-

Questar (STR)

Posted by Eddy Elfenbein on June 17th, 2008 at 1:02 pmI’ll never understand why a company with a cool name like Mountain Fuel Supply Company would want to change its name to the horribly ugly sounding Questar (STR), but change it they did.

Perhaps they knew what they were doing. The stock has been an amazing performer for years. Over the last 20 years, the shares’ total return (including dividends) is up about 60-fold, which is over 22% a year. The stock hit another new high today.

-

FactSet’s Earnings

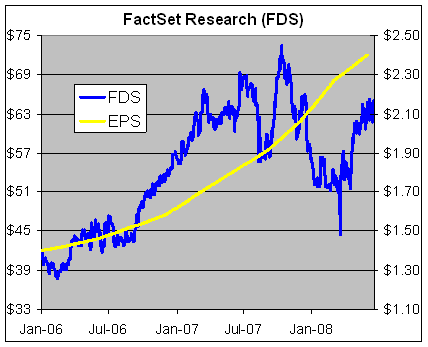

Posted by Eddy Elfenbein on June 17th, 2008 at 10:37 amVery strong earnings report today from FactSet Research Systems (FDS). Sales and net income both rose 22%. Earnings-per-share came in at 65 cents, two cents a head of the Street. For the same quarter one year ago, FactSet made 56 cents which included a four cent tax benefit.

Here are some highlights from the company:Other Financial Highlights

* U.S. revenues were $102 million, up 18% from the year ago quarter.

* Revenues from non-U.S. operations increased 30% to $45.7 million.

On a constant currency basis the increase was 29%.

* Operating margins were 32.5%, consistent with the previous and

year ago quarters.

* Other income declined 60% to $0.9 million from a reduction in U.S.

interest rates during the last nine months.

* Free cash flows generated during the quarter was a record

$45.8 million, exceeding the average of the previous four quarters

by $17 million.

Operational Highlights — Third Quarter of Fiscal 2009

* Users rose to 39,600 at quarter end, up 500 professionals over the

past three months.

* Client count was 2,044 at May 31, a net increase of 23 clients.

* PA 2.0 subscribers totaled 5,487 users from 607 clients at the end

of the quarter.

* Employee count at May 31, 2008 was 1,826. Headcount did not change

during the third quarter. The number of employees is up 18% over

the last year.

* FactSet already has accepted offers from 80 new employees for the

upcoming fourth quarter, the majority of which will expand the

sales and consulting and engineering departments.

* Capital expenditures were $12.3 million, net of landlord

contributions for construction. Expenditures for computer equipment

were $7.6 million and the remainder covered office space expansion.

* Client retention rate remained above 95%.

* On May 8, the Company’s Board of Directors approved a 50% increase

in the regular quarterly dividend from $0.12 per share to $0.18 per

share. The cash dividend of $0.18 per share will be paid on

June 17, 2008 to holders of record of FactSet’s common stock on

May 29, 2008.

* Common shares outstanding at May 31, 2008 were 48.0 million.Here’s a look at the company’s stock (blue, left scale) and earnings-per-share (gold, right scale). The two lines are scaled at 30-to-1. FactSet’s P/E ratio plunged from 37 in October to 19 in mid-March.

-

Hedge Fund Manager Still Alive, Fund Not So Much

Posted by Eddy Elfenbein on June 17th, 2008 at 10:12 amThe U.S. Marshals say that Samuel Israel III did NOT leap to his death after writing “suicide is painless” on the hood of his car.

Well done, Marshals, even though I could have told them that. The hood thing had all the earmarks of the first clue on any Law & Order. Please, no one is ever guilty at the 18th minute mark.“Suicide has been ruled out,” William Dundon, a spokesman for the U.S. Marshals Service, said in an e-mail to Reuters.

Another law enforcement official who is familiar with the investigation, but not authorized to speak publicly on the matter said “the investigation is solely a fugitive investigation now.”

Israel, 48, had been due to begin serving a 20-year prison term in Ayer, Massachusetts a week ago.

Officials would not say how authorities had learned that Israel, who suffers back and heart problems, was alive. But after no body washed up on the Hudson’s shores for days, police became skeptical he was dead.

In April, Israel was sentenced for fabricating investment returns, making up an accounting firm to sign off on documents and ultimately stealing $450 million from investors, including Indiana’s DePauw University.

