-

More Than You Ever Cared to Know About P/E Ratios

Posted by Eddy Elfenbein on May 21st, 2008 at 12:40 pmI want to expound on what I said the other day about the use of Price/Earnings Ratios. It works like this, picking stocks (good), timing the market (bad).

I also criticized the idea of using P/E ratios based on ten years’ worth of earnings. Now I want to show you why.

First off, I got this historical data off Robert Shiller’s website which has monthly numbers going back 140 years.

Now I have to explain my analysis carefully, and I have to apologize because it’s not easy to do. Plus, whenever I attempt this, I get dozens of emails asking what the hell I’m talking about. (Note, dear reader, I’m criticizing my articulational abilities, not your comprehensional skillz.)

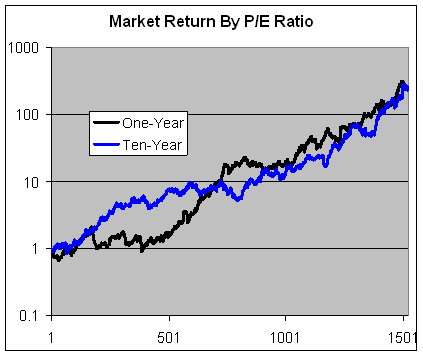

Deep breath. I take all of the monthly data of stock market returns and P/E ratios. I then resort the data, not by time, but this time by P/E ratio, highest to lowest. Then, I calculate all those individual monthly returns. Basically, it’s a stock market graph, not by time, but by declining P/E ratio.

If the P/E ratio has an impact on the market, I would expect the line to droop down early on, then rally frenetically with lower ratios. If the P/E ratio has no impact, then I expect that the line would rise in a smooth diagonal line. Here’s a look at how the 10-year and 1-year P/E Ratios stack up:

As you can see, the 1-year P/E ratio has some impact on market returns, but not much. The market shows a net loss up to the 390th data point which corresponds to a P/E ratio of about 17.8. That means that all over the market’s net gains have come when the P/E Ratio is less than 17.8. According to Shiller’s data, that’s almost the entire time since 1996.

Still, I’m not impressed by the one-year’s performance. Compare that to this dramatic graph showing the market’s performance ranked by the previous day’s gain.

The 10-year P/E has, in my opinion, almost no impact on equity prices. The blue line barely wiggles on its way down the P/E Ratio scale. Knowing what the 10-year ratio was gave you zero input on what stock prices were about to do. -

Hauser’s Law

Posted by Eddy Elfenbein on May 21st, 2008 at 10:22 amIn yesterday’s WSJ, David Ranson has a bizarre article expounding on, what he calls, Hauser’s Law, which is named in honor of economist Kurt Hauser. The law states: “No matter what the tax rates have been, in postwar America tax revenues have remained at about 19.5% of GDP.”

And the article includes this nifty chart:

Zubin Jelveh goes off on the chart because it implies that the variation in marginal rates have zero impact on the bottom line. It’s true that other taxes besides income taxes have played an increasingly significant role in U.S. tax policy. But what I understood Hauser’s Law to mean is that none of that matters. The tax code will always produce the same amount.

I’m fairly sympathetic to rules like Hauser’s Law. Especially with social sciences, I tend to believe that there situations where no matter what the rules are, they’ll produce the same results. (Some of you may recall Elfenbein’s 17th Law which states that U.S. GDP growth has been remarkably stable over the last 40 years and about 3.1%.)

The problem I have with Hauser’s Law is that it doesn’t seem to include state and local taxes, which should raise the bar by quite a lot. Also, why should we look to the nation as a whole? To find out if there’s an upper limit, I think we should look at what state has the highest rate. For that matter, perhaps we should look at foreign countries.

While tax revenues may been fairly stable over the past 50 years, that doesn’t mean we couldn’t generate more if we wanted to.

