-

CWS Market Review – July 26, 2022

Posted by Eddy Elfenbein on July 26th, 2022 at 7:58 pm(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

This is an unusually busy week for the stock market. About one-third of the companies in the S&P 500 are due to report their earnings this week. There’s also a Federal Reserve meeting with an expected rate hike. If that’s not enough, we’ll also get our first look at the report on Q2 GDP.

So far, our Buy List earnings reports are looking quite good. I’ll have more details in the premium issue later this week. Fiserv, for example, released a nice earnings report this morning, and the company raised its full-year guidance. The stock rallied over 4.2% today.

Walmart Drops 8% on Profit Warning

This earnings season, Wall Street is keeping a close eye on how companies are dealing with rising costs. This is a tough issue because it works at both ends. Companies are facing rising input costs for their goods, and they need to pass along on their higher expenses to their customers. Some companies can do this effectively, while others cannot.

With investing we always want to look at “switching costs.” This is one of the key pillars of “wide-moating” investing.

Think of it this way: if Company X were to disappear tomorrow, how easily would consumers be able to move on? If its products aren’t available, could they be effectively mimicked somewhere else? For some companies, that’s not a problem but as investors, we want to focus on stocks that are nearly irreplaceable.

For many years, there simply was no substitute for Walmart (WMT). In fact, the company rose to prominence by being a substitute for Main Street.

I mention Walmart because after the closing bell yesterday, Walmart shocked Wall Street by lowering its guidance for this year. I should explain that Walmart is so large that its quarterly earnings report is effectively a report on American consumer behavior. The company will have sales this fiscal year of about $600 billion.

In May, Walmart said it’s expected to see its operating income for the year fall by 1%. Now it’s expecting a drop of 10% to 12%. The initial estimate had been for an increase of 3%. Walmart laid the blame on inflation. The retail giant said that higher prices are holding back shoppers.

This isn’t the first time Walmart said it’s having trouble. In May, the company said that it was sitting on too much inventory. That’s about the worst problem a retailer can face. The only way out is to slash prices and hope the goods finally move. In May, Walmart said that its inventory jumped by 33% during Q1.

On Tuesday, shares of Walmart dropped by close to 8%. The company’s warning scared the entire sector. Shares of Target and Amazon also got punished, but by not as much as WMT. Walmart is also a component of the Dow Jones Industrial Average so its fate has an out-sized impact on the stock market

Walmart, like many retailers, follows an off-cycle reporting schedule. Its fiscal year ends at the end of January. It does this so the holiday shopping season lands in one reporting quarter. This means that its fiscal Q2 will end at the end of this month. Walmart will report its results for Q2 on August 16.

Walmart said that it expects to see comparable-store sales growth of 6% for Q2. The problem is that the growth is coming from the low-margin areas. For Walmart, its groceries are nearly a loss leader. They only sell grocery items to get people inside. The apparel business carries much larger profit margins.

During an inflationary environment, consumers tend to focus on lower-priced items, be it beer or coffee or dining out. Once again, it’s about switching costs.

This spring, the big box retailers have been facing big problems of shifting consumer behavior. During the pandemic, shoppers used their stimulus checks to buy things like patio furniture. While that’s good, those tend to be one-shot items. Consumers aren’t going to buy patio furniture again next year. The issue isn’t as much about growth as it is about maintaining profitability.

Weakness at Walmart is not an encouraging sign for the overall health of the U.S. economy.

Are We in a Recession?

On Thursday, the government will release its initial report on Q2 GDP growth. Wall Street expects low but positive growth, but there is a good chance that growth will be negative. If that’s the case, it will be the second quarter in a row of negative GDP growth. For Q1, the economy shrank at a 1.6% annualized rate.

Two or more quarters in a row of negative GDP growth is often called the definition of a recession; however, that’s not technically correct. I hate to get into issues of semantics, but in this case it matters.

Two or more quarters of negative GDP is a convenient shorthand for a recession. Most times, that would align with a recession, but there can be exceptions. This could be one of those times.

