-

The Long Shot

Posted by Eddy Elfenbein on March 20th, 2008 at 7:47 amMatthew Yglesias comments on the absurdity of John Meriwether blowing up, yet again. He includes this parable:

Imagine I find a kind of gambling machine somewhere that works kinda sorta like an enormous roulette wheel. It has 100,000 possible outcomes, and on 99,999 of those outcomes it pays off at a 1:1 ratio. But on the 100,000th outcome, you lose at a 1:300,000 ratio. Obviously, placing a bet on that machine would be foolish.

Not to me.

I’d lay down $1,000, let it roll for 20 spins and walk away a billionaire.

Addendum: Or there’s a very remote chance that I’d go in the roulette business. I’d be cool with either outcome. -

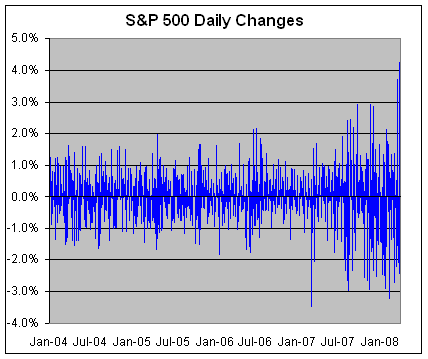

The Return of Volatility

Posted by Eddy Elfenbein on March 20th, 2008 at 7:42 am

According to a recent report by S&P, market volatility is at a 70-year high. I think that’s merely going by 1% daily changes. Other measurements indicate that volatility has indeed risen, but it’s more accurate to say that volatility has returned to normal from an unusually calm period.

The VIX still hasn’t reached the heights of 1998 to 2002. The index has closed above 30 for a few times recently, but it did it fairly regularly a few years ago.

I think the effect of volatility on equity returns is not very strong. The current VIX seems to have an effect on the dispersion of returns, but not the direction. -

How NCAA Tournament Seeds Have Fared

Posted by Eddy Elfenbein on March 19th, 2008 at 7:45 pmThe Chicago Tribune looks at how the NCAA tournament seeds have fared since 1985. I love the idea of a big tournament that invites a huge number of teams. It seems the most democratic, but there are some gaps in justice. For example, the #8 or #9 seed is really screwed because they always must play a #1 in the second round. Only 12 #8 or #9 teams have made it past the second round.

On the other hand, #12 is a pretty good seed. Those teams have a losing, but respectable record against the #5 seeds. A total of 14 number #12 seeds have made it past the second round.

My guess is that the seeds increase linearly while quality increases geometrically. The difference between a #12 and a #5 is probably about the same as a #1 and a #3.

If we wanted to be hard-headed, we could really make it a 12-team tournament and the results would be almost the exact same. Twenty of the 23 winners have been #1, #2 or #3 teams. Of course, that would ruin a lot of the fun.

I’ve noticed that no matter what happens, the media talks about how the first weekend was a “Cinderella Weekend.” But going by history, there’s nothing that surprising by having at least one #14 beat a #3, or having a #2 or #3 lose in the second round.

It’s fun to root for the Cinderella teams (we have a couple of local teams ranked in the double-digits), but history says that the odds are against them. -

“Mama – just killed my fund”

Posted by Eddy Elfenbein on March 19th, 2008 at 4:57 pmSung to the tune of ‘Bohemian Rhapsody‘ by Queen

Is this the real price?

Is this just fantasy?

Financial landslide

No escape from reality

Open your eyes

And look at your buys and see.

I’m now a poor boy (poor boy)

High-yielding casualty

Because I bought it high, watched it blow

Rating high, value low

Any way the Fed goes

Doesn’t really matter to me, to me

Mama – just killed my fund

Quoted CDO’s instead

Pulled the trigger, now it’s dead

Mama – I had just begun

These CDO’s have blown it all away

Mama – oooh-hoo-ooo

I still wanna buy

I sometimes wish I’d never left Goldman at all.

