-

“Mother of inflated hope/Mistress of despair”

Posted by Eddy Elfenbein on May 21st, 2009 at 2:06 pmThe Chronicle of Higher Education interviewed economist Stephen Ziliak.

In haiku.Q. How does writing verse

Help your students understand

A math-based science?

A: Thought transportation —

Newton’s laws might still abide,

Listen: Einstein’s train.

Q: A labor union

Protects workers from abuse —

But what does it cost?

A: Green Knights of Labor,

free Haymarket Anarchists,

cost less than Madoff.

Q: Debt plus recession —

Which is the better move:

saving or spending?

A: Treasury shoppers

choose plain broth over duck soup,

Nudge this paradox.

Q: Regarding Wall Street,

Do virtues of laissez-faire

Apply as elsewhere?

A: Traders are human,

swapping vices for virtues

and vice versa.

Q: Mom and Dad, I’m home!

The job market is nasty —

Where is my bedroom?

A: Invisible hand:

Mother of inflated hope,

Mistress of despair!

Q: Haiku might seem dumb

to bean counters and stuffed shirts —

Students disagree?

A: In this other world

wild orchids freely blossom —

haiku GDP. -

First They Came for My Natty Bo…

Posted by Eddy Elfenbein on May 21st, 2009 at 11:30 amUSA Today reports:

WASHINGTON (AP) — Consumers in the United States may have to hand over nearly $2 more for a case of beer to help provide health insurance for all.

Details of the proposed beer tax are described in a Senate Finance Committee document that will be used to brief lawmakers Wednesday at a closed-door meeting.

Taxes on wine and hard liquor would also go up. And there might be a new tax on soda and other sugary drinks blamed for contributing to obesity. No taxes on diet drinks, however.

Beer taxes would go up by 48 cents a six-pack, wine taxes would rise by 49 cents per bottle, and the tax on hard liquor would increase by 40 cents per fifth. Proceeds from the new taxes would help cover an estimated 50 million uninsured Americans.I bet Obama would never tax appletinis or mojitos.

-

Very Short Post on MO

Posted by Eddy Elfenbein on May 21st, 2009 at 11:13 amIf you’re looking for a nice yield, it’s hard to find something better than Altria Group (MO). The company just declared a quarterly dividend of 32 cents a share. That comes to 7.8% a year. The company has decent cash flow so I don’t see the dividend being cut to pieces.

-

Disturbing Segment on CNBC

Posted by Eddy Elfenbein on May 20th, 2009 at 2:12 pmOn CNBC, Jeff Macke starts acting weird, then very weird. You know it’s bad when Dennis Kneale is the sane one.

I’ve watched this clip a few times and I have no idea what Macke is talking about. It seems like he’s referring to some inside joke, but I don’t get where he’s going. Poor Dennis just backs away.

(Via: Clusterstock) -

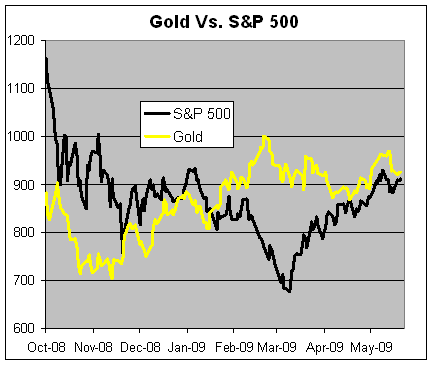

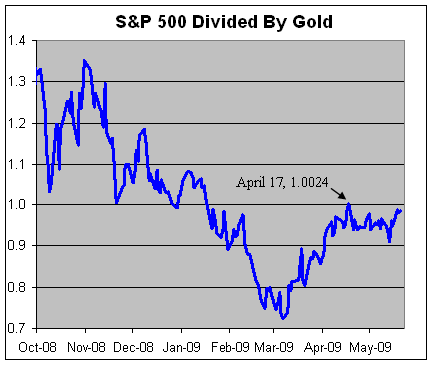

Gold Vs. the S&P 500

Posted by Eddy Elfenbein on May 20th, 2009 at 12:42 pmHere’s a look at how gold has done against the S&P 500:

Here’s the same graph but I divided the two numbers (S&P 500 by gold):

On the day of the inauguration, exactly four months ago, the ratio slipped below 1.0. The ratio has previously bounced off 1.0 on November 20. Since the inauguration, it’s closed above 1.0 only once and that was on April 17 which was the day of Citigroup‘s (C) **cough** “earnings” report.

Interestingly, the S&P has stayed roughly even with gold over the past few weeks which puts the rally in a different light.

My view is that we’ll test 1.0 again. If the market likes what it sees, then we might move much higher. -

Nouriel Roubini in TNR

Posted by Eddy Elfenbein on May 20th, 2009 at 7:56 amSaturday Night Live recently had a strange skit about a talk show hosted by the Bee Gees. Honestly, it wasn’t terribly funny but what struck me was that one of the guests was supposed to be Nouriel Roubini (I think it was Fred Armisen).

The Roubini character was the straight man in the skit, but it’s telling that he’s reached the point where he can be a typical “important person” you’d see on a talk show, even a parody of one.

Roubini is probably the hottest economist in the world right now. More tellingly, we live in a time where there is a hottest economist in the world.

Roubini just got another honor, a profile in the New Republic. It’s a pretty good profile. One complaint I have is that these profiles often try a tired formula—that the person’s ideas are an outgrowth of who they are. The New York Times tried that recently with Freeman Dyson and it didn’t work.