The committee that decides when recessions begin and end is run by the National Bureau for Economic Research (NBER). This is from their website:

The NBER’s traditional definition of a recession is that it is a significant decline in economic activity that is spread across the economy and that lasts more than a few months. The committee’s view is that while each of the three criteria—depth, diffusion, and duration—needs to be met individually to some degree, extreme conditions revealed by one criterion may partially offset weaker indications from another. For example, in the case of the February 2020 peak in economic activity, we concluded that the drop in activity had been so great and so widely diffused throughout the economy that the downturn should be classified as a recession even if it proved to be quite brief. The committee subsequently determined that the trough occurred two months after the peak, in April 2020. An expansion is a period when the economy is not in a recession. Expansion is the normal state of the economy; most recessions are brief. However, the time that it takes for the economy to return to its previous peak level of activity may be quite extended.

The problem is that the drop of 1.6% for Q1 sounds worse than it was. During Q1, consumer spending held up relatively well despite rising costs. This is an example of something sounding like a lame excuse, but it is true in this case.

I think it’s unlikely that the U.S. is in a recession at the moment. I would place the odds at 30%, give or take. However, I’m more concerned about where the economy is headed in the near future, and it’s not encouraging. If we were to look out some, then I would say there’s a 75% chance of a recession starting sometime in the next 12 months.

Expect the Fed to Hike Rates by 0.75%

Much of the direction of the economy depends on what the Federal Reserve plans to do. The Fed meets this week, starting today and concluding tomorrow. The Fed’s policy statement will be out tomorrow afternoon at 2 p.m. ET.

It’s very likely that the Fed will raise short-term interest rates by 0.75%. That will bring the target for the Fed funds target range to 2.25% to 2.5%. Traders on the futures markets think there’s a 25% shot of a full 1% increase. That’s probably unlikely, but it’s interesting that some people are expecting that.

What comes next? I think we can expect more rate hikes, but this is the problem for the Fed. If the economy starts to show weakness, there will be pressure to stop the hikes, or even cut rates.

In fact, futures traders expect a rate cut next year. That’s highly unusual. Quick pivots in Fed policy have certainly happened before, but I don’t recall a pivot that was expected.

The futures market now thinks the Fed will have its target range at 3% to 3.25% in June 2023. That’s 0.25% lower than the prior in meeting in May. A recession next year is a very real possibility.

Good Relative Performance for our Buy List

I’m always a little hesitant to highlight our performance when our Buy List is doing well. I don’t want to jinx it, but I will take a brief moment to point out that our strategy has been outperforming the market over the last several weeks.

Since April 4, the AdvisorShares Focused Equity ETF is down 7.49% while the S&P 500 ETF is down 14.06%. Yes, I’m guilty of some minor cherry-picking, but we’ve earned it. Being down less in a down market may not sound like a great result but it makes a big difference over the long term.

If you want to learn more about our ETF, you can visit our website here.

3M to Spin Off Its Health Care Business

Before I go, I wanted to mention today’s announcement from 3M (MMM). I discussed this stock last year as an example of a good company that’s been weighed down by legal costs.

For years, 3M was a great company. Blue chips don’t get much bluer than 3M. It’s beaten the market and consistently increased its dividend. Recently, however, the stock has lagged badly.

When a well-run outfit sees its stock lag, I take notice. The problem 3M faces is lawsuits regarding the environmental damage resulting from chemicals it used to use. There’s also a lawsuit regarding 3M’s earplugs for the military.

Today, 3M said it will spin off its health care business. It will also seek bankruptcy for its subsidiary that made the military earplugs.

I like to see companies break themselves up. Pay attention when a good company has a garage sale. This can often be very good for shareholders. The new companies are no longer burdened with the legacy costs of the parent companies.

With the health care business gone, 3M will be in three business lines; safety and industrial products, consumers products and electronics and transportation. It will still be a very sizeable company. The stock gained 5% today.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

-

Morning News: July 26, 2022

Posted by Eddy Elfenbein on July 26th, 2022 at 7:05 amAs Prices Soar in Ukraine, War Adds Economic Havoc to the Human Toll