He was out on bail to allow time for prison officials to prepare his medication, court documents show.

In an ironic twist, Israel’s disappearance may be especially awkward for his lawyers.

Lawyers at Morvillo, Abramowitz, Grand, Iason, Anello & Bohrer, P.C. defended Israel plus another fugitive, Jacob “Kobi” Alexander, the former chief executive of Comverse Technology Inc, who is wanted in the U.S. on stock-options backdating charges. Alexander escaped U.S. authorities in 2006 and has been living in Namibia since then.This is a good day for people who shorted the suicide contract. I wonder what the odds are that they’ll find Israel in Israel.

-

Little Bank, Big Profits

Posted by Eddy Elfenbein on June 16th, 2008 at 1:34 pmI love finding tiny companies that no one knows about, but are great investments. This is especially true with small banks. There are roughly a bazilion little banks that are publicly traded, and yet many aren’t followed by a single Wall Street analyst.

Here’s a good name to consider, Smithtown Bancorp (SMTB). The funny thing is that this bank is based in Wall Street’s backyard yet only two analysts follow it. The company has a market cap of roughly $200 million, which is barely a peep compared with the big boys (Citigroup’s market cap is more than 500 times larger).

Like a lot of banks, Smithtown is going through a rough patch, but the company still earned $1.47 a share last year. That was its 13th straight record year. Not a lot of companies can boast of that.

The shares are down about 15% in the past year. -

Say It Ain’t So, Lenny

Posted by Eddy Elfenbein on June 16th, 2008 at 1:19 pmForbes recently suggested that Lenny Dykstra isn’t making his own stock picks, but relying on Richard Suttmeier (note both Lenny, Suttmeier and I are columnists at RealMoney.com).

Peter Kafka prints Suttmeier’s response (you can read it here) and I think they have a good case. First, they’re not doing anything secretive or improper. Secondly, Dykstra is merely using Suttmeier’s research as a primary screening tool.Sheesh! What’s the big deal about that? -

Oil at $140

Posted by Eddy Elfenbein on June 16th, 2008 at 11:03 amThe price for oil is at another new record near $140 a barrel. A gas station in Egnland, however, is selling gas for just £1.99 pounds a litre.

Wait a sec, that’s $17.69 a gallon.

According to GasBuddy.com, Hume Lake Gas in Hume, CA is selling gas for $4.99 a gallon. -

“The US economy is Out of the Woods”

Posted by Eddy Elfenbein on June 16th, 2008 at 10:33 amAnatole Kaletsky at the Times argues that the U.S. economy is not in a recession:

American consumers, far from cutting back to bare essentials as was expected by bearish commentators after the credit crunch, are actually increasing their spending. The evidence of this, contained in the strong retail sales figures for May published last Thursday, was by far the most important economic news of the past few weeks. Yet these figures received almost no media coverage and little market attention.

Yet May’s retail sales figures revealed a picture completely at odds with conventional wisdom about the US economy. Despite the jump in energy prices and the related collapse in measures of consumer confidence, retail sales rose by 1.1 per cent on the month, the strongest gain since last November. Sales adjusted for inflation and excluding food and energy also showed gains much stronger than expected. Also April’s sales, initially thought to have fallen, were revised upwards to show a significant gain – and the two-month average of these volatile figures suggested that growth in the US consumer economy is now similar to the rate a year ago, before the sub-prime crisis and credit crunch.

This conclusion is not based on one set of good retail sales statistics, but includes stronger-than-expected recent figures on industry sales, stocks, imports, exports, purchasing managers’ surveys and even home sales. But in saying this, am I not forgetting about the dreadful employment figures published last Friday, which triggered the collapse of the dollar I mentioned at the start? Not at all. Despite the shock-horror headlines about a terrifying leap in unemployment from 5 to 5.5 per cent, employment figures for May were quite strong and fully consistent with the message of economic acceleration. Rates of unemployment are irrelevant in timing the economic cycle, since they are a lagging indicator, turning some six to nine months after the economy as a whole. Meanwhile, the job creation figures, which do reflect current economic conditions, showed a modest decline of 49,000 in payroll employment, exactly in line with expectations and consistent with the economy growing at about 1.5 per cent, just slightly below the 2 per cent trend rate of productivity growth.