-

Scary Government Fact of the Day

Posted by Eddy Elfenbein on May 20th, 2008 at 4:34 pmFrom Megan McArdle:

If you want to know just how ridiculous our agricultural programs are, consider this: for about half a century, we priced milk based on how far the cow was from Eau Claire, Wisconsin. No, I swear, I am not making this up. Apparently, the USDA scientifically determined that Eau Claire was the perfectest place in the entire world to keep cows, and that therefore the farther you were from that fabled city, the harder you must find it to produce milk.

-

Inflation Watch: $175 Burger on Wall Street

Posted by Eddy Elfenbein on May 20th, 2008 at 2:11 pmForget about $130 oil, there’s a $175 burger.

The burger can be enjoyed at the Wall Street Burger Shoppe on Water Street between Broad Street and Coenties Slip.

Kevin O’Connell, the restaurant’s co-owner and chef, told WCBSTV.com he came up with the idea when a friend suggested he create a luxurious version of the American classic.

“He kind of challenged me and it was a question of how do you make a burger that was worth that kind of money,” he said. “It actually turned out to be a really awesome thing to eat.”

The burger is made with Kobe beef and topped with seared fresh foie gras, an assortment of exotic mushrooms, shaved black truffle, and golden truffle mayonnaise – another of his creations made from chopped black truffles, truffle oil, and gold flakes. -

Investing on the First Day of the Month

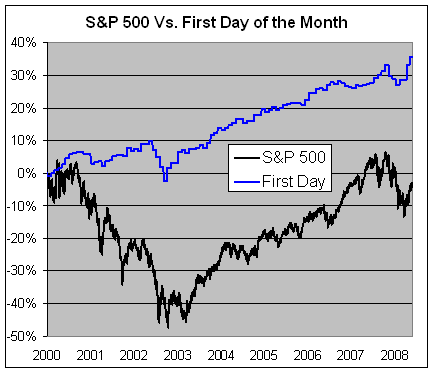

Posted by Eddy Elfenbein on May 20th, 2008 at 11:12 amSince the start of this decade, the S&P 500 is now down -2.9% (toss in dividends, it’s up +11.7%). However, investing in just the first day of the month has delivered a return of 35.4%.

I should add that the out-performance is not just due to the market’s implosion at the beginning of the decade. As market turned around, the first day of the month held its own. From March 11, 2003 to October 9, 2007, the S&P 500 gained 95.5%. The first day of the month gained 25.2%.

That’s a pretty heft contribution from just one day in the month. Consider that on the trading calendar, the first day of the month is less than 5% of the time. -

Tanta on Robert Shiller

Posted by Eddy Elfenbein on May 20th, 2008 at 10:25 amTanta at Calculated Risk has a great post on Robert Shiller’s recent editorial in the New York Times. I’ve often taken exception to Shiller’s arguments. I believe that too often he sees bubbles are serious defects in the economy, and they’re the result of the moral failings of the public. Me? I just think bubbles happen. Anyway, give Tanta a read.

-

New Book to Hate

Posted by Eddy Elfenbein on May 20th, 2008 at 10:13 amMalcolm Gladwell is coming out with a new book. Here’s the blurb at Amazon:

In this stunning new book, Malcolm Gladwell takes us on an intellectual journey through the world of “outliers”–the best and the brightest, the most famous and the most successful. He asks the question: what makes high-achievers different? His answer is that we pay too much attention to what successful people are like, and too little attention to where they are from: that is, their culture, their family, their generation, and the idiosyncratic experiences of their upbringing. Along the way he explains the secrets of software billionaires, what it takes to be a great soccer player, why Asians are good at math, and what made the Beatles the greatest rock band.

Brilliant and entertaining, OUTLIERS is a landmark work that will simultaneously delight and illuminate.I shouldn’t say I hate the book before it comes out, I’m just a little skeptical of Gladwell’s approach to things. He’s a big fan of CONCEPTS and he has a tendency to see the application of his CONCEPTS everywhere. When in fact, these CONCEPTS really don’t have the ability to leap with ease into many different fields. What Gladwell really does is write intellectual fast food for the NPR set.