Earnings and Gas Worries Keep Europe Subdued

China Targeted Fed to Build Informant Network, Access Data, a Probe Says

Powell’s Bond Market Recession Indicator Is Sending a Warning

Fed Prepares Another Rate Increase as Wall Street Wonders What’s Next

Why a Strong Dollar Is a Double-Edged Sword for the U.S. Economy

She’s 17 and Has a Roth IRA. How Gen Z Is Handling Its First Bear Market

The ‘Free’ Checking Myth Is Costing Consumers Over $8 Billion

Low-Cost Cities With Strong Economies Remain Attractive as Housing Market Slows

More Signs Emerge That Inflation Is Altering Shopping Habits

Melting Profits Threaten the Ice Cream Man

Tech Antitrust Bill Threatens to Break Apple, Google’s Grip on the Internet

Newly Cheap Microsoft Is Still a Favorite Growth Play for Investors

GE Tops Estimates After Aviation Sales Surge

Coca-Cola Tops Sales Estimates on Higher Prices, Raises Guidance

G.M. Profit Falls 40 Percent as Costs Rise and Chips Are Lacking

UBS Misses Expectations; CEO Cites One of the ‘Most Challenging’ Quarters for Investors in a Decade

Be sure to follow me on Twitter.

-

Get Ready for a Busy Week

Posted by Eddy Elfenbein on July 25th, 2022 at 10:42 amThe stock market is a bit lower this morning. This will be a busy week for Wall Street. We have lots more earnings plus the Fed meeting. About one-third of the S&P 500 is due to report earnings this week.

This is the final week of trading for the month of July, and it looks like it could be the market’s best month of the year so far. Tech stocks are lagging so far today, and energy stocks are doing well.

For this week’s meeting, traders see a 77% chance of a 0.75% rate increase. Assuming that’s correct, traders are about evenly divided on the outlook for the September meeting. About half see a 0.5% increase, while the other half sees a 0.75% rate increase.

The GDP report is due out on Thursday. This will be the government’s first look at how well the economy did during the second three months of this year. Wall Street is expecting small but positive growth.

-

Morning News: July 25, 2022

Posted by Eddy Elfenbein on July 25th, 2022 at 7:07 amChina’s Gen Z Is Dejected, Underemployed and Slowing the Economy

China Chases Chip-Factory Dominance—and Global Clout

Japan Is a Reminder of How Situational Today’s Inflation ‘Hawk-ery’ Is

Germany on Cusp of Recession, Says Ifo, as Business Sentiment Sinks

Bank of England Policymakers Torn on Need for Big Rate Move Next Week

Fed’s United Front on Interest Rates May Soon Be Tested

Morgan Stanley, JPMorgan Disagree on Outlook for Fed’s Pivot

The 60/40 Strategy Will Make a Comeback, Morgan Stanley Says

Weak Earnings Reports Aren’t Fazing Investors After Brutal Year for Stocks

‘I’m Always Worrying’: The Emotional Toll of Financial Stress

Cheaper Beer, Cigarettes Gain Favor as Inflation Pinches Shoppers

We Need to Keep Building Houses, Even if No One Wants to Buy

A $40 Billion Wireless Sector Meltdown Puts Focus on T-Mobile

Why Big Tech Is Making a Big Play for Live Sports

Bed Bath & Beyond Followed a Winning Playbook—and Lost

Clock Ticks for Evergrande Restructuring Plan After Shakeup

Ties Between Alex Jones and Radio Network Show Economics of Misinformation

Be sure to follow me on Twitter.

-

The S&P 500 briefly breaks 4,000

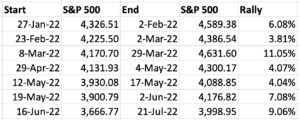

Posted by Eddy Elfenbein on July 22nd, 2022 at 11:02 amThis latest bear-market rally is looking pretty good. It’s the second-best rally of this bear market. Here’s a list of the others.

The S&P 500 briefly broke above 4,000 this morning. Earnings are still the big story. Facebook is down over 5%. Verizon is off by more than 6% after it missed by a penny per share. Shares of Snap are down 36% today after another terrible earnings report.

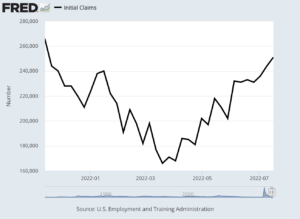

Yesterday’s jobless claims report rose to 251,000. I wouldn’t say that’s a higher number, but it’s certainly a trend of higher claims. This may show up in the official jobs report soon.

