-

-733.08

Posted by Eddy Elfenbein on October 15th, 2008 at 9:06 pmThe Dow dropped today by 733.08 points to close at 8577.91. That’s a loss of 7.87%. By percentage, this was worse than both October 9 (-7.33%) and September 29 (-6.98%). This was the worst day for the Dow since October 26, 1987, and it was the ninth-worst day ever. Three of the 19 worst days have come in the last 13 sessions.

The S&P 500 fell by 9.03% today which was much worse than the Dow. The Dow has outperformed the S&P 500 on all three big plunges. It also performed on October 7, which was only a drop of 5.11%.

The Dow has been steadily outperforming the S&P for nearly three years. In fact, last week the Dow-to-S&P ratio hit a 5-1/2 year high. The ratio hasn’t broken 9.5 yet, but it seems as if it’s about to. The ratio hasn’t been over 10 since 1966. -

Unitedhealth Group Moves Up Earnings Data

Posted by Eddy Elfenbein on October 15th, 2008 at 4:34 pmUnitedhealth Group (UNH) just said that it will report earnings tomorrow, instead of next week as originally planned. Something could be up, but I’ve lost a lot of faith in this company. Previously, the company said it expects 2008 EPS of $2.95 to $3.05. Since that translates to a P/E ratio of about 7, I don’t the market trusts them either.

-

Acceleration Matters

Posted by Eddy Elfenbein on October 15th, 2008 at 2:54 pmHere’s a look at some historical data of the S&P 500 since 1950.

The day after a down day, the S&P 500 has dropped at annualized rate of 12%. The day after that, it’s risen at an annualized rate of 11.3%.

The day after an up day, the S&P 500 has climbed at an annualized rate of 27.9%. The day after that, it’s risen at an annualized rate of 4.3%.

So in both cases we see a reversion to the long-term trend, and interestingly, both show next-day adjustments of about 23%.

After two consecutive down days, on the third day, the market drops at an annualized rate of 8.5%. But if the second day’s drop is greater than the first day’s, then the third-day loss is at an annualized rate of 17.8%. If the second day’s drop is less then first, then the third day shows a small annualized gain of 4%.

After two consecutive up days, the market rises at annualized rate of 21.8% on the third day. Here’s comes the kicker: If the second day’s gain is greater than the first, then the market gains an annualized rate of 42.2% on the third day. If the second day’s gain is less than the first, the third day’s gain is just 5.6%.

Acceleration matters, but it’s not everything. Turnarounds are also very good.

When the market goes down, then up, the third day’s gain is an annualized 36.6%. In fact, that represents nearly the entire gain of the stock market even though those days come about less than one-quarter of the time.

On down-then-up occasions, when the second day’s gain is greater than the first day’s loss, then the third day gains an annualized 49.8%. When the second day’s gain is less than the first day’s loss, the third day gains merely 24.1% annualized. -

Roubini Hasn’t Been So Correct

Posted by Eddy Elfenbein on October 15th, 2008 at 11:45 amIf you keep predicting a recession, eventually you will be right. Every time there was the slightest downturn in the numbers, Paul Krugman predicted a recession. Eventually he was right. Do we give him credit for the one he got right, or the multiple ones he got wrong? To liberals, the answer seems obvious. Which gives credence to the conservative belief that liberals are people who cannot do basic math.

A more interesting question is what to do about doomsayers like Nouriel Roubini, who got the magnitude of the crisis right, but has similarly been predicting a financial holocaust for five years, with changing scenarios which mostly did not come to pass. Obviously, he was right that the global financial system was shaky. On the other hand, his understanding of why the global financial system was shaky does not seem to have been strong enough to predict the source of the failure–the current account deficit and the dollar have been at best minor players, at least in the way that he was worried about way back in 2004.Finally, someone is criticizing Roubini. His status as a financial visionary is wholly undeserved. He’s been screaming about the downfall of capitalism for years now.

Here’s my complaint about making predictions–there’s a lack of balance. Basically, you can call for the world to end for years, then step back and take any crisis and claim vindication. It’s like the people who said they were right about Iraq. But the disaster they saw coming was millions of Arabs rushing to Saddam’s side and a Stalingrad-like siege of Baghdad.

Also, Robert Shiller is a similar story. He never said what people think he said about the stock market. But if you make a bullish prediction and you’re wrong, well then forget about it. Glassman will forever be linked to Dow 36,000. His mistake was being specific. In June 2003, Krugman said the stock market was in a bubble, and he was fantastically wrong. Yet that disappears down the memory hole.