(guitar solo)

~~~

I see a little silhouette of a Fed

Bernanke! Bernanke! Can you save the whole market?

Monolines and munis – very very frightening me!

Super senior, super senior

Super senior CDO – magnifico

I’m long of subprime, nobody loves me

He’s long of subprime CDO fantasy

Spare the margin call you monstrous PB!

Easy come easy go, will you let me go?

Peloton! No – we will not let you go – let him go

Peloton! We will not let you go

(let him go !)

Peloton! We will not let you go – let me go

Will not let you go

let me go (never) Never let you go – let me go Never let me go – ooo

No, no, no, no, No, NO, NO ! –

Oh mama mia, mama mia, mama mia let me go

S&P had the devil put aside

for me

For me, for me, for me

~~~

So you think you can fund me and spit in my eye?

And then margin call me and leave me to die Oh PB – can’t do this to me

Just gotta get out – just gotta get right outta here

Ooh yeah, ooh yeah

No price really matters

No liquidity

Nothing really matters – no price really matters to me

Any way the Fed goes…..(Hat Tip: Ritholtz)

-

The Three-Month T-Bill Now Yields 0.5%

Posted by Eddy Elfenbein on March 19th, 2008 at 2:29 pmI don’t know what to say. If you invest one million dollars, that works out to a yearly gain of $5,000.

The government can now rent $70,000 a day for the grand total of $1.

-

A Couple of Bookies

Posted by Eddy Elfenbein on March 19th, 2008 at 1:06 pmIn the movie Trading Places, the Duke brothers explain to Eddie Murphy the essence of their investment business. Murphy shoots back, “You two sound like a couple of bookies to me.”

He’s right; fundamentally, it’s the same idea. Now Bloomberg has a story about one Wall Street’s firm’s growing interest in gambling. Cantor Fitzgerald has a Cantor Gaming unit that’s involved in sports books.

Bloomberg writes:The firm is seeking Nevada state approval for field tests of a handheld device for playing digital card games and roulette in a casino’s public spaces, such as pools and nightclubs. Officials of closely held Cantor Fitzgerald say it could eventually be used anywhere.

It makes sense for them to be involved in this. Basically, their business is math. I believe that I once read that the entire field of statistics has always been driven by gambling.

“It’s all about processing,” said Lee Amaitis, 57, head of Cantor Gaming, from London. “All you’re doing is math. If you have an engine that can drive random generating results, you can process bets.”

-

Up In Smoke

Posted by Eddy Elfenbein on March 19th, 2008 at 11:40 amAttendees say Mr. Cayne has sometimes smoked marijuana at the end of the day during bridge tournaments. He also has used pot in more private settings, according to people who say they witnessed him doing so or participated with him.

Dow Rises 420 Points

-

Re: “Bear Stearns is fine.”

Posted by Eddy Elfenbein on March 19th, 2008 at 8:20 amThere’s some controversy surrounding Jim Cramer’s “Bear Stearns is fine” comment from last Tuesday. Cramer has said that he was referring to Bear Stearns as a depository institution, not as an investment. He claims that he was telling the questioner that his money was safe at Bear Stearns’ money management arm. Cramer also says that he called Bear’s stock “worthless “on Friday.

Mick Weinstein at Seeking Alpha, whom I respect greatly, agrees with Cramer. I’m sorry but it doesn’t wash with me. Let me say that I think it’s very possible that that what’s Cramer intended. But, to a reasonable person, there’s no reason to see it that way.

Mad Money is a show dedicated to Cramer’s discussion of stocks. That’s the appeal. Only a few times have I heard him discuss larger money management issues. Plus, there was a stock chart of BSC up on the screen. That strongly implies to an average person that he meant the shares.