-

Morning News: July 22, 2022

Posted by Eddy Elfenbein on July 22nd, 2022 at 7:01 amJapan Inflation Shows Early Signs of Hitting a Peak

The Economy Putin Didn’t Actually Ruin

Europe Joins Fight Against Inflation, Raising Rates for First Time in 11 Years

Spain’s Finance Minister Says Decision on Bank Tax is “Taken and Fair”

New China Covid-19 Lockdowns Would Threaten U.S. Economic Recovery (Just Ask Tesla)

Germany Bails Out Struggling Gas Provider Uniper with a Multibillion-Euro Rescue

Recession Now Looks Like the Price to Pay for Beating Inflation

BofA Says Stock Outflows Are Catching Up to Market Despair

‘Awful’ Snap Sales Wipe $76 Billion From Social Media Stocks

China Fines Didi $1.2 Billion as Tech Sector Pressures Persist

Airlines Are Making Money Again, But They Can’t Keep Up With Surging Travel Demand

Amazon Faces Fierce Competition in Health Ambitions After One Medical Deal

Domino’s Earnings Miss Expectations as Pizza Chain Struggles with Driver Shortage, Higher Costs

Three Arrows Founders Break Silence Over Collapse of Crypto Hedge Fund

A Town Built on Gold Is Being Swallowed by the Earth

Be sure to follow me on Twitter.

-

Morning News: July 21, 2022

Posted by Eddy Elfenbein on July 21st, 2022 at 7:00 amRussia Resumes Nord Stream Natural-Gas Supply to Europe

U.S. Initiates Trade Fight With Mexico Over Energy Policy

Japan Leaves Weak Yen Alone Despite Above-Target Inflation

The Relentlessly Peculiar Notion of Government ‘Fighting’ Inflation

A Recession Alarm Is Ringing on Wall Street

U.S. Home Prices Hit Record of $416,000 in June as Sales Continued to Slide

The US Has Lost Its Way on Computer Chips

How Software Is Stifling Competition and Slowing Innovation

More Investors Vote Against Corporate Directors Over Climate Change

Angel Investor Calacanis Rips Into ‘Grifting’ VCs Flipping Crypto Tokens to Retail

Loans Could Burn Start-Up Workers in Downturn

Protesting Truckers Pledge Extended Blockade of Port of Oakland

Apple Can Hit $3 Trillion on Services Shift, Morgan Stanley Says

Tesla Ends Streak of Record Quarterly Profits After China Factory Shutdown

Elon Musk Signals Optimism Tesla’s ‘Supply Chain Hell’ Will End

China Fines Didi $1.2 Billion After Wrapping Year-Long Probe

Why Netflix’s Earnings Weren’t Enough to Restore Confidence

Be sure to follow me on Twitter.

-

Abbott Beats the Street

Posted by Eddy Elfenbein on July 20th, 2022 at 10:24 amThe stock market is down a bit so far in early trading.

Abbott Labs (ABT) kicked off earnings season for us this morning. For Q2, Abbott earned $1.43 per share. That was 31 cents better than estimates.

The company now expects full-year earnings of at least $4.90 per share. That’s an increase of 20 cents per share to its previous forecast. The shares are currently down about 2%.

The existing-home sales report came out this morning. The number of existing homes sold fell to a two-year low. The annualized rate was 5.12 million. Expectations were for 5.35 million. Hats off to Tom Lawler, the housing economist, who got the number exactly right.

The median sales price rose to $416,000 which is another record.

-

Morning News: July 20, 2022

Posted by Eddy Elfenbein on July 20th, 2022 at 7:07 am‘My Worldview Has Been Destroyed’: Chinese Banking Scandal Tests Faith in the System

Russia Is China’s Top Oil Supplier for 2nd Month, Saudi Volumes Tumble

Putin Signals Russian Gas Will Resume in a Key Pipeline but at a Reduced Level

Inflation Climbs to 9.4 Percent in Britain, a New 40-Year High

Italy Is Haunted by the Pain of Past Economic Crises

ECB Being Pulled in Multiple Directions as It Preps First Rate Rise in Decade

Powell’s Econ-101 Lesson Presents Best-Case Inflation Scenario

Bernstein Strategists Say Stocks Have Yet to See Capitulation

Blackstone Sees Fed Funds Rate Near 5% on Longer Hiking Cycle

Sam Bankman-Fried Turns $2 Trillion Crypto Rout Into Buying Opportunity

CFPB to Push Banks to Cover More Payment-Services Scams

Mortgage Demand Drops to a 22-Year Low as Higher Interest Rates and Inflation Crush Homebuyers