(Hat Tip: Weisenthal) -

Just a Quick Observation

Posted by Eddy Elfenbein on May 20th, 2008 at 10:11 amWhen did the NBA playoffs become the sports of equivalent of Stalingrad? With yesterday’s Spurs victory, the playoffs are now officially half over. But the final regular season game happened five weeks ago from tomorrow. We still have more than one month to go. What the hell takes them so long?

The Spurs and Hornets played their sixth game on Thursday, then took off Friday, Saturday and Sunday, to play the seventh game on Monday. On top of that, the first round is almost completely unnecessary. All eight lower ranked teams won. In the second round, three of the four lower ranked teams won. The only exception was the Spurs beating the Hornets. Although the Hornets had the #2 seed, the teams had the same regular season record.

Can’t we do away with at least one round? As a point of principle, I don’t think a team with a losing record should ever be allowed to make the playoffs.

OK, rant over. -

Jay Leno on Cars

Posted by Eddy Elfenbein on May 19th, 2008 at 8:52 pmFirst, Portfolio got Tom Wolfe to write in their inaugural issue. Now a bigger coup — Jay Leno writes about cars:

The type of vehicles America makes best are, unfortunately, not the type of vehicles that people really want anymore. Nobody builds better trucks than the Americans do. Not even the Japanese build as good a truck as the Ford F-150 or the Chevy Silverado. It’s the same with performance cars. The Corvette Z06 has 505 horsepower, comes with a big warranty, and can hit 200 miles per hour. It weighs almost exactly the same as a half-million-dollar Porsche Carrera GT and gets higher mileage—26 miles per gallon.

Where we seem to lose it is in the low-bucks econocar. I used to be able to identify any American car from 25 yards. Now they all have this jellybean look. It’s a mystery to me, because the one thing we used to do better than anybody else was build cheap, extremely high-quality cars. We did it for decades, all the way back to the beginning of the industry. There was no better car for the money than the Model T. It was a basic car, but it used the finest materials available. There are still almost a million of them out there.

When you get into a high-priced, well-made American car today and the key is in the ignition, you hear a melodic bong, bong. But when you get in a cheap American car, like a rental, and the key is left in, it goes plink, plink, plink. It’s just horrible. Every time you use the turn signal, it’s like breaking a chicken leg. In order to make the more expensive car more appealing, U.S. companies feel as though they have to dumb down the cheaper car. -

The Market By Days of the Week

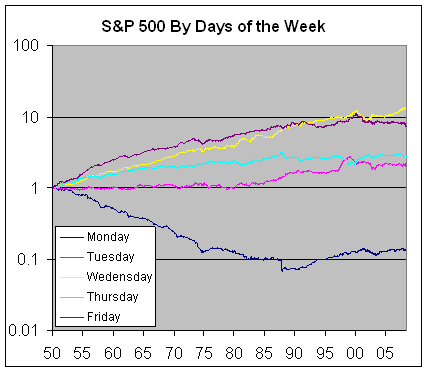

Posted by Eddy Elfenbein on May 19th, 2008 at 5:21 pmSince 1950, the S&P 500 is down on the combined days of Monday, Tuesday and Thursday. All of the indexes gains have come on Wednesday and Friday (dividends not included).

Here are the combined gains:

Monday -86.43%

Tuesday 125.23%

Thursday 184.30%

Friday 656.15%

Wednesday 1,201.75%

Since May 16, 1998 the breakdown is as follows:

Friday -13.25%

Tuesday -11.51%

Monday 11.13%

Thursday 13.41%

Wednesday 32.87%

This means that all of the net capital gains for the past 10 years have come on Wednesdays which is just 20% of the time (that’s 32.87% for Wednesday, -3.24% for the other four days combined).

- Load More

You can do very well by betting on the big winners before they became the big winners.

"Japan’s births mark record low in 2024, plummet below 700,000." They predicted it would get here by 2039 but made it 15 years early. ?

Florida's Housing Market 'Turning Down Fast'

-

-

Archives

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His