If he was referring to Bear’s deposits, Cramer didn’t mention basic facts, like you should immediately speak with your broker, or check up on the firm’s deposit insurance. Anyone who has spent five minutes studying for a Series 7 knows about SIPC. At no point did Cramer make an effort to clear up would could be confusing. Plus, he goes the extra step of saying that “Bear Stearns is not in trouble.”

In today’s WSJ, James Stewart writes that “Bear Stearns didn’t have a retail brokerage operation and didn’t cater to individual investors.” The firm did (and I suppose, does) have a small retail operation but that’s only for high net worth individuals. I looked at Bear’s website and they don’t even have an office here in Washington, DC. Once any trouble hit, I would think that those brokers informed their clients as soon as possible. In high-net worth money management, clients aren’t typically kept in the dark. -

Raise the Price

Posted by Eddy Elfenbein on March 19th, 2008 at 8:08 amI really don’t see how Bear shareholders will approve the $2 deal. Apparently, I’m not alone. The stock is currently at $6 and it went as high as $8 yesterday.

Part of that the buying is being driven by BSC creditors (hedge funds, mainly) who don’t mind taking a small equity loss in exchange for a big debt gain—they just want the deal done. No one knows how much equity Bear truly has, but there’s around $300 billion of Bear Stearns bonds out there. If the whole mess goes to a bankruptcy court, then the stock holders go to the back of the line.

Of course, the debtor’s strategy could backfire if the price goes too high and JPM gets cold feet. Still, I doubt that would happen. As always, one shouldn’t fight the Fed.

I would say that the most likely outcome is that JP Morgan will sweeten the offer. To add some context, it’s really not that much for them. The company’s market value has already increased by $20 billion this week. The offer for Bear will cost them $236 million. What’s the big deal if they double or even triple it? Plus, it could win them some goodwill. Dimon is a very smart guy, and it might be a shrewd move to get out in front of what could become very unpleasant. If I were him, I’d meet with Joe Lewis, Legg Mason and other major BSC holders. He’s already won big. He can afford to be magnanimous.

On top of that, let’s not forget that JPM owns a gigantic call contract of whenever-$2s, and there’s also the building deal. Plus, it’s not unreasonable for the U.S. credit market to recover over the next few weeks. That could be a huge boon for BSC’s debt. To quote Michael Scott, it’s win-win-win. In fact, taxpayers could win as well.

I think we ought to move beyond the question of whether the Fed should be involved in—what I’ll call—a quasi-bailout. Instead, let’s look at the deal that was made, and it makes JPM look Putin-esque. The WSJ reminds us that it’s not uncommon for the government to make money off bailouts:During the 1995 peso crisis, the Clinton administration offered Mexico $20 billion in loans, with the country’s oil revenues as security. The International Monetary Fund offered another $18 billion. Critics condemned the loans as a bailout. In the end, Mexico didn’t require the entire amount, and the country’s finances recovered. The U.S. ended up making a profit on the interest payments.

The government also turned a profit from the Air Transportation Stabilization Board, an entity set up after the Sept. 11 attacks to support the airline industry. The board ultimately provided a total of $1.56 billion in loan guarantees to six carriers. The government earned just under $350 million from fees and stock sales, according to the Treasury Department.Last year, the Fed made a profit of $34 billion. It’s very possible that the central bank could make money on whatever they’ll get from Bear’s book. I still don’t understand who gets what. This seems to be a classic case of we don’t know what we don’t know. Perhaps the best move for the Fed is to hold the bonds to maturity.

-

Has Bill Miller Lost His Magic

Posted by Eddy Elfenbein on March 19th, 2008 at 7:42 amLegg Mason Value Trust (LMVTX) has badly lagged the market since the beginning of 2006. It has only gotten worse recently.

- Load More

You can do very well by betting on the big winners before they became the big winners.

"Japan’s births mark record low in 2024, plummet below 700,000." They predicted it would get here by 2039 but made it 15 years early. ?

Florida's Housing Market 'Turning Down Fast'

-

-

Archives

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His