regulate. Noting that Fannie Mae and Freddie Mac spent $100 million on campaign contributions over the last 10 years, Grayson said: “The system is in some sense corrupt. A senator said the other day that Wall Street owns Washington, and while I might not go that far, you don’t have the airlines ‘owning’ the [airline regulators]. There is a lot of influence that Wall Street has on the government, even the judicial branch.” Indeed, Grayson could have cited the front-page story in today’s Wall Street Journal, documenting the remarkable efficiency with which banking campaign contributions appear to have helped ease accounting rules that in turn helped the banks. -

Ode to Becky

Posted by Eddy Elfenbein on June 3rd, 2009 at 11:08 am

(HT: WSF) -

Oh Dear Lord

Posted by Eddy Elfenbein on June 3rd, 2009 at 11:01 amA fund for investing in lawsuits:

Richard W. Fields says he has come up with a win-win financial strategy for the downturn. He is investing in lawsuits.

Not in trip-and-fall cases, mind you, but in disputes that are far larger, more costly and potentially more lucrative, often pitting major corporations against each other.

Mr. Fields is chief executive of Juridica Capital Management, which runs a fund that invests in one side of a lawsuit in exchange for a share of any winnings, The New York Times’s Jonathan D. Glater writes.

“It’s always a good time to invest in litigation,” Mr. Fields told The Times, though he added that the weak economy helped. “When the recession started to bite, the phones started ringing off the hook. Last year, we looked at 122 cases and we made 17 investments.”

A small but growing number of investors are exploring this idea, helping companies avoid some of the risks and costs of litigation in exchange for part of any money paid out when the case is settled or resolved by a court. After all, it can be costly to hire lawyers, who may charge close to $1,000 an hour at elite firms. -

A Closer Look at the 200-Day Moving Average

Posted by Eddy Elfenbein on June 2nd, 2009 at 2:17 pmOne of the quick-and-dirty tools used to technical analysts is to see where a stock or index is compared with its average price over the past 200 days. This is an easy way to get a read of a stock’s momentum.

Yesterday was a big day for the 200-DMA world. The S&P 500 closed above its 200-DMA for the first time since December 26, 2007. That closed out the index’s longest run below its 200-DMA according to my records which go back to 1932.

That streak, however, is still well short of the longest run above the 200-DMA which ran from November 1953 all the way to May 1956. Since the index has gone up over the time, the “above” streaks tend to be longer than the “below” streaks.

On November 20, 2008, the S&P was a stunning 39.6% below its 200-DMA. That’s the biggest discount on my records. The only thing that comes close is the reading from this past March.

So does the 200-DMA work? The evidence suggests that it’s a pretty good indicator of future price performance. When the S&P 500 has been below the 200-DMA, it’s dropped a total of about 20% over the equivalent of 27 years. In other words, the S&P 500 has been below its 200-DMA about one-third of the time.

Historically, the best time to invest has been when the S&P is less than 1.7% below the 200-DMA.

When the index is above the 200-DMA, well, then everything looks much brighter. All of the market’s gain and then some have happen when we’re above the 200-DMA which occurs about two-thirds of the time.

The market seems to like nearly every point of being above the 200-DMA. Danger only clicks in when the S&P 500 is over 17.5% above the 200-DMA which is a very high reading.

-

Peter Lynch on Bottom Fishing

Posted by Eddy Elfenbein on June 2nd, 2009 at 10:55 am

You can also see Phil Carret, the legendary money manager. In 1924, he wrote “The Art of Speculation.” Carret died in 1998 at 101. -

Academic Study: “Analysts’ revisions are typically information-free”

Posted by Eddy Elfenbein on June 2nd, 2009 at 9:16 amThe Irish Times notes that Wall Street analysts…you better sit down for this…often don’t know what they’re talking about:

The Citi research looked at analyst recommendations over the last 15 years. It found that analysts were at their most bullish at the end of 1999, despite the fact that price-earnings ratios suggested markets had never been so over-valued. The dotcom crash in early 2000 triggered a vicious three-year bear market during which analysts grew progressively bearish. This bearishness increased even as the market bottomed in the autumn of 2002. Bullishness took root as the market rose over the following five years, peaking just prior to the outbreak of the financial crisis. Since then, analyst bearishness has risen inexorably.

