-

Marcy Kaptur Pwns Bernanke

Posted by Eddy Elfenbein on June 6th, 2009 at 2:30 pmSeveral months ago, a YouTube video made the rounds of Ron Paul questioning Ben Bernanke. The video was hailed as Paul putting Bernanke in his place. That’s not what I saw. Megan McArdle summed it up best: “I see a really, really smart economist responding to Ron Paul the same way you react to Cousin Mildred when she corners you after Christmas dinner to complain about the flouridation of the water supply.”

That’s pretty much what I see in this video that’s currently making the rounds:

Incidentally, Kaptur is the same person who didn’t even know who Bernanke was last year. -

Morning Links

Posted by Eddy Elfenbein on June 5th, 2009 at 10:01 amHere are a few items floating around the interblogs.

Abnormal Returns has an excellent post called Being right is overrated. AB should do more writing. David Merkel has a reply.

Justin Fox asks Are Stocks Still Good for the Long Run? My answer—they’re good enough.

Government benefit checks accounted for one-sixth of personal income in the first quarter.

Jim Cramer says Bernanke has saved us from the second Great Depression.

The LA Times notes the return of the male prostitute. Sadly, no mention is made of Fred Garvin. -

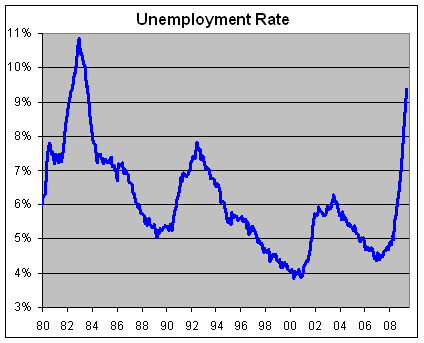

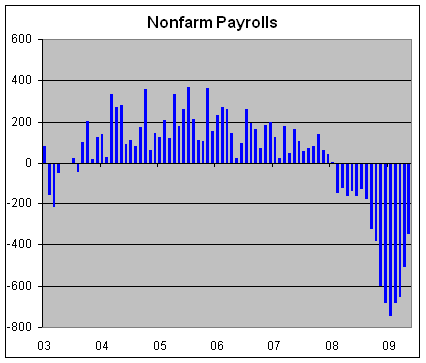

Job Market Sucks Somewhat Less than Expected

Posted by Eddy Elfenbein on June 5th, 2009 at 9:40 amThe jobs numbers are out today. Unemployment hit 9.4% last month and the nonfarm payrolls fell by 345,000 which was much less than the 525,000 loss Wall Street was expecting.

The unemployment hasn’t been this high since August 1983. The rate is being reported as 9.4% but looking at the details, it’s 9.357% which rounds up.

See how the last two bars on the NFP graph look like the beginning of a trend. That’s what the market has been so excited about.

-

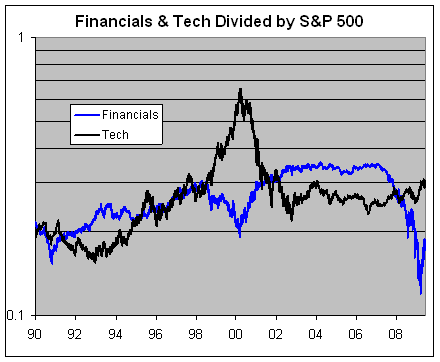

Financials and Techs Divided by the S&P 500

Posted by Eddy Elfenbein on June 4th, 2009 at 1:26 pmHere’s a look at the S&P Financial Sector Index (^SPSY) and Technology Sector Index (^SPLY) divided by the S&P 500 (^SPX). A rising line means that the industry group is outperforming; a falling line means it’s underperforming.

-

Happy 75th Birthday SEC

Posted by Eddy Elfenbein on June 4th, 2009 at 11:50 amOn June 6, 1934, FDR signed into law the Securities Exchange Act of 1934 which bright the Securities and Exchange Commission to Life. Roosevelt then appointed Joseph P. Kennedy to be its first head which caused some to think this was “setting a wolf to guard a flock of sheep.” (Incidentally, Georgetown hosts the poorly named Joseph P. and Rose F. Kennedy Institute of Ethics).