Home Building Stalls as the Real Estate Market Cools. That Won’t Help Affordability

As EVs Go Mainstream, A Rush for Share of Home Charger Market

The Pilot Shortage Is About to Get A Lot Worse

Eric Adams Says NYC ‘May Not Have Central Business Districts Anymore’ as Remote Work Persists

Twitter-Musk Trial Set for October in Lawsuit Over Stalled $44 Billion Takeover

Be sure to follow me on Twitter.

-

CWS Market Review – July 19, 2022

Posted by Eddy Elfenbein on July 19th, 2022 at 4:23 pm(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

Inflation-Phobia Stalks Wall Street

The stock market is still spooked by last week’s CPI report. Some observers thought we might see some cooling off of inflation. Well, that was not the case. Over the last year, inflation is running at 9.1%.

Inflation falls particularly hard on lower-income consumers and we’re already seeing it alter consumer behavior. According to the latest data, consumers are cutting back on purchases at the grocery store. Last month, for example, the price for a pound of white bread got to $1.69. That’s up 12% from last year. A pound of wheat bread got to $2.22, which is a record. In many parts of America, gasoline recently broke $5 per gallon, although it’s been drifting lower recently.

While inflation is tough for consumers, it also wreaks havoc on the financial markets. The data shows that inflation is fairly benign until it gets to about 5%. Above that, stocks start to feel the squeeze, and right now, we’re nearly double that rate. This is why everyone is on edge.

Following last week’s inflation report, there was a brief period where traders were expecting a full 1% increase from the Federal Reserve at next week’s FOMC meeting. However, the Wall Street Journal had a story over the weekend which said that a 0.75% increase is much more likely. As we know, the Fed pays close attention to inflation expectations. A recent survey of inflation expectations dropped to its lowest level in a year.

Still, that hasn’t calmed folks down. Despite the WSJ article, traders are currently placing 35% odds on a 1% hike. I doubt that will happen, but it shows how unnerved traders are. Even if we only get a 0.75% hike next week, we’ll probably get another 0.75% increase in September. Before the end of the year, it’s very possible that short-term interest rates will be 2% higher.

The higher rates are already having an impact. This morning, we got a report that housing starts fell for the second month in a row. Housing starts are now at a nine-month low. The bright spot, if there is one, is that homebuilders are still busy working down their backlog of unfilled orders.

The U.S. Dollar’s “Doom Loop”

Another side effect of higher interest rates is the soaring U.S. dollar. Recently, the dollar reached parity against the euro for the first time in 20 years. The dollar has also reached an all-time high against the Indian rupee. It also reached a high against the yen.

There’s even been talk of a possible “doom loop” involving the U.S. dollar. Simply put, that means that the strong dollar causes economic weakness which in turn leads to an even stronger dollar, which leads to more weakness. The cycle then repeats itself ad nauseam.

In normal times, that’s an easy cycle to break. The Fed would simply lower interest rates and weaken the dollar, but it can’t do that now with inflation heading toward 10% per year.

Here’s the Dollar Index. Notice how strongly it has rallied over the last year.

This angle gets more interesting because the European Central Bank meets on Thursday and is expected to raise interest rates for the first time in 11 years. The ECB’s President, Christine Lagarde, has signaled that the ECB will hike by 0.25%, but some economists think it will be a 0.5% increase.

The strong dollar is having an impact almost everywhere. Obviously, the Fed is keeping its eye on the foreign exchange market, but we’re seeing its impact within U.S. companies. While the dropping euro is great for U.S. tourists, it’s terrible news if you’re a big tech stock.

I’ll give you a perfect example. Yesterday afternoon, IBM (IBM) reported decent results for its Q2. For the quarter, IBM made $2.31 per share which was four cents better than Wall Street’s consensus. The company also said that it shut down its operations in Russia.