The report also looked at the difference in performance between the stocks most favoured by analysts and the stocks least favoured by analysts. It found that the furious global rally off the March bottom has caught analysts completely by surprise, with forecasters more off the mark than at any other time during the period under study.Later on.

The Financial Times reported this month on an academic study that looked at the effect of analyst recommendations on stock prices. It found that “buy” and “sell” tips have little appreciable effect on prices. “Analysts’ revisions are typically information-free,” the study concluded, adding that investors were aware of this.

One analyst who has been consistently critical of his fellow professionals is James Montier of Société Générale. The award-winning analyst said last year that it was “transparently obvious that analysts lag reality”. They “only change their minds when there is irrefutable proof they were wrong, and then only change their minds very slowly”, he said.

The latter study appears to confirm this – almost 80 per cent of analysts’ changes in recommendations came after major corporate events. Analysts are “like rabbits caught in the headlights”, Mr Montier said, and are “seemingly incapable of any form of independent thought”.Do rabbits stare at headlights?

Maybe analysts should start listening to this guy who has almost zero private sector experience:

The market is up 35% since then. -

Long Bond Hasn’t Suffered a Loss Like Since Since Another Century — And Not the 20th

Posted by Eddy Elfenbein on June 2nd, 2009 at 9:07 amMebane Faber writes that the long bond is suffering its worst draw down since at least 1900.

By the way, his new book is out. -

Dow Jones Admits It Paid Attention to Bloggers on Decision to Add Cisco to DJIA. Suck it S&P!

Posted by Eddy Elfenbein on June 1st, 2009 at 10:32 pmIn the WSJ, John Prestbo explains why they decided to replace GM and Citigroup with Cisco and Travelers today.Here are some highlights:

Did the fact that Travelers used to be part of Citigroup play a role in choosing that particular insurance company?

No. Citigroup spun off Travelers in 2002, so it has been operating independently for going on seven years. And it was independent prior to becoming part of Citigroup in 1998. We were committed to restoring the insurance sector to the Dow after ejecting American International Group, Inc. (AIG) last September after the government takeover. Travelers is a property and casualty insurer, as AIG is, and it is certainly a leader in that industry.

Why choose a tech company, Cisco, to replace an automaker?

We did not need another consumer goods company after adding Kraft Foods when we removed AIG. In looking around, we were struck by the fact that Cisco makes products that pave the Information Highway – computer networking equipment, things that enable high-speed data and video transmission, and so on. We saw Cisco helping the economy and culture adjust to the digital age, much as automobiles influenced economic and social changes in the 20th Century.

Well, why not Apple (AAPL) or Google (GOOG)?

Those companies certainly qualify as blue chips, but we chose Cisco this time.This part really caught my attention

Cisco has been on bloggers’ suggestion list for a long time. Do you pay any attention to these kibitzers?

Yes. They and many others take the Dow seriously enough to complain when they think we are doing something wrong and to offer their ideas. So, we take them seriously in return. However, most of these folks are looking at things from an investor’s point of view, as though the Dow was a portfolio they owned (and maybe some of them really do). But our goal is to maintain an index to accurately reflect the market as whole, and by extension the U.S. economy. That is a different purpose, which sometimes leads us in a different direction.Good for them! I’m glad they did two things. One, they listened to bloggers. Two, they said they listened to bloggers.

This is pretty big news for financial blogs. We’re talking about a 113-year-old index and one of the best brand names around.

Now…about Bing. -

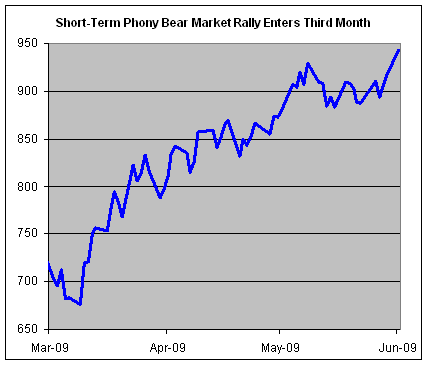

S&P Makes New High

Posted by Eddy Elfenbein on June 1st, 2009 at 7:43 pmWe did it. The S&P closed at 942.87, the highest close since November 5.

The phony, fraudulent, manipulated, short-term bear market sucker’s rally is now up 39%.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His