-

CWS Named One of Five Favorite Financial Blogs

Posted by Eddy Elfenbein on June 1st, 2009 at 2:49 pmDavid Berman at the Globe and Mail named Crossing Wall Street one of his favorite financial blogs.*

For four years, a long time in this business, Eddy Elfenbein has been treating readers with a mix of charts and sharp observation.

The others are Bespoke Investment Group, Stocks To Watch Today, Humble Student of the Markets and Footnoted.org.

* He actually wrote “favourite.” When are Canadians and Brits going to learn English? -

AMZN@$83

Posted by Eddy Elfenbein on June 1st, 2009 at 2:09 pmDid Amazon (AMZN) start trading in pesos today?

$83! Really?

This won’t end well. -

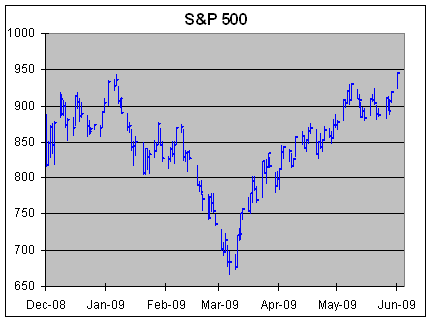

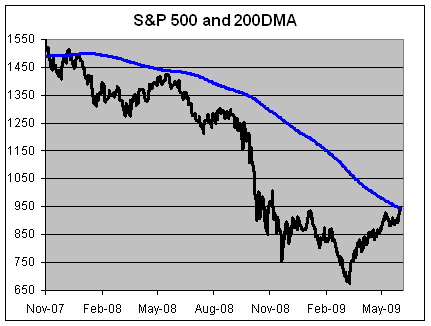

S&P Nears Seven-Month High

Posted by Eddy Elfenbein on June 1st, 2009 at 12:55 pmThe S&P 500 is currently over 945. If it holds up, this will be the highest close since November 5, the day after election day.

Also, if today’s gains hold up, the S&P 500 will be above its 200-day moving average for the first time in 18 months.

-

“What’s Good for General Motors Is Good for America”

Posted by Eddy Elfenbein on June 1st, 2009 at 11:02 amOne of great urban myths of American business history is that the head of GM once said “what’s good for General Motors is good for America.”

That line is once again getting a lot of press today. There’s one problem — it’s not true.

Here’s what happened. In 1953, President Eisenhower nominated GM’s CEO Charles “Engine Charlie” Wilson to be Secretary of Defense. I’ll turn it over to Wikipedia:During the hearings, when asked if as secretary of defense he could make a decision adverse to the interests of General Motors, Wilson answered affirmatively but added that he could not conceive of such a situation “because for years I thought what was good for the country was good for General Motors and vice versa.”

Gee, that’s kinda different. So what’s often portrayed as the ultimate in corporate arrogance that defined the atavistic nature of American capitalism was instead a humble statement of public spiritedness.

-

After 84 Years, GM is Booted from the Dow

Posted by Eddy Elfenbein on June 1st, 2009 at 9:37 amGM (GM) and Citigroup (C) are out, Travelers (TRV) and Cisco (CSCO) are in.

-

GM Goes Bust

Posted by Eddy Elfenbein on June 1st, 2009 at 9:03 amWhat used to be the largest corporation in the world is now bankrupt.

This isn’t exactly a surprise. Here’s what I wrote in 2006:Whither GM?

In 1979, the British economy was in free fall. Inflation was spiraling out of control. The unions were demanding commensurate pay increases, and when they didn’t get them, they struck. The country that had stood up to the Luftwaffe was failing apart. The garbage men went on strike and soon piles of “rubbish” dotted the countryside. Even the gravediggers went on strike and corpses were gruesomely left unburied.

The winter of 1978-79 was called the Winter of Discontent, echoing the opening lines of Richard III. The situation was so bad that Her Majesty’s government had to apply for a loan from the IMF. This was back in the days when that had some sense of shame to it. You were even expected to pay it back.

A reporter asked the Prime Minister, James, Callaghan, his opinion of the “the mounting chaos in the country.” Callaghan said: “Well, that’s a judgment that you are making. I promise you that if you look at it from outside, and perhaps you’re taking rather a parochial view at the moment, I don’t think that other people in the world would share the view that there is mounting chaos.”

That was it. British socialism died right there. The commanding heights were nothing more than a literal heap of trash. The next day, The Sun’s headline read: “Crisis? What Crisis?”

I can’t help but think of the similarities between British socialism and General Motors (GM). Once upon a time, GM ruled the world. Today, it’s an embarrassment. What’s good for GM, is largely irrelevant to America.

For reasons unclear, billionaire Kirk Kerkorian sunk a good part of his fortune in GM’s stock. His investment has been a disaster. Now’s he’s sent his aide, another son of York, Jerome York to be exact, to Detroit to tell the automaker everything they’re doing wrong. The New York Times quotes York as saying: “The time has come to go into crisis mode and act accordingly.”

No, the time to go into crisis mode has long since past. GM is a fiscal black hole. The company burns through $24 million a day. That’s more than the Yankees. Yet the company still pays out $566 million a year in its dividend. Crisis? What Crisis?

