-

When Investor Activism Doesn’t Pay

Posted by Eddy Elfenbein on September 13th, 2007 at 9:48 amShareholder activism has become quite a buzzword in recent years. But a recent study found that it’s not always such a good idea:

The study by a Harvard Business School assistant professor, Robin Greenwood, and Michael Schor, a former student, found that activist funds are like a boxer with one punch: They are most successful when they prod managers to put a company up for sale. Shares of the target company typically rise, and all shareholders benefit.

But the authors found that activist investors have much less impact when a targeted company isn’t sold. In those cases, the study found there is little change in the next 18 months in the company’s stock price or financial results. That is true even when the company takes steps recommended by the activists, such as firing the chief executive, buying back stock or adding new directors.

“The money is in getting the target acquired,” Mr. Greenwood says. “The ones that don’t end up getting acquired don’t end up with much of anything.”That’s an interesting view and I’m not terribly surprised. Carl Icahn didn’t get much from Time Warner. I would also think that shareholder activism would have some effect on closely-hold companies, especially by families (like Dow Jones). That’s just my hunch but I think you would find greater complacency there.

-

Oil Hits $80

Posted by Eddy Elfenbein on September 12th, 2007 at 3:26 pmOil hit an all-time high today of $80.18. But adjusted for inflation, we still have more to go.

Prices rose from 1979 through 1981 after Iran cut oil exports. The average cost of oil used by U.S. refiners was $37.48 a barrel in March 1981, according to the Energy Department, or $84.73 in today’s dollars.

-

Jos A Bank’s Earnings

Posted by Eddy Elfenbein on September 12th, 2007 at 11:11 amJos A Bank Clothiers (JOSB), the most erratic stock on our Buy List, just released very good second-quarter earnings. Sales rose 12% to $119 million and EPS came in at 44 cents a share which is a nice improvement over the 38 cents from last year. Wall Street was looking for 42 cents a share.

Actually, breaking down the numbers, JOSB earned 44.49 cents per share. If they earned just $2,000 more, the number would round up to 45 cents per share.

I’ve always noticed a tendency for EPS reports to come in at a number just about 0.5 so it can round higher. There’s probably some research report waiting to be written here (grad students take note). I’ll give JOSB credit for not trying to massage their earnings higher.

All in all, this seems be a good report. I’ll have to dig through the numbers later. I added the stock at the beginning of the year and for awhile it seemed like a brilliant move on my part. The stock had been at over $48 and I was adding it at the year-end price of $29.35. By June, the stock had climbed back to $45. Since then, the stock has fallen all the way back to where it was. Fortunately, JOSB is doing well today. -

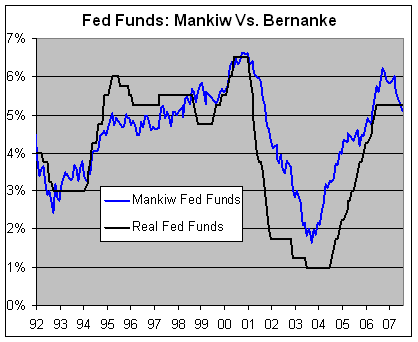

What Should the Fed Funds Rate Be?

Posted by Eddy Elfenbein on September 11th, 2007 at 2:57 pmHarvard Econ Professor (and blogger) Greg Mankiw came up with a nifty equation of determining what the Fed Funds rate ought to be.

Federal funds rate = 8.5 + 1.4 (Core inflation – Unemployment)

In July, the unemployment rate was 4.647%. The core CPI was 2.210%. That translates to a Fed Funds rate of 5.088%, which is below where the Fed is now. Here’s a look at how the Mankiw Rate compares with the real Fed Funds rate over the past few years.

One small problem with this method is lag. The latest month we have data for is July. The August CPI will be coming out next week. (I also had a minor technical criticism of Mankiw’s equation.) -

Orphan Stocks

Posted by Eddy Elfenbein on September 11th, 2007 at 2:11 pmI’m a big fan of orphan stocks. These are companies with little or no analyst coverage.

Last year, I highlighted three of my favorite banks with zero analysts following them. Since then, all three banks were bought out.

It doesn’t take much to get a good idea of how well business is going. The filings have all the details.

DealBook highlights a study on why firms get little coverage. Surprise, it’s because they don’t provide the investment banking income. -

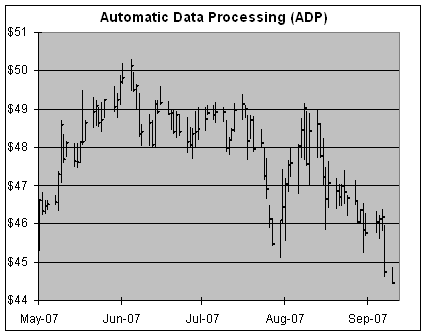

Automatic Data Processing (ADP)

Posted by Eddy Elfenbein on September 11th, 2007 at 11:38 amADP is starting to catch my eye as a good contrarian stock. (The first step, however, is to ignore their notoriously inaccurate monthly employment reports.)

The stock is down to $44 from $50 in early June. I’m not claiming any great insight on its business, but it’s simply a good stock at a good price. In the last three years, earnings are up 56%. Gross margins are around 50% and the company has a solid balance sheet. The company also raised guidance for FY 08. ADP is now looking for 12% sales growth and profit growth of 18% to 21%. I like those numbers.

-

Looking at Spinoffs

Posted by Eddy Elfenbein on September 11th, 2007 at 10:34 amHere’s an interesting look at spinoffs I saw in the WSJ from a few months ago:

Recent spinoffs have seen their shares drop more sharply than the historical trend: Spinoffs typically fall in the first month, recover by the third and start outperforming the market after six months. This happens as more analysts start covering the companies, and the spinoffs’ management teams, no longer part of big empires where attention and capital are often spread thin — are able to expand the businesses more aggressively.

A Thomson Financial study of 200 spinoffs going back to 1996 bears this out. The median stock sank 2.1% one month after its spinoff, but then inched up 1.6% after three months. In six months, the median rose 8.2%, and it climbed 12.7% within 12 months. In the smaller sample of 83 businesses spun off from S&P 500 companies, the average share price was 37.3% higher in 12 months, beating the index’s 10-year average return of 6.7%.I’m not surprised by the initial underperformance, but I doubt the rebound is due to the sudden realization that management can do whatever it wants. I think the initial drop is simply due to a high price set by the parent and a flood of selling by shareholders.

All things being equal, I look favorably at spin-offs. But there must be something worthy of spinning off before we can throw the usual hype about management no longer being constrained.

For example, Eaton Vance (EV) spun-off Investors Financial Services (IFIN) and both stocks have been remarkable performers. In fact, IFIN was recently bought out at a very rich premium. Don’t jump at every spin-off. I think DNA matters more than people realize. -

Wall Strip on Tim Hortons

Posted by Eddy Elfenbein on September 11th, 2007 at 10:03 am -

Crossing Wall Street Six Years Ago

Posted by Eddy Elfenbein on September 11th, 2007 at 8:48 am

-

The Money Honey Turns 40

Posted by Eddy Elfenbein on September 10th, 2007 at 3:44 pm

Happy Birthday Maria from everyone at Crossing Wall Street!

- Load More

You can do very well by betting on the big winners before they became the big winners.

"Japan’s births mark record low in 2024, plummet below 700,000." They predicted it would get here by 2039 but made it 15 years early. ?

Florida's Housing Market 'Turning Down Fast'

-

-

Archives

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His