-

Headline of the Day

Posted by Eddy Elfenbein on October 9th, 2008 at 10:40 amFrom the Register:

Oracle shareholders choke on Ellison’s package

Size an issue -

Great Moments In Government

Posted by Eddy Elfenbein on October 8th, 2008 at 9:16 pmSeptember 19, 2008:

S.E.C. Temporarily Blocks Short Sales of Financial Stocks

Financial Select Sector SPDR (XLF) closes at $22.38October 1, 2008

S.E.C. Extends Ban on Short-Selling

Financial Select Sector SPDR (XLF) closes at $20.67October 8, 2008

A Debate as a Ban on Short-Selling Ends: Did It Make Any Difference?

Financial Select Sector SPDR (XLF) closes at $15.28 -

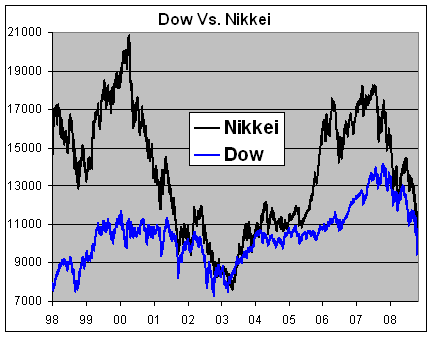

Chart of the Day

Posted by Eddy Elfenbein on October 8th, 2008 at 3:34 pm

-

Sad Guys on Trading Floors

Posted by Eddy Elfenbein on October 8th, 2008 at 2:56 pm

The latest blog, nothing but pictures of sad guys on trading floors.

(Via: Ritholtz) -

The British Bank Bailout

Posted by Eddy Elfenbein on October 8th, 2008 at 2:48 pmI just got back from being on Britain’s SkyNews where I mentioned that Britain’s policy today is better than the Paulson plan, at least in the eyes of taxpayers.

British policy, until now, has been far too reactive and unimaginative. The key difference is that under today’s plan, British taxpayers get a stake in the banks through preferred stock in exchange for loaning banks money. What banks needs is an injection of capital. I think it will be interesting to see how many banks that have hitherto claimed perfect health will start crawling towards the government’s money line.

The key advantage in our takeover of Fannie and Freddie is that we fire management. Some CEOs in Britain deserve the same fate. I should add that I’m not one who’s terribly worried about the issue of CEO compensation. When the conversation involves trillions, we can worry about millions latter. -

Americans’ Satisfaction at All-Time Low of 9%

Posted by Eddy Elfenbein on October 8th, 2008 at 12:24 pmYikes! According to Gallup, just 9% of Americans are satisfied with the way things are going in the U.S. right now.

The previous low point for Gallup’s measure of satisfaction had been 12%, recorded back in 1979, in the midst of rising prices and gas shortages when Jimmy Carter was president. Gallup has recorded a 14% satisfaction level at several points — once in the senior Bush’s administration in 1992, and several times earlier this year.

The reason for Americans’ extraordinarily low level of satisfaction is straightforward: the economy. Asked in the weekend Gallup Poll to name the most important problem facing the country today, almost 7 in 10 Americans mentioned some aspect of the economy, far ahead of any other problem mentioned.I always thought with polling you could get 15%-20% to agree with any statement. I mean, how many people think Elvis is alive?

-

China to the Rescue

Posted by Eddy Elfenbein on October 8th, 2008 at 11:33 amKen Rogoff suggests a plan:

The Chinese government could offer to lend up to $500bn (from its current stock of $1,800bn) to the US government for the rescue of its financial sector. Its previous assistance – buying US bonds – was indirect and unconditional. Not so in this case.

China’s loan offer would be direct to the US government to be spent in the current financial crisis. More important, it would come with strings attached. Tied aid, the preferred mode of operation of western donors since the postwar period, would now be embraced by China.

What would be the nature of the strings – or “conditionality” as the US Treasury, a longtime practitioner of this art, has called it? Conditionality as imposed by the World Bank and International Monetary Fund was underpinned by an ideology that favoured markets and globalisation. But there was also an assumption that either borrowing third world governments did not understand their benefits or the reformers there needed a “spoonful of sugar” to help overcome any internal opposition.

China would impose two conditions. First, it would declare that the offer of money was conditional on the US government’s adopting a particular approach to rescuing the banks, namely to favour in the next round the use of government money to recapitalise the banks. Europe has been using this approach and evidence suggests it is the most effective way of dealing with large-scale financial crises.

The US government – like third world governments in the past – has been unable to adopt the most efficient course of action. This stems from an ideological obsession against “socialising” banks or because inducement is necessary to overcome any domestic opposition to it.

The second condition would relate to “social safety nets”, which had become standard embellishments to World Bank/IMF adjustment programmes. China would stipulate that monies be devoted to cushioning the impact on vulnerable homeowners, so that they would not be forced into forgoing the American dream of home ownership. Chinese conditionality on this front would achieve an outcome that several economists on the left and right have argued for on grounds of fairness, and also to address the fundamental problem in the housing market.

For China, this offer of help would have three virtues. First, it would be riding to the rescue of a situation partly created by its own policies of undervalued exchange rates, which led to lax global liquidity conditions. Second, its economic interest would be served because successful US efforts at rescuing its financial sector could help avert an economic downturn, protecting China’s exports, its growth engine.

Perhaps most important, it would seal China’s status as a responsible superpower willing to deploy its economic resources for the sake of protecting the world economy. And if the means for achieving that are by providing the current hegemon with the largest aid package the world has ever seen with a healthy dose of sensible conditionality, well, what could be more statesmanlike than that? -

The S&P 500 Broke 1,000

Posted by Eddy Elfenbein on October 7th, 2008 at 4:00 pmFor the first time in five years, the S&P 500 closed in three-digit territory. The index closed today at 996.23.

-

Phases of the Moon and the Stock Market

Posted by Eddy Elfenbein on October 7th, 2008 at 11:26 am

Some people think it’s merely a coincidence. Those people would include me. -

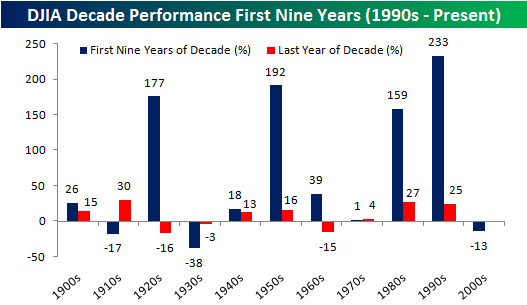

The Worst Decade Since the Thirties

Posted by Eddy Elfenbein on October 7th, 2008 at 11:11 amBespoke points out that this decade has been one of the worst in history for stock returns:

Unless we get a major rally to close out the year (15%+), this will only be the third time since 1900 that the Dow Jones posted negative returns in the first nine years of a decade (excluding dividends).

-

Archives

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His