This hasn’t been a good year for the SEC. Regulators continue their war against efficient markets. Last year’s shorting ban in financial stocks was a bust (financials underperformed the broader market). The SEC completely missed the Madoff scandal after being told what was happening. The agency’s own inspector general said they bungled the Pequot Capital thing (“raised serious questions about the impartiality and fairness”).

It gets even worse. Check out this Dow wire story from earlier this week:The internal watchdog at the Securities and Exchange Commission revealed Monday his office is investigating several employees, including one top SEC official, after receiving complaints alleging they improperly disclosed non-public information.

One pending investigation by SEC Inspector General H. David Kotz comes in response to an allegation that a top SEC official improperly disclosed non-public information to a large investment bank.

In another case, Kotz reported that his office is investigating two enforcement attorneys for possibly disclosing non-public information from an internal SEC database to a corrupt FBI agent and short seller who was later convicted of fraud, racketeering and conspiracy.

Then, in yet a third case, the inspector general said he’s looking into whether a former SEC attorney may have revealed confidential investigative information in a book he wrote. Kotz said the attorney may have provided the privileged information to a company where he worked as a lobbyist after leaving the SEC.

Separately, his office is also trying to determine if non-public information may have been disclosed to a national news outlet.

Kotz, who is leading the internal investigation into the agency’s failure to detect Bernard Madoff’s Ponzi scheme, disclosed some details about his pending investigations in his newly published semi-annual report to Congress on Monday.

In it, he said he has 19 pending investigations, one of which is tied to the Madoff failings.Here’s to 75 more years!

-

Fantasy Football Lawsuit

Posted by Eddy Elfenbein on June 4th, 2009 at 11:34 amYahoo Inc. has sued the NFL Players Association, claiming it shouldn’t have to pay royalties to use players’ statistics, photos and other data in its popular online fantasy football game because the information is already publicly available.

Let’s see if I have this right: A company is bringing a real lawsuit against a group of adult men who play a children’s game for their statistics which are used by other adult men who merely pretend they’re in charge of the first group of adult men while they play the children’s game.

There are the parts of the New Economy I like best. -

Odd Lots

Posted by Eddy Elfenbein on June 4th, 2009 at 7:50 amHere are some assorted links I wanted to pass on:

Why having the Penguins win the Stanley Cup is good for the stock market.

Here’s an investment beating stocks and gold this year.

Actual academic report: The economics of Dr. Seuss.

Jeremy Siegel “virtually sure” it’s not going to be a long wait for a good return on stocks.

The rally is being led by junk stocks.

Ukraine’s economy drops 21% in Q1.

Iceland central bank slashes rates to 12%. In other news, Iceland has a central bank? -

Way Ahead of You

Posted by Eddy Elfenbein on June 3rd, 2009 at 5:28 pmThe Economist:

-

Good Story on DirectEdge

Posted by Eddy Elfenbein on June 3rd, 2009 at 4:43 pm -

Rep. Alan Grayson at Ritholtz-Palooza

Posted by Eddy Elfenbein on June 3rd, 2009 at 4:17 pmCongressman Alan Grayson had some interesting comments at Barry Ritholtz’s conference today:

Grayson appeared on a panel with Nassim Taleb, best known as the author of The Black Swan. Their exchange about the proper role of government regulation of the financial system was entertaining, if a bit meandering. Grayson, who grew up in the Bronx and holds three Harvard degrees, has a rare ability to say relatively radical things without coming off as a rabid populist. Moderator Barry Ritholtz, author of the just-published Bailout Nation, asked a straightforward question: The U.S. government does a reasonably good job of regulating things like the safety of airplanes and foods. Why, then, does it do such a lousy job of regulating the financial system?

Grayson’s answer was immediate and succinct: “Capture.” For those not up on regulatory theory, this refers to the notion that regulators become captive of the industries they regulate. Noting that Fannie Mae and Freddie Mac spent $100 million on campaign contributions over the last 10 years, Grayson said: “The system is in some sense corrupt. A senator said the other day that Wall Street owns Washington, and while I might not go that far, you don’t have the airlines ‘owning’ the [airline regulators]. There is a lot of influence that Wall Street has on the government, even the judicial branch.” Indeed, Grayson could have cited the front-page story in today’s Wall Street Journal, documenting the remarkable efficiency with which banking campaign contributions appear to have helped ease accounting rules that in turn helped the banks.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His