The truth is that you often can’t see a connection between important thinkers and their personalities or backgrounds. This sort of game can easily descend in psycho-babble. It will read something like, “He’s ideas are outside the mainstream and in high school, he was…wait for it…an outsider. Hello, Theme!!”

There’s even a theory that the stalemate in economics between investment (the male) and savings (the female) was finally broken by Keynes, the homosexual. That’s totally loopy to me but hey, it’s not my idea.

I’ve never met Roubini, but I would think the interesting angle to take is that he seems to be the opposite of his ideas—the playboy professor with the buzzkill forecasts.

Unquestionably, Roubini is an important thinker. However, I was glad to see the profile mention that Roubini hasn’t been as prescient as many people believe:Anirvan Banerji, an economist with the Economic Cycle Research Institute, has been particularly dismissive of Roubini’s forecasting abilities: “The average time between recessions is about five years in the postwar period,” he says. “So, if you forecast a recession one year and it doesn’t happen, and you repeat your forecast year after year … at some point the recession will arrive.”

And Roubini has undeniably overshot. In 2004, he predicted that the oncoming recession would precipitate the crash of the dollar. The crisis has mainly buoyed it. On September 1, 2005, three days after Hurricane Katrina made landfall, Roubini told Reuters that economic disaster was imminent. What followed instead was a bump in financial activity that forestalled the recession for more than two years.If you’re waiting for Jon Stewart to do a sanctimonious takedown of Roubini, I wouldn’t hold your breath. Though I nearly choked when the profile mentioned Nassim Taleb, “who also predicted a catastrophe in his book The Black Swan.” The old adage is true: It’s not what books say that’s important, it’s what people assume they say that’s important.

I’m glad to see Roubini get the attention, fame and fortune he deserves. But I have to add we shouldn’t judge economists by how accurate their macro forecasts are. That’s a losing game. Instead, we should focus on the power of their ideas to explain the economy, and see the connections that they see.

If you want to be a prognosticator, then go on the record with specific advice. If not, then you should try to explain the economy as clearly as you can. -

This Just In…

Posted by Eddy Elfenbein on May 19th, 2009 at 5:51 pmPeople With Higher IQs Make Wiser Economic Choices, Study Finds

People with higher measures of cognitive ability are more likely to make good choices in several different types of economic decisions, according to a new study with researchers from the University of Minnesota’s Twin Cities and Morris campuses.

The study, set to be published online in the Proceedings of the National Academy of Sciences this week, was conducted with 1,000 trainee truck drivers at Schneider National, Inc., an American motor carrier employing 20,000. The researchers measured the trainees’ cognitive skills and asked them to make choices in several economic experiments, and then followed them on the job.

People with better cognitive skills, in particular higher IQ, were more willing to take calculated risks and to save their money and made more consistent choices. They were also more likely to be cooperative in a strategic situation, and exhibited higher “social awareness” in that they more accurately forecasted others’ behavior.I’m looking forward to authors’ follow-up study, “Your Ass and a Hole in the Ground: A Study on Dissimilarities.”

-

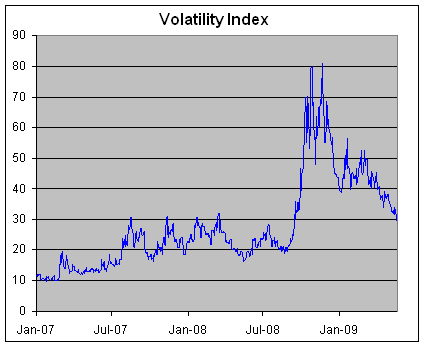

The VIX and Market Returns

Posted by Eddy Elfenbein on May 19th, 2009 at 4:17 pmMost commentators assume that low volatility is good for the market. That’s not necessarily the case. All a high low or VIX is at predicting is high or low volatility, not direction.

CNBC reports:Historically, the S&P has seen an average of 3% and 6% gains respectively over the 3 and 6 months that follow a crossover below 30.

That’s a completely useless stat. The general market averages close to those returns anyway. Given the historical sample size, that study simply measures noise and nothing else.

Here are some numbers I came up with:

Since 1990, when the VIX is below 15 (about 31% of the time), the S&P’s annualized return is 7.8%.

When the VIX is between 15 and 20 (27% of the time), the S&P’s annualized return is 2.8%.

When the VIX is between 20 and 25 (22% of the time), the S&P’s annualized return is -1.5%.

When the VIX is over 25 (20% of the time), the S&P’s annualized return is 11.1%.

To the extent there’s a tipping point, it seems to be a VIX of 13. Above 13, the S&P shows an annualized return of 3.0%, below 13 it jumps to 14.1%. However, 13 is a very low VIX reading; it’s been below 13 about 18% of the time.

Outside that, there doesn’t seem to be much of a trend. -

Amazon at $77

Posted by Eddy Elfenbein on May 19th, 2009 at 1:17 pmAmazon (AMZN) is at $77 a share!

Really? Is that real money, or Monopoly money or Canadian euros??

If they mean actual U.S. dollars, I wouldn’t pay half that much. -

Volatility Chills

Posted by Eddy Elfenbein on May 19th, 2009 at 12:10 pmThe Volatility Index (VIX), which is also known as the “fear index,” dipped below 30 today for the first time in eight months. Personally, I’m glad I’m not in my 20s anymore.

At one point, the VIX nearly hit an intra-day high of 90. A lower VIX isn’t necessarily good for the bulls or bears, but it does show that the market is very different from a few months ago.

-

Archives

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His