Of course May’s strong retail sales were due in part to the tax rebates of $600 to $2,000 per household from the US Treasury from last month. Many analysts, therefore, dismissed the gains as misleading. But this was the wrong response. The role of tax cuts in boosting consumer spending is a reason for optimism, not scepticism, about the economic outlook. The tax rebates were designed to boost consumer spending and that is why we have always expected (in line with the Fed and the US Treasury) to see economic recovery from this summer. Retail sales figures have now shown that the US tax cuts are working as planned. They will temporarily boost consumption – and by the time that this temporary tax boost runs out around Christmas, the US economy will be starting to enjoy the benefits of lower interest rates, operating with a lag of 12 to 18 months. -

Lehman’s Earning, Or Lack Thereof

Posted by Eddy Elfenbein on June 16th, 2008 at 9:26 amLehman Brothers (LEH) told us to expect the worst and they were right. The company lost an astonishing $2.8 billion last quarter. Revenues came in at negative $688 million. It’s hard to make a profit when your revenue is in the red. The company got rid of $147 billion in assets last quarter.

Lehman’s leverage ratio — how many times assets exceed a firm’s equity — fell to 24.3 from 31.7 at the end of the first quarter and 28.7 last year. A week ago, Lehman predicted the ratio would slide to 25. The higher the number, the more debt the firm has taken on to fund those assets.

Lehman’s capital-markets business posted negative net revenue of $2.4 billion as fixed-income revenue fell to negative $3 billion. Both were in line with projections.

Equities revenue dropped 65% from a year earlier and 57% from the fiscal first quarter to $600 million, amid $300 million in losses on private equity and investments in which the bank was a principal.

The investment-banking business saw net revenue slump 25%. But investment-management revenue was flat at $800 million, worse than the company’s projection last week for a 13% rise to $900 million.

The brokerage said it has a liquidity pool of $45 billion, up 32% from the prior quarter.

Lehman said it reduced its exposure to residential mortgages, commercial mortgages and real estate investments by about 20% in each asset class during the quarter.From the end of 1996 to the end of 2006, shares of LEH climbed from $7.69 (adjusted for two 2-for-1 splits) to $78.12. That’s a 10-fold gain in 10 year, and it doesn’t include the modest amount from Lehman’s dividend.

The company just made a high-profile change in the executive suites but I really don’t think that’s what needed right now. Moody’s, for their part, recently downgraded the company. Naturally, this comes after the stock has plunged 75%. I doubt Lehman will able to continue as a separate entity. -

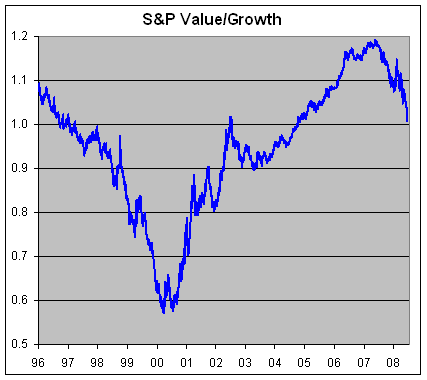

S&P 500 Value Index Divided By the S&P 500 Growth Index

Posted by Eddy Elfenbein on June 13th, 2008 at 11:48 am

Growth has recently been outperforming Value which is unusual for a bear market. The difference is that many financial stocks fall into the Value category, and that’s where the most pain has been. -

Portfolio Called It

Posted by Eddy Elfenbein on June 12th, 2008 at 2:11 pmFrom the April issue of Portfolio on Erin Callan:

Wall Street’s Most Powerful Woman

And why she might not rise higher than Lehman’s C.F.O.

- Load More

Costco 1st Quarter Revenues...

2025: $63 Billion

2020: $37 Billion

2015: $26 Billion

2010: $18 Billion

2005: $12 Billion

2000: $7 Billion

1995: $4 Billion

That's a 10% annualized growth rate over the last 30 years.

$COSTBezos once said: "The thing I've noticed is when the anecdotes and the data disagree, the anecdotes are usually right. There's something wrong with the way you are measuring it."

Applies to so much more than business. Never let a statistic blind you from seeing the naked truth…I imagine it would.

"New Stalin monument in Moscow subway stirs debate".

-

-

Archives

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His