Talk about unburied corpses. I honestly don’t think GM will survive this decade. Even if it does, it will hardly be recognizable. Any future GM will merely be a Commonwealth living in the shadow of a by-gone Empire. York’s plan is to get rid of the dividend and reduce the pay of senior management. Well…that’s a nice start, but I think GM will have to go a lot further; perhaps ditching some of its key brands like Hummer.

The New York Times quoted Frederick A. Henderson, GM’s new CFO:“To be honest, I am in crisis mode. So I agree with him,” Mr. Henderson said. In December, he succeeded John M. Devine, now a G.M. vice chairman, who accompanied him to Mr. York’s speech. Like Mr. Devine, Mr. Henderson watched impassively while Mr. York spoke.

Impassively? Ha! I bet they were ready to toss him out the window. I’d actually feel much better if GM were really in crisis mode. They’re not. They’re sleepwalking. Perhaps now, they’re sleeprunning. This is a company that plainly refuses to see reality. They’d be plenty happy to go on ignoring the mess they’ve made, but high oil prices forced the issue. The long-run was much shorter than any of us expected.

The idea that GM can discount its way home is a foolish illusion. The facts are clear. Every GM car carries about $1,500 in health care costs. The employees’ health care trust has over $20 billion, and GM had to tap it twice recently. For $1 billion each time. Retirees outnumber current U.S. employees 2.5 to 1. The company has stopped providing earnings guidance.

GM’s problem isn’t cars or legacy costs. Companies can deal with those. What GM has is a leadership crisis. They need to make major changes soon. If not, the Winter of Discontent will last a very long time.. -

Very Cool Interactive Map of GM Fallout

Posted by Eddy Elfenbein on May 31st, 2009 at 11:54 pmCheck it out.

(HT: ZH) -

GQ quotes Nassim Nicholas Taleb as saying that in the falling market he “made $20 billion for our clients, half a billion for the Black Swan fund.” Yeah…about that.

Posted by Eddy Elfenbein on May 31st, 2009 at 10:45 pmJanet Tavakoli does some great legwork:

A recent GQ article quoted Nassim Nicholas Taleb as saying that in the falling market he “made $20 billion for our clients, half a billion for the Black Swan fund.”

I checked with Nassim Taleb regarding the $20 billion in gains and asked if he were misquoted. He responded via email: “The quote is inaccurate. THe [sic] 20 billion might correspond to the face value of positions.” This response is both vague and different in character from the mythical $20 billion in gains inaccurately quoted in GQ’s article. The total gains could be a tiny fraction of what Taleb loosely describes as “face value.”

Why is GQ’s mistake important? In my opinion, public claims of enormous private hedge fund gains require credible back up, and one would think that GQ would have known that before it inaccurately quoted Taleb as having made a bell ringing gain of $20 billion for clients. Presumably, the error referred to outside clients, not the black swan fund itself, but it could have the side effect of attracting investors to the black swan fund, similar to advertising or salesmanship.

The black swan fund’s strategy is purportedly to buy out-of-the-money put options on stocks and broad market indices and hedge tail risk for clients. The strategy may produce long periods of mediocre—or even negative—returns followed by a large gain and vice versa. No one can tell you for certain exactly when (or for how long) large gains are possible. Initial success in a newly created fund may not be replicated in the future, and there is always the problem of scaling. Scaling refers to the fact that an individual fund may make a high return on an initial investment, say 100% on $100 million, but lose 10% on $1 billion.Read the whole thing.

-

Jack Welch’s Challenge

Posted by Eddy Elfenbein on May 31st, 2009 at 12:23 pmIt was Jack Welch’s night to reign supreme once more.

That’s the assessment of Vanity Fair magazine, which along with Bloomberg News staged a panel discussion in Manhattan on Thursday evening on how the economy got into its current mess and how to get out of it. Vanity Fair said Mr. Welch, the former longtime chief executive of General Electric, was the audience favorite as he gave what it called “an unapologetic defense of old-school capitalism in a room teeming with past and future Masters of the Universe.”

Mr. Welch went head to head with the other panelists and the moderator, DealBook’s Andrew Ross Sorkin. At one point, he challenged the Nobel Prize-winning economist Joseph Stiglitz on the role of unions, saying, “Give me a highly successful, unionized American industry.”Hollywood.

Want another? Pro Sports. -

Corporate Dividends Are Drying Up According to Bankrupt Newspaper

Posted by Eddy Elfenbein on May 31st, 2009 at 12:13 pmThe Minneapolis Star Tribune reports:

In February, General Electric Co. — the classic widows-and-orphans stock — cut its dividend for the first time since 1938, a move that will save the company about $9 billion a year.

The January to March period marked the first quarter since Standard & Poor’s started recording dividend data in 1955 that the number of dividend cuts was greater than the number of dividend increases. A record low 283 companies announced dividend increases in the first quarter of 2009.

“While the number of dividend decreases is at a record high, the number of increases has set a new record low,” said S&P senior index analyst Howard Silverblatt in April. “Since 1955, the average has been 15 increases for every decrease. Now its three increases for every four decreases.”

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His