But neither of those issues were the big story. Instead, IBM said it expects to take a 6% hit to its revenues thanks to the strong dollar. That’s a big bite. IBM’s earlier projection had been for a hit of 3% to 4%. Q2 revenue was hit by $900 million thanks to the greenback. We’re talking about a $3.5 billion bite this year. Despite a good quarter, the dollar news dominated everything, and it’s likely to get worse. Shares of IBM fell 5.25% today.

This is just the beginning. The strong dollar is going to beat up several more tech stocks this year. We just don’t know yet which ones and how much.

Earnings Season Is Heating Up

This is also the start of earnings season. Only about 9% of the S&P 500 has reported so far, so it’s too early to draw any large conclusions. The “beat rate,” meaning how many firms have reported earnings better than expected, is running at 65%. That may sound good, but it’s well below the 77% rate that Wall Street has averaged over the past five years.

By the way, you read that correctly. Historically, a large majority of companies beat expectations, but those are the official expectations. The expected expectations may not be the same as the official expectations. Some companies are very skillful in managing what Wall Street analysts say. It’s all about expectations.

Wall Street had been nervous going into this earnings season. A recent survey by Bank of America showed wide-spread pessimism from investors. Recession expectations are at their highest levels since the pandemic.

Fortunately, many of the earnings reports we got today relieved investors. The dollar also fell some today which probably helped the bulls. The S&P 500 closed higher by 2.76%. This was the best day for stocks in nearly one month. For the first time since April 20, the S&P 500 closed above its 50-day moving average. That can often be a good omen, but I encourage you not to read too much into it.

The Nasdaq Composite also had a very good day. The index closed higher by 3.1%, but the really strong index today was the Russell 2000. The small-cap index rallied 3.5% today.

Here’s a great stat from Callie Cox: ten times this year, the S&P 500 has rallied more than 1% during the day only to finish lower on the day by the closing bell.

Shares of Johnson & Johnson fell over 1% today after the company beat earnings but lowered its guidance for the rest of this year. Lockheed Martin missed expectations, but the stock rallied 0.8% today.

In after-hours trading, shares of Netflix traded higher by 8%. The good news for Netflix is that it “only” lost 970,000 subscribers last quarter. Wall Street had been expecting a loss of two million. Once again, it’s all about expectations.

Tomorrow, we’ll get our first Buy List earnings report when Abbott Labs (ABT) releases its Q2 earnings report. The results will come out before the opening bell.

Previously, the company told us to expect full-year earnings of $4.70 per share. For Q2, Wall Street expects earnings of $1.12 per share. Not only am I expecting Abbott to beat Wall Street’s view for Q2, but I think there’s a good chance they’ll raise their full-year guidance as well.

Mueller Industries Soars 14.5%

In June 2021, I featured a small stock for you called Mueller Industries (MLI). Muller is one of those little stocks that’s virtually ignored by Wall Street. The company has a great long-term track record, yet no Wall Street analysts follow it.

Mueller is a leading manufacturer of copper, brass, aluminum and plastic products. This is a classic small-cap cyclical stock. Once you realize the scope of their business, you understand that the use of Mueller’s products is seemingly endless. Mueller makes everything from copper tubing and fittings to brass and copper alloy bars and refrigeration valves.

You can find Mueller most anywhere. Some of the companies that rely on Mueller are in sectors like plumbing, heating, air conditioning, refrigeration, appliance, medical, automotive, military and defense, marine and recreational. Mueller’s operations are located throughout the United States and in Canada, Mexico, Great Britain, South Korea, and China.

Mueller has about 5,000 employees and it’s based in Collierville, Tennessee. The company’s operations are divided among three divisions: Piping Systems, Industrial Metals, and Climate.

I bring up Mueller because the company released an outstanding earnings report. I can’t tell if it beat expectations or not because no one follows it, so there are no expectations. For Q2, Mueller made $3.65 per share. That’s up from $1.92 per share for last year’s Q2. Mueller has zero net debt.

The shares rallied 14.5% today. Over the last 30 years, Mueller is up more than 100-fold, and no one on Wall Street follows them. Sigh.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

By the way, if you haven’t already signed up for our premium newsletter, please join us today. It’s $20 per month or $200 for the entire year.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His