So here’s the lesson, if you ever make a forecast always be gloomy and vague. -

Money Galore

Posted by Eddy Elfenbein on October 15th, 2008 at 9:47 amThis month’s Portfolio estimates that the James Bond franchise has generated nearly $14 billion in profits. The authors estimate that $12 billion came from the movies, $812 million from video games and $1 billion from books.

-

Pennies From Heaven

Posted by Eddy Elfenbein on October 14th, 2008 at 1:42 pmDoes the weather affect market volatility? Apparently, the answer is yes.

The relationship between the weather and stock market returns has been well documented both empirically and theoretically. We extend this literature by considering for the first time the impact of weather conditions on stock market volatility. Specifically, we analyze historical volatility using the extensive data set of Hirshleifer and Shumway (2003) which consists of daily measures of cloudiness along with stock market index returns for 26 stock exchanges internationally between 1982 and 1997. The empirical results suggest that sunnier mornings can be associated with higher levels of time-varying market risk as approximated by the conditional daily volatility of returns from GARCH and EGARCH models. The analysis of the VIX, VXO, VXN and VXD implied volatility indices for the CBOE offers further support to this finding.

-

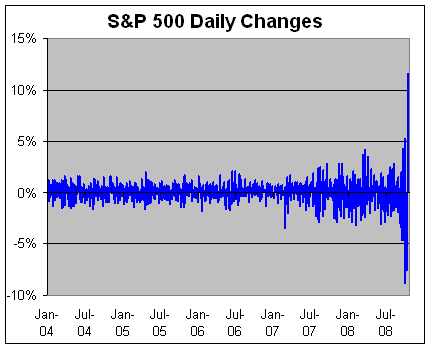

S&P 500 Volatility

Posted by Eddy Elfenbein on October 14th, 2008 at 12:36 pmI’ll spare you 1,000 words and give you the picture.

-

Nassim Nicholas Taleb Gets Angry

Posted by Eddy Elfenbein on October 14th, 2008 at 11:03 am

I think I’m one of very few people who isn’t impressed by Nassim Nicholas Taleb. I have the suspicion that The Black Swan is one of the great unread books of modern times. I can’t prove this, but I’ve read the book and it’s one of the most arrogant and incoherent books I’ve ever read. The Black Swan is so bad that it’s nearly unreadable.

Taleb really has one idea—that financial market returns don’t follow a normal distribution. OK, I got it. That’s all that he’s complaining about in this clip. For the record, this isn’t Taleb’s idea. A much better book is Benoit Mandelbrot’s, The Misbehavior of Markets.

At around five minutes into the clip, the interviewer asks, “Climate change, civil liberties, do these now go out the window in the face people losing their jobs and homes?” Yes deary, that’s exactly what it means.

Here’s a short review I did of The Black Swan. -

J&J Beats the Street

Posted by Eddy Elfenbein on October 14th, 2008 at 10:05 amWell, not everything is a disaster out there. Johnson & Johnson (JNJ) just reported earnings of $1.17 a share, six cents better than estimates. The company also raised its full-year guidance, which sounds more impressive than it is since there’s just one quarter left this year. But still, they’re holding out well against the Apocalypse. On Friday the stock traded as low as $52.06. Today, it’s over $65.

-

Wreck-javik

Posted by Eddy Elfenbein on October 14th, 2008 at 9:53 amPoor little Iceland. The country is probably best described as a hedge fund with a vote in the UN. The stock exchange there was shut down for three days and it just reopened. Down 77%.

Kaupthing Bank hf, Glitnir Bank hf and Landsbanki Islands hf collapsed this month with debts equivalent to as much as 12 times the size of Iceland’s economy. The three banks accounted for about 76 percent of the ICEX 15 Index’s value prior to the nationalization.

The OMX Iceland 15 Index fell 2,317.23, or 77 percent, to 687.39 as of 11:48 a.m. local time. Five of the 13 other stocks in the index didn’t trade, while the five that did account for about 7.1 percent of the index’s value.

Trading was halted since Oct. 9 after the measure lost 30 percent in nine days as the country’s financial system collapsed. Iceland’s delegation started talks in Moscow today to secure an emergency loan of as much as 4 billion euros ($5.47 billion) from Russia.

The country should seek aid from the IMF and later apply for European Union membership and adopt the euro, Foreign Minister Ingibjorg Solrun Gisladottir wrote in Morgunbladid on Oct. 13.

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His